India Built-in Kitchen Appliances Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Hoods, Refrigerators, Ovens & Microwaves, Hobs, Dishwashers, Others), By Application (Residential, Commercial), By Price Range (Mass, Premium), By Sales Channel (Retail Online (Direct Sale, E-Commerce), Retail Offline (Exclusive Stores, Direct Sales, Supermarkets & Hypermarkets, Others)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Built-in Kitchen Appliances Market Statistics and Insights, 2026

- Market Size Statistics

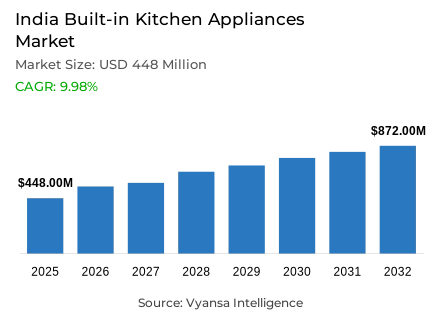

- Built-in kitchen appliances market size in India was valued at USD 448 million in 2025 and is estimated at usd 492 million in 2026.

- The market size is expected to grow to USD 872 million by 2032.

- Market to register a CAGR of around 9.98% during 2026-32.

- Product Shares

- Hobs grabbed market share of 30%.

- Competition

- More than 10 companies are actively engaged in producing built-in kitchen appliances in India.

- Top 5 companies acquired around 60% of the market share.

- Franke Group, Elica S.p.A., Glen Appliances Private Limited, LG Electronics India Private Limited, Samsung India Electronics Private Limited etc., are few of the top companies.

- Application

- Residential grabbed 85% of the market.

India Built-in Kitchen Appliances Market Outlook

The India built-in kitchen appliances market size was valued at USD 448 in 2025 and is projected to grow from USD 492 in 2026 to USD 872 by 2032, exhibiting a CAGR of 9.98% during the forecast period. Demand is supported by the steady expansion of urban housing and apartment-led living. The World Bank reports that 37% of India’s population lives in urban areas in 2024, while the Ministry of Housing & Urban Affairs states that Pradhan Mantri Awas Yojana-Urban (PMAY-U) has sanctioned 1.18 crore houses, with over 89 lakh completed by November 2024. As modern homes increasingly feature modular kitchens and fixed cabinetry, built-in appliances are becoming part of the standard kitchen layout rather than optional additions.

Within product categories, hobs hold about 30% share, reflecting their central role in cooking areas of modular kitchens. In many projects, homeowners begin kitchen upgrades with cooking equipment, which keeps demand steady for integrated hobs alongside chimneys and cabinetry. Built-in kitchen appliances also appeal because they save counter space and create a cleaner design, which fits well with compact apartment layouts and modern interior preferences.

However, higher installation costs remain a major barrier. Ministry of Statistics and Programme Implementation (MoSPI)’s Household Consumption Expenditure Survey (HCES) reports average urban MPCE at Rs. 6,996 and rural MPCE at Rs. 4,122, while the World Bank places India’s GDP per capita at US$2,694.7 in 2024. Because built-in kitchen appliances often require cabinetry, installation, and after-sales support, the total project cost becomes significantly higher than freestanding alternatives. This keeps adoption concentrated mainly in higher-income urban households and slows wider penetration.

Sales are heavily driven by housing projects and residential installations. Residential applications account for around 85% of total demand, as built-in kitchen appliances are usually included in apartment and modular kitchen designs. The Economic Survey 2024-25 reports 1.38 lakh real estate projects and 95,987 agents registered under Real Estate Regulatory Authority (RERA) as of January 2025, creating a structured housing pipeline where appliance decisions are often finalised during the design stage through builders, architects, and modular kitchen partners.

India Built-in Kitchen Appliances Market Growth DriverUrban Housing Modernisation Supports Built-In Adoption

India’s built-in kitchen appliances demand is driven by the steady expansion of urban housing and apartment-led living. World Bank data shows 37% of India’s population lives in urban areas in 2024. At the same time, the Ministry of Housing & Urban Affairs states that PMAY-U has sanctioned 1.18 crore houses, with over 89 lakh completed by November 2024. These indicators keep the base of modern kitchens broad and support demand for integrated hobs, ovens, chimneys, and dishwashers.

Built-in appliances fit well with new urban homes because they save counter space, improve layout, and support cleaner interior design. As more homes are planned with modular kitchens and fixed cabinetry, built-in products become part of the kitchen setup rather than an optional add-on. This keeps residential installation a strong demand driver for the category in India.

India Built-in Kitchen Appliances Market ChallengePremium Pricing Keeps Mass Adoption Narrow

India’s biggest challenge is the premium cost attached to built-in installation. MoSPI’s HCES, released in December 2024, puts average urban MPCE at Rs. 6,996 and rural MPCE at Rs. 4,122, while the urban-rural gap remains 70%. World Bank data also puts India’s GDP per capita at US$2,694.7 in 2024. These figures show why built-in kitchen appliances remain concentrated in higher-income households.

The issue is not only appliance pricing. Most purchases also need cabinetry, fitting, and after-sales support, which lifts the total project cost further. Because of this, many buyers still choose freestanding products that are easier to move, replace, and finance. This keeps wider penetration slower, especially outside the upper end of urban housing.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Built-in Kitchen Appliances Market TrendDigital Research and Product Transparency Shape Buying

A clear trend in India is more digital and information-led appliance buying. World Bank data shows 70% of individuals use the internet in 2025. In parallel,Bureau of Energy Efficiency (BEE) says its Standards & Labeling framework currently covers 34 appliance and equipment categories, and its star-labelled ecosystem includes domestic LPG stoves and microwave ovens. BEE’s QR-based system and consumer app also let buyers verify labels, compare models, and check savings more easily.

