Germany 155mm Artillery Shells Market Report: Trends, Growth and Forecast (2026-2032)

By Shell Type (High-Explosive (HE\HE-FRAG) Shell, Smoke Shell, Illumination Shell, Training/Practice Shell, Other Special-Purpose Shell), By Guidance (Unguided, Precision-Guided), By Range Class (Standard Range, Extended Range, Assisted Range (Base Bleed, Rocket-Assisted (RAP))), By Operational Use (Training Consumption, Routine Peacetime Stockpile Replenishment, Active Conflict Replenishment\Urgent Operational Demand, Strategic Reserve\Surge Inventory Build), By Artillery Platform Type (Towed Howitzers, Self-Propelled Howitzers, Truck-Mounted Howitzers) ... Read more

|

Major Players

|

Germany 155mm Artillery Shells Market Statistics and Insights, 2026

- Market Size Statistics

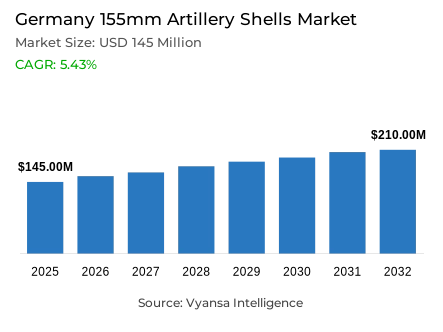

- 155mm artillery shells market size in Germany was estimated at USD 145 million in 2025.

- The market size is expected to grow to USD 210 million by 2032.

- Market to register a CAGR of around 5.43% during 2026-32.

- Shell Type Shares

- High-explosive (he/he-frag) grabbed market share of 65%.

- Competition

- 155mm artillery shells in Germany is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 70% of the market share.

- GIWS (Gesellschaft für Intelligente WirkSysteme mbH), Junghans Microtec GmbH, Nitrochemie, Rheinmetall AG, Diehl Defence etc., are few of the top companies.

- Guidance

- Unguided grabbed 80% of the market.

Germany 155mm Artillery Shells Market Outlook

The Germany 155mm artillery shells market, valued at $145 million in 2025, is poised for substantial growth over the forecast period, projected to reach $210 million by 2032. The market is expected to register a compound annual growth rate (CAGR) of approximately 5.43% during 2026-2032. This expansion is primarily driven by Germany's unprecedented defense spending allocation of over €58 billion in 2024, aimed at strengthening artillery capabilities and replenishing depleted munitions reserves. Major procurement initiatives, including Rheinmetall's €8.5 billion framework contract for 155mm ammunition, underscore the government's commitment to rebuilding stockpiles for the Bundeswehr and allied forces through 2029.

The market's growth trajectory is fundamentally shaped by heightened security concerns stemming from the Ukraine conflict and Germany's renewed NATO readiness commitments. Multi-year government contracts provide demand certainty that enables defense contractors to pursue ambitious capacity expansion plans, with Rheinmetall targeting approximately 1.5 million artillery shells annually by 2030. The 155mm artillery shells benefit from transnational cooperation, as evidenced by multinational participation from the Netherlands, Estonia, and Denmark in major procurement frameworks. This collaborative approach links allied financial resources directly to Europe-wide production capacity expansion, positioning Germany as a central hub in the evolving European defense ecosystem.

However, production bottlenecks and infrastructure limitations continue to challenge near-term supply dynamics. Despite record budget allocations, constrained factory output and procurement backlogs have left supplies trailing operational requirements. New manufacturing facilities like the Unterlüß plant in Lower Saxony offer partial relief, designed to produce 100,000 rounds annually initially and scaling to 200,000 once fully operational, yet first deliveries are not anticipated until 2025. These capacity constraints underscore the gap between surging demand and available production infrastructure during the early forecast years.

The High-Explosive (HE/HE-Frag) rounds dominate the market with a 65% share, reflecting their essential role across virtually all artillery employment scenarios for end users. Meanwhile, unguided projectiles command an 80% market share, favored for their cost-effectiveness, manufacturing simplicity, and suitability for large-scale fire missions. The preference for unguided ammunition enables military planners to maintain substantial stockpiles sufficient for extended operations, while the dominance of HE rounds underscores procurement priorities focused on general-purpose explosive projectiles that deliver fragmentation and blast effects critical to modern artillery doctrine.

Germany 155mm Artillery Shells Market Growth Driver

Escalating Defense Expenditure and Strategic Procurement Initiatives

Germany has launched a massive defence procurement spurt, spending over €58 billion in 2024 on strengthening its artillery and restoring vital munitions stocks. An example of this wave is the 155mm ammunition framework contract of Rheinmetall at 8.5 billion euros, which includes an initial delivery order of over 100,000 high-explosive rounds that will be shipped to the Bundeswehr and allied stockpiles. The urgency of the procurement is directly due to the conflict in Ukraine and the renewed dedication of Germany to NATO readiness standards, which forces the government to deal with years of underinvestment in conventional munitions. Additionally, the framework agreement involves multinational involvement of the Netherlands, Estonia, and Denmark, and contracts that run until 2029 to supply a number of hundreds of thousands of shells.

