Germany Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Germany Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

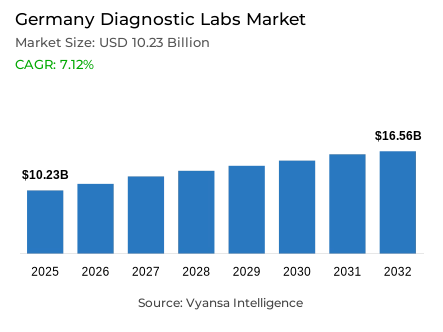

- Diagnostic labs in Germany is estimated at USD 10.23 billion in 2025.

- The market size is expected to grow to USD 16.56 billion by 2032.

- Market to register a cagr of around 7.12% during 2026-32.

- Lab Type Segment

- Hospital-based laboratories grabbed market share of 45%.

- Competition

- Diagnostic labs in Germany is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 70% of the market share.

- Bioscientia Healthcare GmbH, Laborzentrum Dr. Risch, Labor Dr. Wisplinghoff, SYNLAB, MVZ Labor Dr. Limbach & Kollegen etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Germany Diagnostic Labs Market Outlook

The diagnostic laboratory market in Germany is set to experience a healthy growth in the near future. The market is projected to grow to USD 10.23 billion in 2025 and reach USD 16.56 billion in 2032 with a consistent CAGR of about 7.12% in 2026–32. The main factors contributing to this growth are the increasing rates of chronic diseases, as more than 6.5 million German adults are already diagnosed with diabetes, and the aging population of the country is rapidly increasing. As 22.4% of Germans were aged 65 or older in 2022 and are expected to increase to 26.4% by 2030, the need to conduct diagnostic tests is growing as the elderly population requires more regular health checks and disease-management services.

The market is experiencing serious workforce issues that are transforming operational strategies. The proportion of physicians working in laboratories who are above 60 years old is about 33%, and the number of hospital laboratory staff has decreased by 29% between 2012 and 2022. To overcome these limitations, automation and AI technologies are being rapidly implemented across laboratories. As approximately 9 million laboratory results are produced each day in the country, laboratories are investing in high-throughput analyzers, robotic sample-handling systems, and AI-driven diagnostic platforms to ensure efficiency and quality standards remain high despite staffing shortages.

The preventive healthcare system in Germany is very strong and offers significant growth potential for diagnostic laboratories. The country spends 7.9% of total health expenditure on preventive care—the highest share in the European Union—supporting comprehensive screening programmes. Free comprehensive laboratory screenings are provided to adults aged above 35 years every three years, while specialised programmes such as prenatal testing encourage regular diagnostic usage across key demographic groups.

The market is dominated by hospital-based laboratories, which account for a 45% share and handle large test volumes due to high patient admissions while offering rapid turnaround times for urgent diagnostics. Similarly, general and clinical testing services contribute 45% of market revenue, covering routine blood counts, chemistry panels, and standard screenings. These basic tests form the foundation of daily diagnostic workflows, and the 20 most commonly billed laboratory tests represent approximately 73% of all outpatient examinations conducted within Germany’s healthcare system.

Germany Diagnostic Labs Market Growth Driver

Expanding Disease Burden and Demographic Shifts Accelerating Market Growth

The Germany diagnostic lab market is undergoing significant growth due to the rising number of chronic diseases and the demographic changes taking place. Currently, over 6.5 million adults in Germany are suffering from diabetes as of 2024, along with a rising number of other chronic illnesses that require periodic laboratory testing and diagnostic analysis. This demand for healthcare is further fueled by the aging demographic structure of the country, where 22.4% of the population was aged 65 years or older in 2022, and is expected to rise to around 26.4% by 2030. The older population by definition requires more frequent and comprehensive diagnostic analysis for disease management and healthcare monitoring.

The rising demand for laboratory medicine services also reflects this growing market base. In 2022, more than half (50.7%) of the insured population in Germany used laboratory medicine services, which marked a significant 5.8% increase from the previous year in 2021. Preventive and diagnostic testing has become an intrinsic part of the healthcare system for a large number of patients. The simultaneous presence of a large number of chronic diseases and a large older population is systematically fueling the number of laboratory tests being conducted across the healthcare system, making diagnostic services an integral part of patient care delivery in the Germany medical system.

Germany Diagnostic Labs Market Challenge

Workforce Shortages and Aging Personnel Creating Operational Constraints

The Germany diagnostic laboratory market is facing another tough hurdle, as there are fewer qualified workers, which, combined with an increasingly elderly workforce on the cusp of retirement, indicates a really big workforce gap. Nearly a third of all lab doctors are over 60, which far surpasses the 23% recorded in all branches of medicine. Despite an increase in the overall number of laboratory workforce coming out to 108,000 in 2022, there have been recorded 6% fewer full-time qualified workforce in the past ten years. This indicates a real challenge faced by the Germany laboratory workforce, as it recorded a 29% decline in staff in hospital lab from 2012 to 2022.

