France Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

France Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

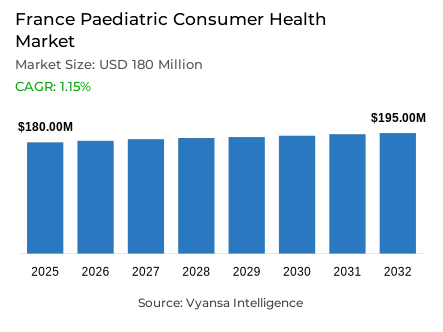

- Paediatric consumer health market size in France was valued at USD 180 million in 2025 and is estimated at USD 186.48 million in 2026.

- The market size is expected to grow to USD 195 million by 2032.

- Market to register a CAGR of around 1.15% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing paediatric consumer health in France.

- Top 5 companies acquired around 50% of the market share.

- Pharm'up SAS, Haleon France SAS, UPSA Laboratoires, Bayer Sante Familiale SAS, Laboratoires Ineldea SAS etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

France Paediatric Consumer Health Market Outlook

The France Paediatric Consumer Health Market was valued at USD 180 million in 2025 and is projected to grow from USD 186.48 million in 2026 to USD 195 million by 2032, reflecting a compound annual growth rate of 1.15% during the forecast period. The growth is moderate because the market is balancing the demographic pressures and a clear shift towards preventive healthcare. Although the decreasing birth rates decrease the number of the youngest end user segment, families are more inclined to use regular wellness solutions to enhance immunity, sleep quality, and overall wellbeing of children. This shift gradually diverts demand towards less symptom-focused medicines and more towards everyday products that are placed around long-term health support.

Within the product landscape, paediatric vitamins and dietary supplements account for approximately 45% of total market share, reflecting the escalating role of preventive nutrition in everyday childcare. Many parents currently keep supplements at home to fill nutritional deficiencies and boost immune function instead of only using occasional treatments when they are sick. The popularity of natural formulations and herbal ingredients has also strengthened the stance of these products, especially among parents who want to find milder alternatives to traditional medicines.

Distribution remains predominantly store‑based, with Retail Offline capturing about 80% of total sales. Pharmacies remain at the centre of end user health purchases in the paediatric segment since parents appreciate professional guidance in purchasing products on behalf of children. The pharmacy channel also helps the families to navigate through dosing information, compare formulations and get reliable advice on both the traditional medicines and natural wellness solutions.

In the future, the market will keep on changing towards preventive healthcare behaviours and safety-oriented buying decisions. Natural formulations, mechanical treatments and child friendly delivery formats are likely to be further popularised as parents focus on gentle but effective products. Despite the limiting nature of demographic trends, the constant demand in the paediatric end user health segment will be supported by the continuous interest of end users in immunity support, stress management, and nutritional balance.

France Paediatric Consumer Health Market Growth Driver

Climate-Linked Allergy Pressure Encourages Routine Remedies

The growing popularity of seasonal allergies due to rising temperatures and longer warm seasons is also contributing to the demand of paediatric wellness and symptom-relief products. Extended pollen periods motivate parents to keep daily-use remedies and supportive health products in children instead of treating them only with occasional treatments in cases of acute allergies. As a result, child-specific vitamins, supplements, and mild allergy remedies are increasingly becoming part of everyday domestic health.

Climate statistics point to the environmental factors that have led to this trend. Météo-France reported that the national average temperature in 2025 was about 14.0 o C, or 1.0 o C higher than the 199120 climate normal. The agency also reports that, on average, one day in every two years, the temperature was higher than seasonal norms, which means that there were long periods of warm weather, which coincide with the high activity of pollen. These circumstances maintain the constant need of allergy relief products and supportive paediatric wellness solutions.

France Paediatric Consumer Health Market Challenge

Declining Birth Rates Reduce Core Consumer Base

The paediatric end user health market in France is faced with a structural constraint of demographic change. The decrease in births will decrease the number of households with infants and young children, which directly impacts the demand of products that are directly related to early childhood care. With the aging population and a reduction in fertility rates, it becomes more difficult to maintain growth in categories that are highly dependent on the consumption of babies and toddlers.

This change is depicted in national demographic statistics. According to INSEE (Institut National de la Statistique et des Études Économiques), 645,000 births were recorded in France in 2025, representing a 2.1% decline compared with 2024 and a 24% decline compared with 2010. In 2025, the total fertility rate was 1.56 children per woman, the lowest since the end of the First World War. This population shift reduces the natural market of paediatric healthcare products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Paediatric Consumer Health Market Trend

Shift Toward Mechanical and Non-Toxic Lice Treatments

One of the most obvious trends in the field of paediatric end user health is the growing popularity of non-toxic treatment methods based on physical, not chemical action. This change is also evident in the products used in the treatment of lice, which are developed using substances like dimeticone, which kill lice by coating them and sealing their breathing holes instead of using neurotoxic insecticides. This strategy is in line with the general inclination of parents to softer products that reduce contact with harsh chemicals.