These increased security requirements have essentially changed the defence posture of Germany, which has led to aggressive replenishment of artillery ammunition throughout the NATO partnership network. The magnitude of the existing orders is not only a routine maintenance of inventory but a calculated re-alignment of conventional deterrence capabilities on a long-term basis. Multi-year demand visibility is now guaranteed by government commitments, allowing defence contractors to justify large capital investments in production infrastructure. This requirement of certainty is a structural change in the market, with allied countries aligning procurement to meet collective security goals, and share the cost of replenishing exhausted ammunition reserves.

Germany 155mm Artillery Shells Market Challenge

Production Bottlenecks and Infrastructure Limitations

Germany is experiencing severe shortages of artillery ammunition despite record budgetary allocations because of limited production capacity and backlog in procurement which has left supplies lagging behind operational demands. The problems of the Bundeswehr are rooted in decades of low factory production, which cannot instantly be increased to the levels of order volumes that are being created by the current security threats. This mismatch is exemplified by the recent acquisition of Muni Berka storage facilities by Rheinmetall, where the production is increasing at a rate that is outpacing the current logistics and distribution infrastructure, resulting in temporary bottlenecks across the supply chain. The issue of raw-materials also makes it difficult to deliver on time, with suppliers having a hard time finding specialty parts needed to make modern artillery projectiles.

The partial near-term alleviation of these capacity constraints is provided by new manufacturing facilities. The Unterlueß factory in Lower Saxony is planned to manufacture 100,000 rounds per year at the start, with a capacity of 200,000 rounds per year eventually, but the first deliveries are not expected until 2025. This slow ramp-up creates a severe mismatch between demand and supply, pushing the boundaries of the German ammunition production ecosystem. The multinational procurement programmes present further complexity due to complex coordination requirements, whereby the synchronised delivery schedules are to be aligned with the operational timelines of the allied end users. These capacity issues are interconnected and form the main limitation to the capability of Germany to meet the enormous demand of 155-mm shells within a short period of time.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany 155mm Artillery Shells Market Trend

Transnational Manufacturing Integration and Allied Collaboration

Germany is leading a radical reorganization of European ammunition production by cross-border industrialization and common production capacity. Rheinmetall currently has 155-mm shell plants in five countries and in October 2025 announced a joint venture with VMZ in Bulgaria, a new plant in Sopot that will produce 100,000 projectiles per year by 2027. This growth complements current capacity in Germany and Spain, establishing a distributed production network aimed at improving supply-chain resilience and shared production. The program is a strategic shift to transnational collaboration, in which technology transfer, investment capital, and manufacturing expertise are free to move across NATO member states to speed up the general supply of ammunition.

This industrial integration is being strengthened by multilateral procurement structures, with the Netherlands, Denmark, and Estonia co-financing the 2024 Rheinmetall contract with German funding. This joint financing scheme has become the norm, whereby allied financial resources are directly tied to the expansion of production capacity in Europe. The new trend is a European artillery-shell ecosystem in which national programmes are pooled together into common supply chains to meet common defence needs. This kind of cooperation allows smaller NATO members to gain access to high-technology manufacturing facilities and share financial risks with several partners. The position of Germany as a production centre and a procurement centre makes it the centre of this emerging European ammunition network.

Germany 155mm Artillery Shells Market Opportunity

Strategic Capacity Expansion and Vertical Integration

The long-term contract guarantees and the long-term government demand are driving transformative investments across the entire ammunition manufacturing industry in Germany. By 2030, Rheinmetall is set to increase its production to about 1.5 million artillery shells per year, with the help of the new Unterlueß plant in Lower Saxony, which will produce 200,000 155-mm rounds on its own when fully grown. These expansions are directly supported by multi-year government commitments, especially the assured 8.5 billion framework contract that offers revenue certainty enough to support high-capital expenditures. Defence contractors are now able to invest in high-tech production equipment, increase the capacity of workforce and ensure long term supplier relationships based on assured volume of orders that will last till the end of the decade.

In addition to manufacturing capacity, industry leaders are seeking vertical integration to dominate whole supply chains and overcome logistics limitations. The acquisition of Muni Berka by Rheinmetall instantly ensured storage of more than one million 155-mm projectiles, which solved bottlenecks in distribution, and increased the flexibility of the supply-chain. This is a strategic consolidation that is part of the wider self-sufficiency in key defence systems to decrease reliance on external suppliers and guarantee quick reaction to future contingencies. The overlap of assured demand, long-term investments, and infrastructure purchases places Germany in a position to significantly expand domestic ammunition manufacturing, establishing a strong industrial foundation that can serve the needs of the country and its allies over long periods of operation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany 155mm Artillery Shells Market Segmentation Analysis