The workforce hurdle led to higher competition for certified laboratory technologists, as the occupation has now been officially recorded as a shortage occupation. The personnel shortage poses operational risks such as delays in testing, which can have a negative effect on patient care outcomes since immediate results are essential for clinical decision-making and treatment strategies. The lack of sufficient new entrants and the accelerating rate of retirements among qualified personnel is fundamentally jeopardizing the operational capacity of the Germany diagnostic laboratory infrastructure, hindering the sector from responding to growing demand despite expanding market opportunities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Diagnostic Labs Market Trend

Digital Transformation Through Automation and Artificial Intelligence Integration

Germany diagnostic labs face the reality of tech-infused change, adopting automation and AI solutions to improve efficiency, especially in the wake of the labor gap. Currently, about 9 million tests are conducted daily, and Germany diagnostic labs are investing heavily in maximizing automation. The MEDICA 2025 event in Düsseldorf featured automation and AI technologies for diagnostic tests as instrumental advancements in addressing the labor gap. Some of the developments taking place in Germany diagnostic labs include automated slide processing and image analysis.

The technological shift is visible across both large chain lab and hospital-based lab, with AI-assisted diagnostic devices increasingly incorporated into daily operations for anomaly detection and predictive analytics. Robotic solutions are undertaking repetitive tasks such as sample sorting and routine assay analysis, allowing qualified personnel to focus on advanced analytical procedures requiring specialized knowledge. This transition toward automation and intelligent systems is reshaping laboratory operations in Germany, enabling labs to handle rising workloads with greater speed and accuracy despite labor shortages.

Germany Diagnostic Labs Market Opportunity

Preventive Healthcare Emphasis Creating Service Expansion

Germany diagnostic labs are in a state of significant technological transformation, leveraging automation and artificial intelligence to maximize efficiency and overcome workforce deficiencies. Every day, lab process approximately 9 million tests, prompting heavy investment in high-volume testing devices, automated sample management, and AI-driven data systems. During MEDICA 2025 in Düsseldorf, automation and AI were highlighted as key solutions to workforce scarcity while maintaining testing quality. Notable advancements include automated slide processing and AI-based image analysis systems.

This digital shift is evident across large lab networks and individual hospital facilities, where AI-assisted tools are becoming standard for anomaly identification and predictive analytics. Robots handle routine tasks such as sample sorting and basic analyses, enabling professionals to concentrate on complex testing that requires advanced expertise. This transition toward technology-driven operations allows Germany diagnostic labs to manage expanding analytical needs with higher precision and throughput despite ongoing staffing constraints.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based lab represent the largest end-user segment in Germany’s diagnostic laboratory market, accounting for approximately 45% of total market share. These in-house facilities, typically located within major hospitals, process substantial test volumes driven by high patient admissions and comprehensive clinical service offerings. Although only about 17% of hospitals mainly large tertiary centers maintain dedicated laboratory departments, these facilities handle disproportionately high testing volumes.

This dominance is reinforced by the integration of hospital lab into clinical care pathways. On-premises labs enable rapid turnaround for critical diagnostics, supporting emergency departments and surgical services. Smaller hospitals without internal labs often outsource testing to private lab, which serve multiple clients rather than capturing the concentrated volumes typical of large hospital lab. As a result, hospital-based lab maintain their leading position through direct access to large patient populations and comprehensive internal testing capabilities.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General and routine clinical testing services constitute the largest service segment within Germany’s diagnostic laboratory market, contributing approximately 45% of total laboratory work and revenue. This segment includes high-volume analyses such as complete blood counts, blood chemistry panels, lipid profiles, glucose testing, urinalysis, and other standard screenings. These tests form the backbone of diagnostics for preventive care, chronic disease monitoring, and initial patient assessments.

Utilization patterns highlight this dominance. In 2022, the 20 most frequently billed laboratory tests primarily standard blood analyses including blood counts, TSH measurements, and HbA1c monitoring accounted for approximately 73% of all outpatient laboratory examinations. While molecular and genetic diagnostics are growing, they remain minor relative to the scale of routine testing that drives laboratory operations and revenues across Germany.

List of Companies Covered in Germany Diagnostic Labs Market

The companies listed below are highly influential in the Germany diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Bioscientia Healthcare GmbH

- Laborzentrum Dr. Risch

- Labor Dr. Wisplinghoff

- SYNLAB

- MVZ Labor Dr. Limbach & Kollegen

- Labor Dr. Schumacher

- Labor Berlin – Charité Vivantes GmbH

- Medicover Germany

- MVZ Labor PD Dr. Volkmann und Kollegen

- Labco Germany

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany Diagnostic Labs Market Policies, Regulations, and Standards

4. Germany Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Germany Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Germany Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Germany Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.SYNLAB

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.MVZ Labor Dr. Limbach & Kollegen

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Labor Dr. Schumacher

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Labor Berlin – Charité Vivantes GmbH

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Medicover Germany

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Bioscientia Healthcare GmbH

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Laborzentrum Dr. Risch

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Labor Dr. Wisplinghoff

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.MVZ Labor PD Dr. Volkmann und Kollegen

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Labco Germany

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.