Europe Phytonutrients Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Carotenoids, Flavonoids, Polyphenols, Phytosterols/Plant Sterols, Specialty Phytonutrients (Curcumin, Organosulfur Compounds, Phytoestrogens), Others), By Functional Positioning (Antioxidant Support, Eye Health, Heart Health, Immune Support, Cognitive Health, Skin Health, Gut/Metabolic Health, Healthy Aging), By Regulatory Use Case (Dietary Supplement Ingredient, Conventional Food Ingredient, Functional Beverage Ingredient, Natural Colorant, Cosmetic Active, Feed/Animal Nutrition Ingredient), By Delivery Technology (Standard Extract Powder, Oil Suspension/Oleoresin, Water-Dispersible Format, Microencapsulated/Beadlet, Emulsified/Liposomal, Ready-to-Blend Premix), By Source (Fruits & Vegetables, Grains & Cereals, Legumes & Pulses, Herbs & Spices, Oilseeds, Others), By Form (Dry/Powder, Liquid, Others), By Sales Channel (Retail Online (Brand-Owned Websites, Third-Party E-commerce Marketplaces, Online Health & Wellness Stores), Retail Offline (Supermarkets & Hypermarkets, Pharmacies & Drug Stores, Specialty Health & Nutrition Stores)), By End-use Industry (Food & Beverages, Nutraceuticals & Dietary Supplements, Pharmaceuticals, Cosmetics & Personal Care, Animal Nutrition, Others), By Country (France, Germany, Italy, Netherlands, Spain, Rest of Europe) ... Read more

|

Major Players

|

Europe Phytonutrients Market Statistics and Insights, 2026

- Market Size Statistics

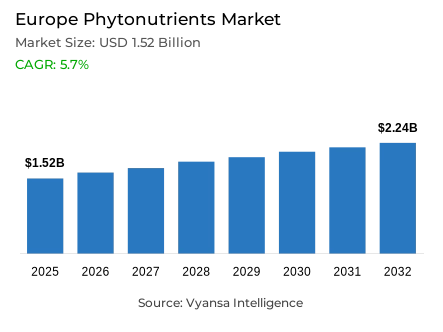

- Phytonutrients market size in Europe was valued at USD 1.52 billion in 2025 and is estimated at USD 1.61 billion in 2026.

- The market size is expected to grow to USD 2.24 billion by 2032.

- Market to register a CAGR of around 5.7% during 2026-32.

- Type Shares

- Carotenoids grabbed market share of 25%.

- Competition

- More than 10 companies are actively engaged in producing phytonutrients in Europe.

- Top 5 companies acquired around 35% of the market share.

- Euromed, Nexira, Kerry Group, Dsm-firmenich, Givaudan etc., are few of the top companies.

- End-use Industry

- Nutraceuticals & Dietary Supplements grabbed 30% of the market.

- Country

- Germany leads with a 25% share of the Europe market.

Europe Phytonutrients Market Outlook

The Europe phytonutrients market was valued at USD 1.52 billion in 2025, establishing a commercially stable and nutritionally well-anchored foundation within one of the world's most health-conscious and ingredient-sophisticated end users markets. Projected to advance from USD 1.61 billion in 2026 to USD 2.24 billion by 2032, the sector registers a CAGR of 5.7% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the sustained and growing relevance of plant-derived bioactive ingredients in health-focused product formulations across preventive nutrition, functional food, and dietary supplement categories throughout the region. Growth is anchored in genuine end users wellness orientation rather than short-cycle ingredient trend adoption, giving this market a commercial durability that sustains consistent ingredient demand across diverse application contexts and economic conditions.

The type architecture defining this market's commercial structure is anchored in carotenoid ingredients. Carotenoids command approximately 25% of total type market share, reflecting the consistent and deeply embedded formulation preference for plant-derived bioactive ingredients whose established nutritional relevance, broad application compatibility, and strong health positioning make them the reference ingredient type across nutraceutical, functional food, and wellness-oriented product development environments throughout Europe. This type concentration confirms that ingredient buyers continue to prioritize naturally derived categories whose performance credentials and end users familiarity sustain disproportionate formulation share across both established and emerging health product development cycles.

