Europe Insecticides Market Report: Trends, Growth and Forecast (2026-2032)

By Origin (Synthetic Insecticides, Bio-Insecticides), By Product Type (Pyrethroids, Organophosphate, Carbamates, Neonicotinoids, Botanicals, Others), By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Commercial Crops, Others), By Form (Sprays, Baits, Strips), By Formulation (Wettable Powder, Emulsifiable Concentrate, Suspension Concentrate, Granules, Others), By Insect Pest Type (Sucking Pest Insecticides, Biting and Chewing Pest Insecticides), By Country (Germany, France, UK, Italy, Spain, Netherlands, Poland) ... Read more

|

Major Players

|

Europe Insecticides Market Statistics and Insights, 2026

- Market Size Statistics

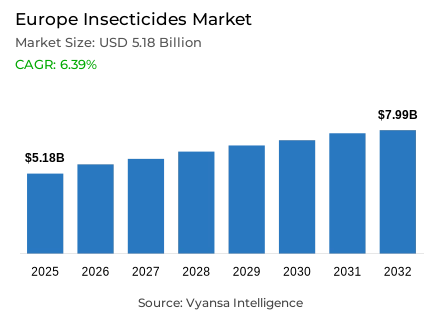

- Insecticides market size in Europe was valued at USD 5.18 billion in 2025 and is estimated at USD 5.72 billion in 2026.

- The market size is expected to grow to USD 7.99 billion by 2032.

- Market to register a CAGR of around 6.39% during 2026-32.

- Origin Shares

- Synthetic insecticides grabbed market share of 75%.

- Competition

- More than 10 companies are actively engaged in producing insecticides in Europe.

- Top 5 companies acquired around 45% of the market share.

- UPL Limited, ADAMA Ltd., Nufarm Limited, Bayer AG, Syngenta Crop Protection AG etc., are few of the top companies.

- Product Type

- Pyrethroids grabbed 30% of the market.

- Country

- Germany leads with a 25% share of the Europe market.

Europe Insecticides Market Outlook

The Europe Insecticides Market size was valued at USD 5.18 billion in 2025 and is projected to grow from USD 5.72 billion in 2026 to USD 7.99 million by 2032, exhibiting a CAGR of 6.39% during the forecast period. Demand expands as growers balance insect pest control with residue compliance, approved active-substance use, biodiversity expectations, pollinator protection, and crop-quality requirements across regulated farming systems.

Agricultural insecticides in Europe protect cereals and grains, oilseeds and pulses, fruits and vegetables, vineyards, sugar beet, commercial crops, and specialty crops from aphids, whiteflies, beetles, caterpillars, mites, and other pests. Demand exists as pest pressure can reduce crop stand, weaken plant growth, lower saleable output, damage harvested quality, and increase rejection risk in quality-sensitive supply chains. These risks make crop protection a recurring seasonal input across open-field and protected cultivation.

The Europe Insecticides Market also reflects a commercial logic linked with timely crop protection. Growers adopt crop insecticide products when field monitoring, pest thresholds, and crop-value exposure justify treatment cost. Product choice is shaped by efficacy, crop label, pest resistance management, maximum residue limits, pre-harvest interval management, application timing, formulation type, pollinator safeguards, and compatibility with integrated pest management across conventional and specialty farming systems.

The outlook remains positive but tightly regulated. Synthetic insecticides remain important where growers need reliable and fast field control, while bio-insecticides, selective chemistries, pheromone-based tools, and precision spraying gain relevance. Future demand will depend on pest pressure, active substance approval, specialty crop economics, residue limits, protected cultivation needs, and effective lower-risk alternatives. The insecticides market in Europe is therefore moving toward selective, evidence-led use, shaped by approved chemistry access and residue discipline. This keeps market development linked to practical farm decisions, not broad pesticide consumption, as growers need products that protect output while meeting regulatory and buyer requirements each season.

Europe Insecticides Market Growth Driver

Pest Monitoring Keeps Crop Protection Essential

The strongest driver in the Europe Insecticides Market is the need to protect crops from insect and mite pressure before damage affects yield, quality, or harvest timing. Eurostat reported that EU pesticide sales reached approximately 316,000 tonnes in 2024, with insecticides and acaricides accounting for 17% of the total pesticide sales mix. This is more insecticide-specific than broad pesticide use because it confirms a dedicated insect and mite-control category within EU plant-protection demand. It also shows that agricultural insecticides remain embedded within regulated crop protection programs where crop loss can occur quickly during untreated infestation windows.