By Shell Type

- High-Explosive (HE\HE-FRAG) Shell

- Smoke Shell

- Illumination Shell

- Training/Practice Shell

- Other Special-Purpose Shell

High-explosive (HE/HE-Frag) rounds make up about 65% of the 155-mm ammunition production in Germany, which is indicative of their dominance in combat operations and training exercises by end users. This segment dominates the market since HE projectiles are the base munition in nearly all artillery usage cases, providing fragmentation and blast effects that are necessary to suppress enemy troops and destroy targets. High-explosive shells are versatile and effective, which is why they cannot be ignored in a variety of operational scenarios, whether it is a defensive fire mission or an offensive barrage. None of the other shell types, such as smoke, illumination, or practice rounds, comes anywhere near the volume or strategic significance of HE ammunition in satisfying end-user needs.

The other 35% of the production includes specialized projectile variants that are used in niche tactical applications. Night operations are assisted by illumination rounds, smoke projectiles are used to obscure and signal, and practice ammunition is used to train without incurring the expense of live explosive fills. Guided munitions with sophisticated fuse technology are a new but small area of this category. The fact that HE/HE-Frag rounds have an overwhelming market share of 65% is a clear indication that procurement priorities and production planning are centered on general-purpose explosive projectiles. This focus represents the military doctrine of mass fires and volume of effect, which remains influential in the ammunition requirements of end users across the armed forces of Germany and its allies.

By Guidance

- Unguided

- Precision-Guided

Unguided artillery projectiles comprise about 80% of the 155mm shell stock of Germany, and they dominate the market because they cost less per unit, are easier to manufacture, and can be used in a variety of ways. Conventional ballistic rounds are still favored by the end users who are engaged in large scale fire missions where volume and continuous rates of fire are more important than precision engagement of a single target. The economic benefits of unguided ammunition allow military planners to hold large inventories that can sustain prolonged operations, and simplified production processes can enable manufacturers to quickly increase production during times of increased demand. The bulk of training drills and combat actions still depend heavily on unguided shells, which confirms their central position in modern artillery doctrine.

Guided 155mm projectiles, which may include GPS or laser guidance systems, are only a minor part of total supply, limited by much greater cost of acquisition and technical complexity. Although precision munitions have lower collateral damage and better performance against specific high-value targets, their cost restricts the amount that can be procured compared to conventional options. Guided rounds are normally reserved by end users in situations that require pinpoint accuracy and are used selectively and not as the main artillery ammunition. The existing 80% market share of unguided projectiles is indicative of the German strategic focus on bulk munitions that could sustain conventional operations. This distribution trend is likely to continue because military needs put a premium on ammunition availability and affordability rather than on the proliferation of high-end guided options in the short term.

List of Companies Covered in Germany 155mm Artillery Shells Market

The companies listed below are highly influential in the Germany 155mm artillery shells market, with a significant market share and a strong impact on industry developments.

- GIWS (Gesellschaft für Intelligente WirkSysteme mbH)

- Junghans Microtec GmbH

- Nitrochemie

- Rheinmetall AG

- Diehl Defence

- Nammo

- BAE Systems

- Leonardo

- Hagedorn-NC GmbH

- KNDS / Nexter Systems

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany 155mm Artillery Shells Market Policies, Regulations, and Standards

4. Germany 155mm Artillery Shells Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany 155mm Artillery Shells Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Shell Type

5.2.1.1. High-Explosive (HE\HE-FRAG) Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Smoke Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Illumination Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Training/Practice Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Other Special-Purpose Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Guidance

5.2.2.1. Unguided - Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Precision-Guided - Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Range Class

5.2.3.1. Standard Range - Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Extended Range - Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Assisted Range- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.1. Base Bleed- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.2. Rocket-Assisted (RAP)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Operational Use

5.2.4.1. Training Consumption- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Routine Peacetime Stockpile Replenishment- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Active Conflict Replenishment\Urgent Operational Demand- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Strategic Reserve\Surge Inventory Build- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Artillery Platform Type

5.2.5.1. Towed Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Self-Propelled Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Truck-Mounted Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Germany High-Explosive (HE\HE-FRAG) Shells Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Guidance- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Range Class - Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

7. Germany Smoke Shells Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Guidance- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Range Class - Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

8. Germany Illumination Shells Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Guidance- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Range Class - Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

9. Germany Training/Practice Shells Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Guidance- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Range Class - Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Rheinmetall AG

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Diehl Defence

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Nammo

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. BAE Systems

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Leonardo

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. GIWS (Gesellschaft für Intelligente WirkSysteme mbH)

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Junghans Microtec GmbH

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Nitrochemie

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. Hagedorn-NC GmbH

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. KNDS / Nexter Systems

10.1.10.1.Business Description

10.1.10.2.Product Portfolio

10.1.10.3.Collaborations & Alliances

10.1.10.4.Recent Developments

10.1.10.5.Financial Details

10.1.10.6.Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Shell Type |

|

| By Guidance |

|

| By Range Class |

|

| By Operational Use |

|

| By Artillery Platform Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.