Germany Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Germany Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

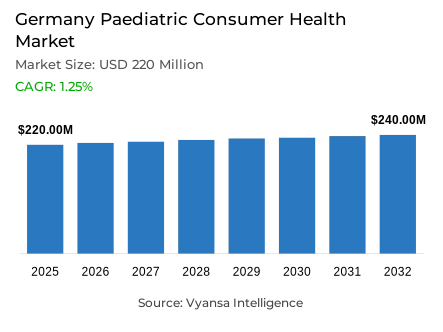

- Paediatric consumer health market size in Germany was valued at USD 220 million in 2025 and is estimated at USD 227.85 million in 2026.

- The market size is expected to grow to USD 240 million by 2032.

- Market to register a CAGR of around 1.25% during 2026-32.

- Product Type Shares

- Paediatric cough, cold and allergy remedies grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing paediatric consumer health in Germany.

- Top 5 companies acquired around 30% of the market share.

- Dr Kade Pharmazeutische Fabrik GmbH, Bene Arzneimittel GmbH, Orthomol Pharmazeutische Vertriebs GmbH, Kenvue Germany GmbH, Sanofi-Aventis Deutschland GmbH etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Germany Paediatric Consumer Health Market Outlook

The Germany Paediatric Consumer Health Market size was valued at USD 220 million in 2025 and is projected to grow from USD 227.85 million in 2026 to USD 240 million by 2032, exhibiting a CAGR of 1.25% during the forecast period. This growth is sustained by heavy investment in marketing and communication, which helps build parental confidence in child-specific formulas. While demographic shifts present some challenges, the industry remains resilient as manufacturers focus on specialized extensions of trusted brands to reduce concerns about self-selecting medicines.

The demand for safety and prevention is reshaping the product landscape, where paediatric cough, cold and allergy remedies grabbed market share of 35%. This segment benefits from the increasing availability of active-ingredient formulas specifically designed for children. Meanwhile, a notable shift toward naturalness is driving interest in drug-free and herbal options, as parents and doctors alike seek gentle paediatric consumer health solutions that prioritize tolerability and respect the young organism.

In terms of distribution, retail offline grabbed 80% of the market, with pharmacies maintaining their lead due to the high value parents place on expert consultations. However, e-commerce is emerging as the most dynamic channel through omnichannel strategies like "buy online, pick up in-store" and AI-driven shopping assistants. These digital advancements are making paediatric consumer health items more accessible, offering convenience and same-day delivery services that align with modern consumer expectations.

Looking ahead, vitamins and dietary supplements are expected to see the highest growth as families focus on physical and mental wellbeing. Clean labeling and "free-from" claims are becoming essential differentiation strategies for brands competing in a crowded space. As shelf space expands across both physical and digital platforms, the trend toward organic, locally sourced paediatric consumer health products—including child-specific probiotics and sleep aids—will likely continue to mirror broader adult wellness patterns.

Germany Paediatric Consumer Health Market Growth DriverConfidence-Focused Communication Strengthens Category Trust

Effective communication in relation to safety, dosing, and child-specific formulations is becoming a key force behind paediatric consumer health demand in Germany. Manufacturers and retailers are also focusing more on age-suited instructions, labels that are easy to understand, and educative messages to reduce reluctance among parents in choosing over-the-counter remedies to children. This communication plan will increase confidence in purchasing and promote the use of both symptomatic relief drugs and daily wellness products by caregivers as part of their daily routine.

This trend is also supported by a favorable retail climate. The Federal Statistical Office of Germany (Destatis) reports that real turnover in the “pharmacies, cosmetic, pharmaceutical and medical products” retail category increased by 3.5% in 2025 compared with 2024. The increased retail activity implies that the demand of health-related products is stable and that people still use pharmacies and specialised stores to make reliable purchases of healthcare products, such as paediatric medicines and supplements.

Germany Paediatric Consumer Health Market ChallengeDeclining Birth Rates Constrain Natural Market Expansion

Germany’s declining birth rate represents a structural constraint for paediatric consumer health products because fewer newborns reduce the inflow of new consumers entering early-childhood care routines. As the number of children in younger age groups decreases, the natural growth base for paediatric medicines, supplements, and wellness products gradually narrows.