The demand chain is practical. EPPO’s Alert List is designed to draw attention to pests that may present a risk to EPPO member countries and support early warning. When aphids, whiteflies, beetles, caterpillars, mites, or other crop insects cross treatment thresholds, growers need insect pest control products that protect stand, leaf area, fruit quality, and harvest scheduling. Demand in the Europe Insecticides Market therefore stays linked to crop yield protection, farm productivity, monitoring-led spraying, and rapid intervention where pest pressure threatens high-value fields. This makes timely treatment an economic decision, not only an agronomic practice, across residue-sensitive European crop systems and high-value horticulture channels.

Europe Insecticides Market Challenge

Residue Compliance Raises Use Discipline

The main challenge in the Europe Insecticides Market is strict residue and authorization control. EFSA’s latest pesticide residue data for 2024 show that 43.1% of tested food samples had no measurable pesticide residues, 54.5% contained residues within maximum residue levels, and 2.4% exceeded MRLs. This creates a tight operating environment because treatment decisions must protect crops while keeping harvested food within residue compliance boundaries. The constraint is especially important in fruits and vegetables, where buyer testing and retail specifications can quickly affect shipment acceptance.

The barrier is operational as well as regulatory. EU pesticide regulation requires products to match approved crops, authorized active substances, dose rates, pre-harvest interval management, pest stage, and maximum residue limits. If a grower applies the wrong product or sprays too close to harvest, crop value can be affected through rejected lots or restricted market access. Suppliers therefore need clearer labels, residue-conscious formulations, pollinator protection guidance, pest resistance management support, and application protocols that fit Europe’s compliance-heavy crop systems. This slows casual pesticide use and favors disciplined crop protection programs in the Europe Insecticides Market. Monitoring, documentation, and correct timing now determine buyer confidence across residue-sensitive channels and high-value export-oriented crop categories in Europe more consistently.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Insecticides Market Trend

IPM and Low-Risk Tools Reshape Use Patterns

The strongest trend in the Europe Insecticides Market is the shift from routine insecticide application toward integrated pest management and lower-risk pest-control tools. The European Commission’s IPM principles state that sustainable biological, physical, and other non-chemical methods must be preferred to chemical methods when they provide satisfactory pest control. It also states that pesticides applied should be as specific as possible for the target with the least side effects. This reinforces decision-based spraying instead of calendar-led chemical application across European crop systems and supports stronger alignment between scouting data and treatment selection.

This does not remove synthetic insecticides from European farming. It changes how agricultural insecticides are used. Growers increasingly combine pest monitoring, threshold-based treatment, biological insecticides, pheromones, selective chemistries, insecticide sprays, and precision spraying. Product adoption shifts toward IPM-compatible insecticides that fit residue control, pollinator protection, resistance rotation, and crop-specific timing. The Europe Insecticides Market therefore moves from broad preventive spraying toward evidence-led pest management, with low-residue crop protection gaining preference in fruits and vegetables, vineyards, protected cultivation, and other quality-sensitive systems. This favors products with narrower target profiles, clearer application guidance, and stronger compatibility with biological alternatives across residue-sensitive crop programs and retailer-led supply chains in Europe now.

Europe Insecticides Market Opportunity

Specialty Crops Create Focused Value Potential

The strongest opportunity in the Europe Insecticides Market lies in fruits and vegetables, where insect damage directly affects marketable quality, shelf life, appearance, and retail acceptance. The European Commission reported that fresh fruit and vegetables accounted for 13.4%, or EUR 72.2 billion, of total EU agricultural production in 2024. This supports a high-value insect-control pocket because quality loss can matter as much as yield loss in specialty crops. It also gives residue-compliant crop protection higher commercial relevance than basic field protection in horticulture.