The treatment methodology also goes beyond direct application on the scalp to encompass environmental solutions. The use of products like textile sprays that are used in bedding, clothing and other household products enables the families to deal with the lice infestations in the immediate environment especially when the fabrics cannot be washed at high temperatures. These solutions are indicative of a wider safety-oriented trend in paediatric practice that places an emphasis on non-toxic and pragmatic treatment approaches.

France Paediatric Consumer Health Market Opportunity

Reliable Supply Chains Strengthen Brand Advantage

The availability of medicine has emerged as a major point of distinction in the paediatric end user health market in France. The recent years have seen supply disruptions, which have heightened the significance of brands with consistent inventories and effective communication with the pharmacy channels regarding product availability. Consistent supply assists pharmacies to retain end user confidence and also makes sure that families can obtain the necessary remedies during the seasonal illnesses.

There is public information that shows the level of medicine shortage in France. The DREES (Direction de la recherche, des études, de l’évaluation et des statistiques) analysis of the ANSM shortage reporting platform shows that shortages were the highest in the winter of 2022-2023, when about 800 medicine presentations were out of stock at the same time. As of 31 December 2024, there were about 400 presentations. In 2024, the French Ministry of Health also announced 3,825 shortage or risk-of-shortage declarations, in contrast to 4,925 in 2023, which demonstrates the continuing problem of supply reliability.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with highest market share under Product Type is Paediatric Vitamins and Dietary Supplements, accounting for approximately 45% of total demand according to the provided segmentation data. The prevalence of this category indicates the increased attention of parents to preventive healthcare and nutritional balance in children.

As opposed to medicines that are only bought when one is sick, supplements are usually part of everyday life to boost immunity, overall health, and sleep habits. The popularity of such products is also supported by interest in natural ingredients and herbal formulations, especially among parents who want to see the solutions as less aggressive and gentle compared to traditional pharmaceuticals. As a result, paediatric vitamins and supplements will continue to be the focus of the preventive healthcare trend that will dominate the French market.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

Retail Offline continues to dominate the distribution landscape, capturing approximately 80% of total paediatric end user health sales according to the provided segmentation data. The main points of purchase are still pharmacies and other physical retail stores since parents want to have direct access and expert advice when choosing healthcare products to use with children.

Pharmacists are also significant in providing advice to the caregivers on dosage, safety, and product appropriateness, which enhances end user confidence in store purchases. Physical retail also enables parents to directly compare formulations, especially when they have to decide between traditional medicines and newer natural or wellness-oriented products. These aspects guarantee that offline retail will continue to be the key channel of purchase of paediatric end user health products in France, despite the gradual growth of digital commerce.

List of Companies Covered in France Paediatric Consumer Health Market

The companies listed below are highly influential in the France paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Pharm'up SAS

- Haleon France SAS

- UPSA Laboratoires

- Bayer Sante Familiale SAS

- Laboratoires Ineldea SAS

- Laboratoires URGO SAS

- Laboratoire PediAct SARL

- Laboratoires Arkopharma SA

- Merck Médication Familiale SAS

- Expanscience SA

Competitive Landscape

France paediatric consumer health market is characterised by a fragmented competitive landscape where pharmaceutical companies and specialised natural supplement brands compete across multiple paediatric categories. Laboratoires Ineldea is a notable participant through its Pediakid range, which emphasises natural formulations targeting immunity, sleep and general wellbeing in children. The growing demand for preventive and natural health solutions has strengthened the brand’s visibility among French parents seeking alternatives to conventional medicines. Meanwhile, companies such as Omega Pharma compete in specific treatment areas with products like Pouxit, which focuses on mechanical treatment approaches. Overall competition is shaped by strict regulations, strong parental preference for natural products, and the presence of both pharmaceutical and herbal-based paediatric health solutions across the market.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- France Paediatric Consumer Health Market Policies, Regulations, and Standards

- France Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- France Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- France Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Bayer Sante Familiale SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoires Ineldea SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoires URGO SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoire PediAct SARL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoires Arkopharma SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pharm'up SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon France SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPSA Laboratoires

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Merck Médication Familiale SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Expanscience SA Laboratoires

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Sante Familiale SAS

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.