The end-use architecture reinforces the structural centrality of nutraceutical and supplement applications as the category's dominant demand source. Nutraceuticals and Dietary Supplements account for approximately 30% of total end-use market share, reflecting the foundational role of health-oriented end users product formats in driving consistent plant-based ingredient procurement across daily wellness, lifestyle management, and preventive nutrition product positioning. The European Commission's documentation that people aged 65 and over account for 22% of the EU population in 2024, up from 16% in 2004, confirms the demographic foundation that sustains institutional and brand-level investment in supplement and nutraceutical formulations whose ingredient requirements generate consistent phytonutrient procurement activity at commercially significant scale.

The forward outlook through 2032 is defined by four converging structural forces whose combined commercial impact creates a phytonutrients market of sustained and well-grounded expansion momentum. Europe's median age reaching 44.9 years in 2025 creates a broad and age-diverse end users base whose preventive health orientation sustains consistent demand for bioactive plant ingredient formulations across multiple wellness categories simultaneously. The EU's total area under organic farming reaching 16.9 million hectares in 2022, equal to 10.5% of total agricultural land, is progressively building the cleaner ingredient sourcing infrastructure that supports natural positioning claims across phytonutrient-containing products. Digital commerce reaching 78% of EU internet users making online purchases in 2025 is opening new direct-to-end users distribution pathways that expand phytonutrient product reach beyond conventional retail boundaries. Germany's combination of 83.4 million end userss and EUR 16.99 billion in organic food spending confirms the regional demand center around which competitive formulation strategy and ingredient sourcing investment are organized over the forecast period

Europe Phytonutrients Market Growth Driver

Ageing Demographics Sustain Preventive Nutrition Ingredient Demand

The rapid and institutionally documented ageing of Europe's population represents the primary structural driver of phytonutrient demand, functioning as a persistent end users wellness imperative that sustains consistent ingredient procurement across nutraceutical, dietary supplement, and functional food formulation categories whose product propositions are built around healthy ageing, daily nutritional support, and preventive lifestyle management. This demographic-driven demand dynamic transcends short-cycle end users trend fluctuations, reflecting a durable population health orientation whose purchasing volume generation is structurally anchored in the deep and growing end users motivation to invest in plant-derived bioactive ingredients that support long-term wellbeing across Europe's most commercially significant adult end users segments.

The quantitative evidence validating this demographic demand dynamic is documented with precision by the European Commission. People aged 65 and over account for 22% of the EU population in 2024, up from 16% in 2004, confirming a sustained and structurally significant demographic shift whose end users wellness purchasing implications are direct and commercially compounding across the forecast period. Europe's median age reaches 44.9 years in 2025, confirming that the broad middle-aged end users cohort whose preventive health investment motivation is strongest represents a commercially dominant share of the region's total buying population. These demographic metrics validate a end users health orientation of sufficient scale and structural depth to sustain consistent phytonutrient ingredient demand growth across supplement, functional food, and wellness product categories over the forecast period

Europe Phytonutrients Market Challenge

Agricultural Price Volatility Constrains Raw Material Cost Predictability

The structural volatility of European agricultural output prices, combined with the plant-derived character of phytonutrient raw material inputs, represents the most consequential operational challenge confronting phytonutrient producers, creating systematic ingredient sourcing cost, procurement planning, and end-product pricing stability burdens that constrain margin management across a competitively price-sensitive natural ingredient market. In a production environment where fruit, vegetable, and botanical raw material costs represent a substantial proportion of total extraction and formulation economics, agricultural price movements beyond producer control create compounding commercial pressure that is particularly consequential for manufacturers seeking to balance ingredient quality commitments with competitive product pricing across European retail and direct-to-end users channels.

