GCC Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Country (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Rest of GCC) ... Read more

|

Major Players

|

GCC Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

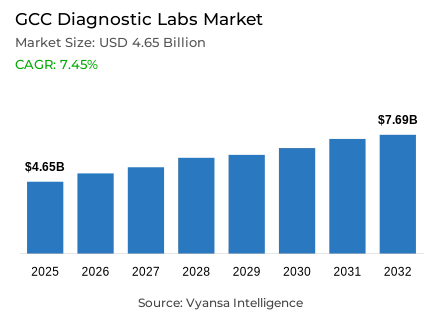

- GCC diagnostic labs market is estimated at USD 4.65 billion in 2025.

- The market size is expected to grow to USD 7.69 billion by 2032.

- Market to register a cagr of around 7.45% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 50%.

- Competition

- Diagnostic labs in GCC is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 60% of the market share.

- GCC Labs; Star Metropolis Laboratory; Thumbay Labs; Al Borg Diagnostics; MedLabs etc., are few of the top companies.

- Testing Services

- General & Clinical Testing grabbed 45% of the market.

- Country

- Saudi Arabia leads with a 40% share of the GCC market.

GCC Diagnostic Labs Market Outlook

The GCC diagnostic labs market is estimated at $4.65 billion in 2025 and is expected to reach $7.69 billion by 2032, registering a steady growth rate of around 7.45% during 2026-32. This growth is driven by strong healthcare coverage across the region, with Saudi Arabia achieving 95.9% population coverage and an average of 1.9 healthcare provider visits per individual annually. Regular patient visits across outpatient and inpatient settings ensure consistent demand for routine laboratory panels including blood counts, metabolic markers, and diagnostic cultures, creating sustained sample flow to laboratories throughout the region.

Hospital-based laboratories dominate the market with a 50% share, operating 24/7 to support emergency care, surgical procedures, and intensive care monitoring. These facilities deliver rapid turnaround times essential for immediate clinical decisions and benefit from continuous inpatient volumes. General and clinical testing accounts for 45% of the market, encompassing routine diagnostic panels like complete blood counts, glucose measurements, and lipid profiles that form the foundation of clinical workflows across primary care, pre-employment assessments, and chronic disease monitoring programs.

Digital transformation is reshaping laboratory operations, with Saudi Arabia's Nphies platform processing over 243 million insurance transactions in 2023 at 99.97% system availability. As 24.3% of adults now access their electronic medical records online, laboratories face increasing pressure to standardize test coding, reduce turnaround times, and deliver consistent digital reports that seamlessly transfer across providers and insurers.

Saudi Arabia leads the GCC market with approximately 40% share, supported by substantial government funding, extensive hospital networks, and ongoing modernization initiatives. Large-scale genomics programs, including the Emirati Genome Program with over 600,000 sequenced genomes and Qatar's 40,000+ genome database, are creating significant opportunities for advanced molecular diagnostics, positioning specialized laboratories to capture higher-value testing services as precision medicine continues advancing across the region.

GCC Diagnostic Labs Market Growth Driver

Universal Healthcare Coverage Sustains Diagnostic Demand

The official coverage levels within the GCC have sustained a constant level of diagnostic need through ensuring the population has access to healthcare services. In Saudi Arabia, the Healthcare Statistics Publication 2024 reveals that 100% of Saudi nationals have been covered for basic expenses on health care within the last year, and in total, the population received 95.9% coverage. The%ages of population coverage remain consistent at 94.8% among adults aged 15 and over, and 96.1% among children aged 15 or under, creating a platform for continuous diagnostic need. The publication reveals that on average, 1.9 health care provider visits per individual were made within the last 12 months of 2024.

This regular use in both out- and inpatient settings prompts clinicians to regularly order routine lab tests including blood counts, metabolic tests, and cultures to confirm diagnosis and monitor treatment progress, fostering the sustained process in the diagnostic labs within the region.

GCC Diagnostic Labs Market Challenge

Regulatory Scrutiny Intensifies Operational Compliance Requirements

The issue of compliance pressures is a long-standing operational challenge facing diagnostic laboratories that are operating in an ever-tightening regulatory environment. In Saudi Arabia, the Council of Health Insurance (CHI) conducted 4,462 supervisory visits in 2023, reporting 1,686 violations among service providers. Since laboratory results directly affect clinical decisions and insurance claims processing, even small non-conformities result in rework, delays, or required corrective measures, and thus significantly add to the compliance burden on laboratory management teams. Digital compliance adds another layer, and CHI reports 748 non-compliance warnings on the Nphies platform in 2023, which proves the active implementation of data standards and procedural requirements.