According to Destatis, Germany recorded approximately 598,000 births between January and November 2025, which is 4.3% lower than during the same period in 2024. This demographic contraction means that manufacturers must rely more heavily on brand differentiation, product innovation, and stronger communication strategies to sustain demand. Companies increasingly focus on maintaining loyalty among existing families and encouraging repeat purchases rather than relying on population growth alone.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Paediatric Consumer Health Market TrendOmnichannel Purchasing Reshapes Access to Paediatric Products

The concept of omnichannel retail is transforming the way parents obtain paediatric consumer health products. Retailers are increasing services like online ordering, home delivery, subscription purchases, and models of buy online, pick up in store, which make it easier to repeat purchases by families. These alternatives are especially appealing to the common products like vitamins, supplements, and mild OTC medicines. This trend is supported by the development of digital commerce in Germany. Destatis reports that real turnover in internet and mail‑order retail increased by 10.1% in 2025 compared with 2024, reflecting continued expansion of e‑commerce activity.

Consumer expectations of faster and more convenient services are also being strengthened by the digitisation of the healthcare system. Gematik, the national digital health infrastructure organisation, confirms that over one billion electronic prescriptions were redeemed by October 2025, which is a sign of extensive use of digital pharmacy services. This online transformation also affects consumer expectations in the purchase of OTC paediatric products.

Germany Paediatric Consumer Health Market OpportunityClean-Label and Transparent Formulations Create Differentiation

Clean-label formulations and open ingredient communication is a significant prospect of paediatric consumer health brands. Clear ingredient lists, free-from statements, and simple benefit explanations are potent instruments of trust-building because parents tend to be more cautious when choosing products that are offered to children. Phytotherapeutic products and drug-free remedies also fit the preventive and gentle healthcare preferences of families. Regulatory control also enhances the worth of plausible safety communication.

In 2025, the official consumer-protection portal of Germany, lebensmittelwarnung.de, registered 323 product recall notices, which is an indication of active control over consumer goods and the significance of compliance and quality transparency. Brands that integrate clean-label positioning with robust records of safety and quality standards can thus develop greater credibility and long-term loyalty among caregivers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with the highest share under Product Type is paediatric cough, cold and allergy remedies, accounting for around 35% of the market based on the provided data. This segment is a leader since respiratory symptoms, congestion, and allergies are among the most common health problems in childhood, which makes them buy them repeatedly throughout the year.

Child-specific formulations are used to strengthen consumer confidence in this category. Parents usually want to use medicines with age-specific indicators and dosing regimens that are child-friendly. Since most of these conditions can be treated at home without the need to visit a physician, readily identifiable and trusted remedies tend to be the initial purchases. These aspects guarantee that cough, cold, and allergy treatments continue to be a key pillar of the paediatric consumer health product mix in Germany.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

Under the Sales Channel segmentation, Retail Offline holds the leading position with approximately 80% of total sales based on the provided data. Physical pharmacies and retail stores are still the most preferred places of purchase since parents prefer instant access and expert advice when choosing medicines to treat children.

retail offline also offers a sense of security in case of emergency health conditions, when the caregiver can compare packaging, read dosage instructions, and talk to pharmacists directly. This atmosphere builds trust and assists parents to make sure decisions when symptoms appear. Despite the growth of digital channels, retail offline still holds a leading role since paediatric health products may be in need of immediate access and high consumer confidence.

List of Companies Covered in Germany Paediatric Consumer Health Market

The companies listed below are highly influential in the Germany paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Dr Kade Pharmazeutische Fabrik GmbH

- Bene Arzneimittel GmbH

- Orthomol Pharmazeutische Vertriebs GmbH

- Kenvue Germany GmbH

- Sanofi-Aventis Deutschland GmbH

- Ratiopharm GmbH

- Nestlé Deutschland AG

- Haleon Germany GmbH

- STADA Consumer Health Deutschland GmbH

- Cooper Consumer Health Deutschland GmbH

Competitive Landscape

Germany paediatric consumer health market features a competitive landscape led by multinational healthcare companies supported by strong brand portfolios and high consumer trust. Kenvue Germany GmbH holds the leading position in retail value terms, supported by well-established brands such as Penaten, which leads nappy (diaper) rash treatments. The company also competes through Dolormin in paediatric analgesics and Olynth in paediatric cough, cold and allergy remedies. Despite its strong presence, Kenvue faces growing competition from lower-priced brands and private label products as economic pressures encourage value-focused purchasing. Increasing product extensions, particularly in paediatric vitamins and dietary supplements and child-specific formulations, are intensifying competition across the market while strengthening category visibility through expanded marketing and retail promotions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Germany Paediatric Consumer Health Market Policies, Regulations, and Standards

- Germany Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Germany Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Germany Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Kenvue Germany GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis Deutschland GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ratiopharm GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestlé Deutschland AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Germany GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dr Kade Pharmazeutische Fabrik GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bene Arzneimittel GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orthomol Pharmazeutische Vertriebs GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STADA Consumer Health Deutschland GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cooper Consumer Health Deutschland GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kenvue Germany GmbH

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.