The structural depth and category specificity of this agricultural cost challenge are quantified with precision by Eurostat and the European Commission. Average agricultural output prices in the EU rise by 5.6% year on year in the second quarter of 2025, while fruit prices climb by 21.1% across the same period, confirming the scale of raw material cost pressure affecting the plant-derived ingredient categories most directly relevant to phytonutrient sourcing economics. Average prices of goods and services used in agriculture and not related to investment edge up by a further 0.4% in the same period, confirming that input cost pressure moves through multiple layers of the agricultural supply chain in ways that compound extraction and formulation cost management challenges for phytonutrient producers. For manufacturers, navigating this volatility demands sustained investment in supplier diversification, contract pricing discipline, and raw material hedging capability over the forecast period

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Phytonutrients Market Trend

Organic Sourcing Momentum Reshapes Ingredient Positioning Standards

The progressive expansion of organic farming across Europe and the strengthening end users preference for traceable, clean-label plant-based ingredients represent the defining structural trend reshaping phytonutrient ingredient positioning standards, sourcing investment priorities, and competitive differentiation parameters across the regional market. This organic sourcing trend is moving the competitive conversation in the Europe phytonutrients market beyond conventional bioactivity specification and price-per-kilogram comparison into the domain of cultivation traceability, certification depth, and supply chain transparency, dimensions that are progressively redefining what health-conscious European ingredient buyers and brand formulators consider when evaluating phytonutrient sourcing partners and supply arrangements.

The institutional documentation and geographic scale of this organic sourcing trend are confirmed with precision by Eurostat and the Thünen Institute. The total area under organic farming in the EU reaches 16.9 million hectares in 2022, equal to 10.5% of total EU agricultural land, confirming that organic cultivation infrastructure is building at a pace and geographic breadth that progressively improves the availability and commercial accessibility of organically certified plant-based raw materials relevant to phytonutrient production. Germany's organically farmed area reaching approximately 1.91 million hectares in 2024, combined with end users spending on organic food rising to EUR 16.99 billion, confirms that the market environment most directly shaping European phytonutrient formulation standards is already operating at a maturity level where organic sourcing is a mainstream commercial expectation rather than a niche positioning choice. As organic ingredient sourcing becomes more widely expected across health and nutrition product categories, phytonutrient suppliers with established organic certification and traceable supply chain credentials will command disproportionate formulator preference over the forecast period.

Europe Phytonutrients Market Opportunity

Digital Commerce Expansion Creates Direct end users Access Pathways

The rapid and institutionally documented expansion of e-commerce adoption across Europe's end users population creates a structurally significant and commercially compelling opportunity for phytonutrient-containing supplement and wellness brands seeking to extend their end users reach beyond conventional retail boundaries into direct-to-end users digital channels whose purchasing frequency, product education capability, and repeat purchase dynamics are particularly well suited to ingredient-led health and nutrition product categories. This digital commerce opportunity is distinguished from conventional retail channel growth by its end users engagement depth, its ability to support ingredient communication and wellness education at the point of purchase, and the direct brand-end users relationship it creates whose data and loyalty value compounds consistently across the forecast period.

The quantitative scale and adoption momentum of this digital commerce opportunity are documented with precision by Eurostat. A total of 95% of EU individuals aged 16 to 74 use the internet in 2025, while 78% of internet users buy or order goods or services online, up from 62% in 2015, confirming that e-commerce has transitioned from an emerging channel into a mainstream end users purchasing behavior whose penetration breadth creates commercially accessible reach across every major European national market simultaneously. For phytonutrient ingredient brands and finished product formulators, this digital buying base creates a direct and progressively more accessible route to serve niche wellness needs, communicate plant-based ingredient credentials, and build repeat purchase loyalty across health-conscious end users segments that are disproportionately represented among Europe's online purchasing population. Brands that invest in digital commerce infrastructure, ingredient education content, and direct-to-end users channel capability will capture disproportionate value from this structurally significant and continuously expanding market opportunity over the forecast period

Europe Phytonutrients Market Country Analysis

By Country

- France

- Germany

- Italy

- Netherlands

- Spain

- Rest of Europe

The segment with highest market share under the Country is Germany, accounting for approximately 25% of the total market. This leading position reflects the convergence of Europe's largest national end users population, the most mature organic food consumption culture, and the deepest health and nutrition product development ecosystem within the EU, collectively creating a phytonutrient demand environment of exceptional commercial scale and ingredient sophistication. With one-quarter of total regional market value concentrated within a single national market, Germany defines the commercial priorities, formulation quality standards, and natural ingredient sourcing expectations that shape competitive strategy across the Europe phytonutrients industry.