As a result, laboratories have to invest in quality management systems that are accreditation-ready, laboratory information system upgrades, interoperability testing, coding accuracy initiatives, cybersecurity infrastructure, and continuous staff training programmes. These demands have the potential to slow growth schedules, increase operational expenses, and overburden smaller independent facilities that are not part of large hospital networks with fewer resources to cover compliance investments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

GCC Diagnostic Labs Market Trend

Digital Infrastructure Transforms Laboratory Workflows

The platform-based data exchange has become the standard operational model of laboratory ordering, reporting, and reimbursement. According to the Council of Health Insurance of Saudi Arabia, the Nphies platform has enabled over 243 million insurance transactions in 2023, which proves that the payer-provider data exchange is now at a significant scale. The platform recorded 99.97 % system availability in the same period, which supported continuous, always-on claims processing and approvals directly related to diagnostic services without disruption. Digital health infrastructure engagement with patients is growing alongside back-end systems, with the Saudi Healthcare Statistics Publication 2024 showing that 24.3% of adults aged 15 and older use their electronic medical records online.

With end users becoming more and more exposed to diagnostic results via digital means, laboratories are under growing pressure to standardise test coding systems, shorten turnaround times, and provide cleaner and more consistent result reports that can be easily transferred across multiple providers and insurers without manual reconciliation and interpretation, which is fundamentally changing the priorities of laboratory operations and technology investments.

GCC Diagnostic Labs Market Opportunity

National Genomics Initiatives Drive Advanced Testing Adoption

The development of advanced molecular diagnostics is finding a lot of opportunities in large-scale national genomics programmes in the GCC. In Abu Dhabi, the Government Media Office states that the Emirati Genome Programme has so far sequenced over 600000 genomes, of which 100000 genome sequences have been sequenced using the latest long-read sequencing technology and extensive analysis of epigenetic data. This comprehensive reference database allows more accurate screening guidelines, variant-interpretation functionality, and companion diagnostic testing that often require specialised laboratory facilities and expertise. Qatar is also developing a large regional genomic capacity, with the Qatar Foundation stating that the Qatar Genome Programme has sequenced more than 40,000 Qatari and Arab genomes, thus creating datasets that can be used to make precision healthcare applications.

With these genomics programmes coming of age and producing actionable clinical intelligence, diagnostic laboratories with the capability to verify genetic results, perform high-quality molecular tests, and incorporate genomics findings into standard care pathways are well-placed to tap into the growing need of higher-value, higher-margin testing services that are not limited to traditional laboratory services.

GCC Diagnostic Labs Market Country Analysis

By Country

- Saudi Arabia

- UAE

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

Saudi Arabia dominates the GCC diagnostic labs market with about 40% market share, which is indicative of its status as the largest and most developed healthcare system among member states. The well-established healthcare infrastructure of the Kingdom is supported by significant government investments, a large network of hospitals, and continuous modernisation efforts that increase the capacity of service-delivery. This market dominance allows Saudi Arabia to receive large volumes of patients and also invest in modern diagnostic technologies that strengthen its competitive advantage. The strategic focus of the country on the growth of access to quality-care by means of massive public-health programmes, workforce-training programmes, and the development of infrastructure maintains the high utilisation of laboratory services among various patient groups.

The fact that Saudi Arabia is becoming a medical hub in the region also increases its market share, attracting patients throughout the GCC in search of specialised diagnostics and high-quality care services. The developed healthcare ecosystem of the Kingdom, including the developed digital-health platforms, involvement in national genomics programs, and extensive regulatory-oversight frameworks that guarantee quality standards and facilitate innovation, places the Kingdom in a position to remain a leader in the market as the healthcare demand in the region remains on the upward trend during the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

GCC Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based Laboratories represent the leading segment by Lab Type, commanding 50% of the GCC diagnostic labs market share. This dominance reflects the critical role these facilities play in delivering urgent diagnostic services, as hospital laboratories operate continuously on a 24/7 basis to support emergency care, surgical procedures, intensive care unit monitoring, and comprehensive inpatient diagnostics, resulting in continuous and time-sensitive test ordering patterns. Being embedded within hospital infrastructure enables rapid turnaround times that directly support immediate clinical decision-making and facilitates repeat testing protocols integral to patient management. Standalone and independent laboratories maintain important market presence, particularly serving walk-in patients, preventive health checkups, employer-mandated screening programs, and chronic disease patients seeking routine testing without hospital visits.

However, these facilities typically depend on physician referrals and lack the consistent inpatient volumes, integrated care pathways, and emergency workloads that characterize hospital-based operations. Consequently, hospital-linked facilities continue to anchor the laboratory service footprint, while independent laboratories compete primarily on convenience factors, home sample collection services, wellness panel offerings, and strategic partnerships with outpatient clinics and retail pharmacies.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General & Clinical Testing is the dominant segment of the Testing Services segment of the GCC diagnostic labs market, making up 45%. This segment includes routine diagnostic testing panels for diagnostic purposes, which physicians most frequently order as first-line screening methods. These include, but are not necessarily limited to, comprehensive blood counts, glucose level testing, lipid level testing, liver and kidney function testing, and infection marker testing. These diagnostic testing panels drive a steady and predictable demand in the primary care clinic setting, pre-employment screening, and preoperative testing.