This opportunity is narrower than broad arable-crop protection. In orchards, vegetables, berries, vineyards, and protected cultivation, even limited damage from aphids, whiteflies, caterpillars, beetles, or mites can reduce grade, create cosmetic defects, or raise rejection risk. Demand strengthens for selective insecticides, bio-insecticides, residue-conscious programs, and monitoring-led applications. The value lies in protecting marketable output and buyer acceptance, not only harvested tonnes. Sustainable crop protection therefore becomes commercially relevant where growers need insect pest control that supports crop quality, shelf-life consistency, and compliance with retail residue expectations. This creates focused demand for IPM-compatible insecticides in premium horticulture systems, keeping the Europe Insecticides Market linked to quality-sensitive crop economics rather than only broad treated acreage expansion patterns across Europe.

Europe Insecticides Market Country Analysis

By Country

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Poland

Germany leads the europe insecticides market with around 25% share, based on supplied market-share input. The germany insecticides market is supported by a large commercial farming base, structured crop-input distribution, formal pesticide reporting, advanced agronomic advisory systems, and high-value production across cereals, oilseeds, potatoes, sugar beet, fruits and vegetables, vineyards, and horticulture. Its leadership is linked with both crop scale and professionalized product use.

Germany’s Federal Environment Agency reported that 87,022 tonnes of plant protection products were sold in 2024, excluding inert gases used only in stored-product protection, and that active-substance volume reached 28,639 tonnes, up 13.2% from the previous year. This confirms a large, regulated plant protection base within Europe. Northern and eastern Germany support broadacre demand, while southern and western regions add fruits, vegetables, vineyards, and horticulture. Demand remains disciplined by residue compliance, environmental scrutiny, and active-substance review pressure, but growers still need insect control where pests threaten output and crop quality.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Insecticides Market Segmentation Analysis

By Origin

- Synthetic Insecticides

- Bio-Insecticides

The segment with the highest share under the Origin category is Synthetic Insecticides, holding around 75% of the market. Synthetic insecticides lead because they offer faster knockdown, established crop labels, predictable field performance, and familiar application protocols against major insect and mite pests. Growers still rely on them when pest pressure threatens crop establishment, crop quality, or harvest timing. This keeps chemical insecticides important in urgent crop protection decisions across diverse European crop systems and supports the current structure of the Europe Insecticides Market.

Bio-insecticides are gaining relevance under integrated pest management programs, but they remain behind where growers need rapid curative action, wider field familiarity, and stronger consistency under variable weather and pest-pressure conditions. Synthetic products remain central because they solve immediate crop-risk problems across cereals and grains, oilseeds and pulses, fruits and vegetables, vineyards, and commercial crops. Future demand will depend on selective active substances, pest resistance management, residue compliance, pollinator safeguards, and compatibility with biological crop protection. The segment’s position is therefore not based on routine use alone, but on its role in fast intervention where untreated pest outbreaks can quickly affect marketable production. This keeps demand disciplined, label-led, and commercially tied to crop-risk urgency in Europe.

By Product Type

- Pyrethroids

- Organophosphate

- Carbamates

- Neonicotinoids

- Botanicals

- Others

The segment with the highest share under the Product Type category is Pyrethroids, holding around 30% of the market. Pyrethroids lead because they are widely used synthetic insecticides with fast-acting activity against several chewing and sucking pests. Their value is strongest where approved crop uses, pest timing, and cost-effective treatment needs align with quick field control in open-field and specialty crop systems. This makes pyrethroid insecticides relevant for both sucking pest insecticides and biting and chewing pest insecticides within the Europe Insecticides Market.

A 2025 Dutch government study identifies cypermethrin, alpha-cypermethrin, deltamethrin, and lambda-cyhalothrin as synthetic pyrethroids used as insecticides. This supports the product logic behind pyrethroid relevance, while the share reflects market structure. Organophosphates, carbamates, neonicotinoids, botanicals, and other crop insecticide products remain part of the mix, but pyrethroids retain broad familiarity among growers and applicators. Environmental, resistance, and non-target organism concerns limit unchecked use, so future demand depends on label compliance, correct timing, mode-of-action rotation, IPM integration, and residue compliance. Replacement pressure will rise where resistance, residue exposure, or non-target risks intensify, but pyrethroids should remain important when approved uses, treatment windows, and pest thresholds support fast intervention in European crop protection programs under strict regulated conditions seasonally.