The structural dominance of Germany is sustained by demand characteristics operating simultaneously across multiple commercial dimensions. end users spending on organic food reaching EUR 16.99 billion in 2024, combined with organically farmed land representing 11.2% of total agricultural land, confirms that Germany's food and nutrition culture has reached a maturity level at which plant-based, naturally sourced ingredient positioning carries strong and consistent commercial value across health product categories. A population of 83.4 million people in 2024, representing approximately 19% of the total EU population, confirms the end users base scale that sustains consistent and high-volume ingredient procurement across supplement, functional food, and wellness product development programs. Germany's structural position as the regional market's dominant commercial anchor is expected to deepen over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Phytonutrients Market Segmentation Analysis

By Type

- Carotenoids

- Flavonoids

- Polyphenols

- Phytosterols/Plant Sterols

- Specialty Phytonutrients

- Curcumin

- Organosulfur Compounds

- Phytoestrogens

- Others

The segment with highest market share under the Type category is Carotenoids, accounting for approximately 25% of the total market. This leading position reflects the deep structural alignment between carotenoid ingredient characteristics and the specific formulation requirements of Europe's most commercially active health and nutrition product development environments, where established nutritional relevance, broad regulatory acceptance, and strong end users familiarity make carotenoids the reference phytonutrient category across supplement, functional food, and wellness product procurement decisions. With one-quarter of total market value concentrated within a single ingredient type, Carotenoids define the commercial priorities, sourcing investment frameworks, and competitive differentiation dynamics of the Europe phytonutrients market.

The structural leadership of Carotenoids is further sustained by their inherent versatility across the full spectrum of phytonutrient application contexts, from daily nutritional supplement formulations through functional food enrichment to specialized preventive health product development. A breadth of application compatibility that creates consistent and compounding ingredient procurement demand well beyond the seasonal purchasing cycles that characterize less versatile ingredient categories. As organic farming expansion across the EU progressively builds the cleaner plant-based raw material supply chains that support natural sourcing claims, carotenoid ingredient positioning within the organic and clean-label wellness product segment is expected to strengthen commensurately. The segment's structural dominance as the market's primary revenue contributor is expected to consolidate over the forecast period.

By End-use Industry

- Food & Beverages

- Nutraceuticals & Dietary Supplements

- Pharmaceuticals

- Cosmetics & Personal Care

- Animal Nutrition

- Others

The segment with highest market share under the End-Use Industry category is Nutraceuticals and Dietary Supplements, accounting for approximately 30% of the total market. This dominant position reflects the consistent and culturally embedded role of supplement and nutraceutical product formats in European end users wellness routines, where plant-based bioactive ingredient integration into daily health management products creates consistent and high-frequency ingredient procurement demand across formulation development, product refresh, and category expansion cycles throughout the region. With nearly one-third of total market value anchored in supplement and nutraceutical demand, this end-use segment defines the ingredient specification standards, bioactivity performance benchmarks, and natural positioning requirements that shape phytonutrient procurement strategy across the Europe market.

The structural leadership of Nutraceuticals and Dietary Supplements is being actively sustained by the demographic and lifestyle forces that are deepening end users orientation toward preventive health product investment across Europe's maturing end users population. The European Commission's documentation of the EU's 65-and-over population reaching 22% of total population in 2024, combined with a median age of 44.9 years in 2025, confirms that the end users base most motivated by daily wellness, healthy ageing, and preventive nutrition product purchasing is expanding consistently as a proportion of the region's total buying population. As supplement and nutraceutical product development continues to prioritize plant-derived, naturally positioned ingredients whose bioactive credentials align with end users wellness expectations, phytonutrient ingredient demand within this end-use segment is expected to strengthen over the forecast period.

Various Market Players in Europe Phytonutrients Market

The companies mentioned below are highly active in the Europe phytonutrients market, occupying a considerable portion of the market and shaping industry progress.