Specialized and esoteric testing services such as molecular diagnostic testing, advanced immunology profiles, allergies, and oncology panels show promising clinical relevance, but these services, by contrast, are ordered for less patient populations within medicine and usually require instrumentation and interpretation capabilities. Yet, as the clinical pathway initially begins with screening and monitoring, rather than specialized testing, the role of general and clinical testing will likely be integral to laboratory daily operations, driving automation line utilization, reagent management, and phlebotomy operations, largely routine panel testing.

Various Market Players in GCC Diagnostic Labs Market

The companies mentioned below are highly active in the GCC diagnostic labs market, occupying a considerable portion of the market and shaping industry progress.

- GCC Labs

- Star Metropolis Laboratory

- Thumbay Labs

- Al Borg Diagnostics

- MedLabs

- Verita Healthcare Group

- United Laboratories

- Sultan Healthcare

- Thyrocare Gulf Laboratories WLL

- Bioscientia

- Yasmed Medical Laboratory

- Gulf Laboratory & Radiology

Market News & Updates

- Thumbay Medicity Dubai Launch, 2026:

Thumbay Group launched Thumbay Medicity Dubai (February 10, 2026), expanding integrated healthcare capacity including laboratory and diagnostic services. The launch increases testing throughput in Dubai and strengthens cross-referral flows within the Thumbay healthcare ecosystem, intensifying competition among private diagnostic providers in the UAE.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. GCC Diagnostic Labs Market Policies, Regulations, and Standards

4. GCC Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. GCC Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Country

5.2.7.1. Saudi Arabia

5.2.7.2. UAE

5.2.7.3. Qatar

5.2.7.4. Kuwait

5.2.7.5. Oman

5.2.7.6. Bahrain

5.2.7.7. Rest of GCC

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Saudi Arabia Diagnostic Labs Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Lab Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By End User- Market Insights and Forecast 2022-2032, USD Million

7. UAE Diagnostic Labs Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Lab Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Qatar Diagnostic Labs Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Lab Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Kuwait Diagnostic Labs Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Lab Type- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Disease- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Test Type- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By End User- Market Insights and Forecast 2022-2032, USD Million

10. Oman Diagnostic Labs Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Lab Type- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Testing Services- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Disease- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Test Type- Market Insights and Forecast 2022-2032, USD Million

10.2.6. By End User- Market Insights and Forecast 2022-2032, USD Million

11. Bahrain Diagnostic Labs Market Statistics, 2022-2032F

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Lab Type- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Testing Services- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By Disease- Market Insights and Forecast 2022-2032, USD Million

11.2.4. By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

11.2.5. By Test Type- Market Insights and Forecast 2022-2032, USD Million

11.2.6. By End User- Market Insights and Forecast 2022-2032, USD Million

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Al Borg Diagnostics

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. MedLabs

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Verita Healthcare Group

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. United Laboratories

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. Sultan Healthcare

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. GCC Labs

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Star Metropolis Laboratory

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

12.1.8. Thumbay Labs

12.1.8.1. Business Description

12.1.8.2. Product Portfolio

12.1.8.3. Collaborations & Alliances

12.1.8.4. Recent Developments

12.1.8.5. Financial Details

12.1.8.6. Others

12.1.9. Thyrocare Gulf Laboratories WLL

12.1.9.1. Business Description

12.1.9.2. Product Portfolio

12.1.9.3. Collaborations & Alliances

12.1.9.4. Recent Developments

12.1.9.5. Financial Details

12.1.9.6. Others

12.1.10. Bioscientia

12.1.10.1.Business Description

12.1.10.2.Product Portfolio

12.1.10.3.Collaborations & Alliances

12.1.10.4.Recent Developments

12.1.10.5.Financial Details

12.1.10.6.Others

12.1.11. Yasmed Medical Laboratory

12.1.11.1.Business Description

12.1.11.2.Product Portfolio

12.1.11.3.Collaborations & Alliances

12.1.11.4.Recent Developments

12.1.11.5.Financial Details

12.1.11.6.Others

12.1.12. Gulf Laboratory & Radiology

12.1.12.1.Business Description

12.1.12.2.Product Portfolio

12.1.12.3.Collaborations & Alliances

12.1.12.4.Recent Developments

12.1.12.5.Financial Details

12.1.12.6.Others

12.1.13. Al Noor Medical Laboratory

12.1.13.1.Business Description

12.1.13.2.Product Portfolio

12.1.13.3.Collaborations & Alliances

12.1.13.4.Recent Developments

12.1.13.5.Financial Details

12.1.13.6.Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.