Various Market Players in Europe Insecticides Market

The companies mentioned below are highly active in the Europe insecticides market, occupying a considerable portion of the market and shaping industry progress.

- UPL Limited

- ADAMA Ltd.

- Nufarm Limited

- Bayer AG

- Syngenta Crop Protection AG

- BASF SE

- Corteva Inc.

- FMC Corporation

- Sumitomo Chemical Agro Europe S.A.S.

- Certis Belchim B.V.

- Mitsui Chemicals Crop & Life Solutions Inc.

- Sipcam Oxon S.p.A.

Market News & Updates

- Certis Belchim B.V, 2026:

Certis Belchim updated Eradicoat Max in January 2026 as a fast-acting contact insecticide for European growers. The soluble concentrate contains 476 g/L maltodextrin and is used against spider mite and whitefly in edible and non-edible crops under permanent protection with full enclosure. The update also highlights 10 L packs, spreading adjuvants, anti-foaming aids and reduced sticky deposits, supporting practical insect-control use in protected crop systems across the European insecticides market today and regionally. for greenhouse and enclosed horticulture operators. regionwide.

- BASF SE, 2025:

BASF highlighted Axalion Active in January 2025 as an insecticide innovation designed to work with beneficial insects. The related Axalion portfolio includes Durilon insecticide, positioned for field crops such as cereals, oilseeds and beets in select European countries. The active targets piercing and sucking pests while supporting integrated pest management programs, adding a differentiated insect-control option for growers balancing pest suppression, beneficial insect use and regulatory pressure in the European insecticides market now and locally. across regulated European crop systems.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Insecticides Market Policies, Regulations, and Standards

- Europe Insecticides Production (Million Tons) Trend 2022-2032

- Europe Insecticides Production (Million Tons) Trend By Origin

- Synthetic Insecticides

- Bio-Insecticides

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Europe Insecticides Production (Million Tons) Trend By Origin

- Europe Insecticides Pricing Analysis 2022-2032

- Europe Insecticides Pricing Trend (USD/Million Tons) 2022-2032

- Europe Insecticides Pricing Trend (USD/Million Tons) By Country 2022-2032

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Poland

- Europe Insecticides Pricing Trend (USD/Million Tons) By Origin 2022-2032

- Synthetic Insecticides

- Bio-Insecticides

- Europe Insecticides Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin

- Synthetic Insecticides- Market Insights and Forecast 2022-2032, USD Million

- Bio-Insecticides- Market Insights and Forecast 2022-2032, USD Million

- By Product Type

- Pyrethroids- Market Insights and Forecast 2022-2032, USD Million

- Organophosphate- Market Insights and Forecast 2022-2032, USD Million

- Carbamates- Market Insights and Forecast 2022-2032, USD Million

- Neonicotinoids- Market Insights and Forecast 2022-2032, USD Million

- Botanicals- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type

- Cereals & Grains- Market Insights and Forecast 2022-2032, USD Million

- Oilseeds & Pulses- Market Insights and Forecast 2022-2032, USD Million

- Fruits & Vegetables- Market Insights and Forecast 2022-2032, USD Million

- Commercial Crops- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Sprays- Market Insights and Forecast 2022-2032, USD Million

- Baits- Market Insights and Forecast 2022-2032, USD Million

- Strips- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Wettable Powder- Market Insights and Forecast 2022-2032, USD Million

- Emulsifiable Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Suspension Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Granules- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type

- Sucking Pest Insecticides- Market Insights and Forecast 2022-2032, USD Million

- Biting and Chewing Pest Insecticides- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Poland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Origin

- Market Size & Growth Outlook

- Germany Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Insecticides Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Origin- Market Insights and Forecast 2022-2032, USD Million

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Crop Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By Insect Pest Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Bayer AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Syngenta Crop Protection AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Corteva, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FMC Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPL Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ADAMA Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nufarm Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sumitomo Chemical Agro Europe S.A.S.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Certis Belchim B.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsui Chemicals Crop & Life Solutions, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sipcam Oxon S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Origin |

|

| By Product Type |

|

| By Crop Type |

|

| By Form |

|

| By Formulation |

|

| By Insect Pest Type |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.