- Euromed

- Nexira

- Kerry Group

- Dsm-firmenich

- Givaudan

- BASF

- Döhler

- Indena

- Kalsec

- Kemin Industries

- IFF

- Symrise

Market News & Updates

- Givaudan, 2026:

Givaudan announced a CHF 55 million investment in Campus 52 in Grasse, France, describing it as a new center of excellence for its House of Naturals organization that will combine agronomy, innovation, operations, and perfumer collaboration, with a production facility and innovation laboratory focused on high-quality natural ingredients and advanced extraction technologies. For the European phytonutrients market, this is a significant strategic move because it expands high-value natural-ingredient development capacity in one of Europe’s key botanical-processing locations and reinforces the region’s role in premium, traceable, extraction-driven plant ingredient innovation

- Euromed, 2025:

Euromed highlighted new clinical data showing that its Pomanox pomegranate extract increased circulating IGF-1 levels in a 12-week, double-blind, placebo-controlled trial involving 72 adults aged 55–70, positioning the ingredient for healthy-aging applications across cardiovascular, cognitive, metabolic, skin, and longevity-related products. For the European phytonutrients market, this is important because it strengthens the evidence base for polyphenol ingredients made and standardized in Europe, and it supports the region’s competitive advantage in clinically substantiated botanical extracts rather than commodity plant ingredients.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Phytonutrients Market Policies, Regulations, and Standards

- Europe Phytonutrients Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Carotenoids- Market Insights and Forecast 2022-2032, USD Million

- Flavonoids- Market Insights and Forecast 2022-2032, USD Million

- Polyphenols- Market Insights and Forecast 2022-2032, USD Million

- Phytosterols/Plant Sterols- Market Insights and Forecast 2022-2032, USD Million

- Specialty Phytonutrients- Market Insights and Forecast 2022-2032, USD Million

- Curcumin- Market Insights and Forecast 2022-2032, USD Million

- Organosulfur Compounds- Market Insights and Forecast 2022-2032, USD Million

- Phytoestrogens- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning

- Antioxidant Support- Market Insights and Forecast 2022-2032, USD Million

- Eye Health- Market Insights and Forecast 2022-2032, USD Million

- Heart Health- Market Insights and Forecast 2022-2032, USD Million

- Immune Support- Market Insights and Forecast 2022-2032, USD Million

- Cognitive Health- Market Insights and Forecast 2022-2032, USD Million

- Skin Health- Market Insights and Forecast 2022-2032, USD Million

- Gut/Metabolic Health- Market Insights and Forecast 2022-2032, USD Million

- Healthy Aging- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case

- Dietary Supplement Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Conventional Food Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Functional Beverage Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Natural Colorant- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic Active- Market Insights and Forecast 2022-2032, USD Million

- Feed/Animal Nutrition Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology

- Standard Extract Powder- Market Insights and Forecast 2022-2032, USD Million

- Oil Suspension/Oleoresin- Market Insights and Forecast 2022-2032, USD Million

- Water-Dispersible Format- Market Insights and Forecast 2022-2032, USD Million

- Microencapsulated/Beadlet- Market Insights and Forecast 2022-2032, USD Million

- Emulsified/Liposomal- Market Insights and Forecast 2022-2032, USD Million

- Ready-to-Blend Premix- Market Insights and Forecast 2022-2032, USD Million

- By Source

- Fruits & Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Grains & Cereals- Market Insights and Forecast 2022-2032, USD Million

- Legumes & Pulses- Market Insights and Forecast 2022-2032, USD Million

- Herbs & Spices- Market Insights and Forecast 2022-2032, USD Million

- Oilseeds- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Dry/Powder- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Third-Party E-commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Online Health & Wellness Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies & Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Health & Nutrition Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals & Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Cosmetics & Personal Care- Market Insights and Forecast 2022-2032, USD Million

- Animal Nutrition- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Country

- France

- Germany

- Italy

- Netherlands

- Spain

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- France Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Phytonutrients Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Functional Positioning- Market Insights and Forecast 2022-2032, USD Million

- By Regulatory Use Case- Market Insights and Forecast 2022-2032, USD Million

- By Delivery Technology- Market Insights and Forecast 2022-2032, USD Million

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Dsm-firmenich

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Givaudan

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Döhler

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Indena

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Euromed

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nexira

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kerry Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kalsec

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kemin Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IFF

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Symrise

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dsm-firmenich

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Functional Positioning |

|

| By Regulatory Use Case |

|

| By Delivery Technology |

|

| By Source |

|

| By Form |

|

| By Sales Channel |

|

| By End-use Industry |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.