This is pushing built-in kitchen brands to sell on specifications, efficiency, and trust, not only looks. Buyers increasingly compare features before choosing a hob, oven, or built-in microwave, especially in premium home projects. As a result, the category is becoming more research-driven, with product transparency and performance communication playing a bigger role in final purchase decisions.

India Built-in Kitchen Appliances Market OpportunityDeveloper Tie-Ups Open a Scalable Sales Route

The strongest opportunity lies in project-led and developer-linked sales. The Economic Survey 2024-25 states that 1.18 crore houses have been sanctioned under PMAY-U and over 89 lakh are completed as of November 25, 2024. The same survey notes that 1.38 lakh real estate projects and 95,987 agents are registered under RERA as of January 6, 2025. This creates a more organized housing pipeline for built-in appliance brands.

Brands can use this route to enter at the design stage through builders, architects, and modular kitchen partners. That helps them place full kitchen sets instead of selling one product at a time. It also improves installation planning, service access, and premium positioning in residential projects where appliance decisions are often locked in before possession.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Built-in Kitchen Appliances Market Segmentation Analysis

By Product

- Hoods

- Refrigerators

- Ovens & Microwaves

- Hobs

- Dishwashers

- Others

The segment with the highest share under the product category is hobs, accounting for around 30% of the market. Hobs lead because they are the core cooking product in a built-in kitchen and usually form the starting point of modular kitchen planning. In India, homeowners upgrading kitchens often prioritize the cooking zone first, which makes hobs more essential than many other built-in appliances.

Their lead also comes from daily use and strong design value. A built-in hob gives a cleaner countertop, fits easily with chimneys and cabinets, and supports a premium kitchen look without changing the full usage habit of the household. This keeps replacement and new-install demand visible across apartments and independent homes alike, helping the segment stay ahead of other product categories.

By Application

- Residential

- Commercial

Residential kitchen appliance sales dominate the largest share of the market under appliance category, capturing approximately 85% of total sales within the total kitchen appliance industry. Increased residential kitchen appliances purchased to decorate one's home for more efficient use of the space, uniform aesthetic of design throughout the home, and everyday ease of use often lead to the demand for residential kitchen appliances. This will continue to support the volume of residential kitchen appliances sold.

This trend is further supported by the manner in which the kitchen appliances in question are marketed. There are many more commercial kitchens available for sale from builders, interior designers, and modular kitchen companies than there are residential kitchens available to buyers for installation. As a result, the market for integrated hobs, ovens, chimneys, and dishwashers in commercial kitchen settings has not been able to expand as quickly as the market for kitchen appliances in residential kitchen settings. This can be seen particularly within mid and premium grade housing projects, where residential kitchen appliances will be included in the overall kitchen design as part of the complete interior design package, thereby keeping the quantity of residential kitchen appliances sold at least four times greater than that of commercial kitchen appliances sold.

List of Companies Covered in India Built-in Kitchen Appliances Market

The companies listed below are highly influential in the India built-in kitchen appliances market, with a significant market share and a strong impact on industry developments.

- Franke Group

- Elica S.p.A.

- Glen Appliances Private Limited

- LG Electronics India Private Limited

- Samsung India Electronics Private Limited

- Whirlpool of India Limited

- Bajaj Electricals Limited

- TTK Prestige Limited

- Haier Smart Home Co. Ltd.

- Arcelik A.S.

Competitive Landscape

The competitive landscape of the India built-in kitchen appliances market in 2025 was moderately fragmented, with a mix of global premium brands and emerging domestic players competing through product innovation, distribution expansion, and modular kitchen partnerships. Key multinational players include BSH Household Appliances (Bosch and Siemens), Whirlpool, Samsung, LG Electronics, Haier, and Miele, which leverage advanced technologies such as smart connectivity, energy-efficient designs, and premium aesthetics to target urban consumers upgrading to modular kitchens. European specialist brands like Hafele, Franke Faber, and Elica focus strongly on built-in hobs, chimneys, and premium kitchen solutions through dealer networks and kitchen studio collaborations. Domestic and regional players such as Kaff Appliances, Glen Appliances, IFB Appliances, and BlowHot Kitchen Appliances compete on pricing, localized product design, and growing retail presence across Tier-1 and Tier-2 cities. Competitive strategies increasingly emphasize product launches, localized manufacturing, and partnerships with modular kitchen developers to capture rising demand driven by urbanization, rising incomes, and smart home adoption in India.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Built-in Kitchen Appliances Market Policies, Regulations, and Standards

- India Built-in Kitchen Appliances Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Built-in Kitchen Appliances Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Hoods- Market Insights and Forecast 2022-2032, USD Million

- Refrigerators- Market Insights and Forecast 2022-2032, USD Million

- Ovens & Microwaves- Market Insights and Forecast 2022-2032, USD Million

- Hobs- Market Insights and Forecast 2022-2032, USD Million

- Dishwashers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- By Price Range

- Mass- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Direct Sale- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Stores- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- India Hoods Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Refrigerators Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Ovens & Microwaves Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Hobs Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Dishwashers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Price Range- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- LG Electronics India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung India Electronics Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Whirlpool of India Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bajaj Electricals Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TTK Prestige Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Franke Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elica S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glen Appliances Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Smart Home Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arçelik A.Ş.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics India Private Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Application |

|

| By Price Range |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.