Europe Cloud ITSM Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solutions, ITSM Platform Solutions, IT Visibility & Control Solutions, Intelligent Automation Solutions, Services, Consulting & Deployment Services, Integration & Migration Services, Support & Managed Services), By Deployment (Public Cloud, Private Cloud, Hybrid Cloud), By Enterprise Size (Large Enterprises, SMEs), By End User (BFSI, IT & Telecom, Healthcare, Retail & E-commerce, Manufacturing, Government & Public Sector, Others), By Country (UK, France, Italy, Spain, Russia, Rest of Europe) ... Read more

|

Major Players

|

Europe Cloud ITSM Market Statistics and Insights, 2026

- Market Size Statistics

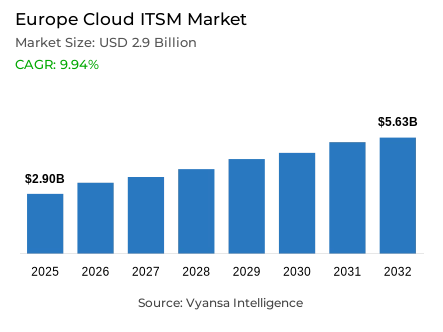

- Cloud itsm market size in Europe was valued at USD 2.9 billion in 2025 and is estimated at USD 3.19 billion in 2026.

- The market size is expected to grow to USD 5.63 billion by 2032.

- Market to register a CAGR of around 9.94% during 2026-32.

- Component Shares

- Solutions grabbed market share of 70%.

- Competition

- More than 10 companies are actively engaged in producing cloud itsm in Europe.

- Top 5 companies acquired around 25% of the market share.

- Zoho Corporation (ManageEngine), Freshworks, SolarWinds, ServiceNow, BMC Software etc., are few of the top companies.

- Deployment

- Public Cloud grabbed 45% of the market.

- Country

- Germany leads with a 20% share of the Europe market.

Europe Cloud ITSM Market Outlook

The Europe cloud ITSM market was valued at USD 2.9 billion in 2025, establishing a commercially stable and structurally well-supported foundation within one of the world's most actively digitalizing enterprise technology ecosystems. Projected to advance from USD 3.19 billion in 2026 to USD 5.63 billion by 2032, the sector registers a compound annual growth rate of 9.94% across the forecast horizon. This steady and well-anchored expansion trajectory reflects the systematic migration of enterprise IT service operations from fragmented, on-premise support structures toward integrated cloud platforms that deliver centralized incident management, workflow automation, and service visibility across increasingly distributed organizational environments. Growth is anchored in genuine operational modernization imperatives rather than technology novelty cycles, giving this market a degree of commercial resilience that sustains consistent platform investment across diverse industry verticals and national markets throughout the region.

The component architecture defining this market's commercial structure is anchored firmly in integrated platform offerings. Solutions command approximately 70% of total component market share, reflecting the consistent and deepening European enterprise preference for unified service management platforms that consolidate incident handling, request management, change coordination, and operational visibility within a single deployment framework. This concentration confirms that European buyers have moved decisively beyond point-solution procurement toward platform-oriented investment strategies. Eurostat's documentation that 52.7% of EU enterprises use paid cloud computing services in 2025, up by 7.4 percentage points from 2023, validates the cloud adoption momentum that is simultaneously expanding the organizational base requiring structured service management and elevating the complexity of the digital environments that cloud ITSM solutions must support.

The deployment architecture reinforces the primacy of public cloud as the category's dominant infrastructure preference. Public Cloud commands approximately 45% of total deployment model market share, reflecting the organizational preference for environments that deliver faster implementation timelines, lower infrastructure ownership burden, and more flexible scaling across geographically distributed service teams. Finland's documented enterprise cloud adoption rate of 79.2% in 2025, the highest recorded in the EU, confirms that mature cloud usage creates proportionally stronger demand for structured service governance, workflow coordination, and platform-level operational visibility across organizations whose IT environments have reached the complexity thresholds where informal support models become commercially and operationally inadequate.

The forward outlook through 2032 is defined by four converging structural forces whose combined commercial impact is creating a cloud ITSM market of sustained and well-grounded expansion momentum. The EU Data Act's applicability from 12 September 2025 is progressively reshaping platform selection criteria by elevating portability, interoperability, and switching ease as operational requirements rather than optional platform features. The European Commission's publication of non-binding standard contractual clauses for cloud computing contracts signals a regulatory direction that favors multi-provider service management architectures over single-vendor dependency models. The 71.9% of EU residents using public authority digital services in 2025, alongside Member States committing EUR 288.6 billion across 1,910 measures in their digital roadmaps, confirms the public-sector investment momentum that is expanding cloud ITSM's addressable market well beyond private enterprise boundaries. The ICT specialist talent shortage documented across 57.5% of recruiting enterprises creates simultaneous adoption constraints and premium pricing conditions for providers whose platforms deliver automation-led complexity reduction over the forcat period.

Europe Cloud ITSM Market Growth Driver

Rising Enterprise Cloud Adoption Expands the Structural Cloud ITSM Demand Base

The rapid and institutionally documented expansion of paid cloud computing service adoption across European enterprises represents the primary structural driver of cloud ITSM demand, functioning as a persistent organizational complexity mechanism that continuously expands the scale and sophistication of the IT service management requirements that cloud-based platforms must address. As more European organizations transition core business processes into cloud environments, the operational requirements for centralized incident management, structured workflow coordination, change governance, and service visibility scale in direct proportion to the breadth and complexity of the cloud workload portfolio that each organization manages. This cloud adoption-driven demand dynamic creates a self-reinforcing growth mechanism whose commercial implications for cloud ITSM platform investment are direct, measurable, and structurally compounding across the forecast horizon.

The quantitative momentum of this cloud adoption-driven demand dynamic is documented with precision by Eurostat. A total of 52.7% of EU enterprises use paid cloud computing services in 2025, up by 7.4 percentage points from 2023, confirming that enterprise cloud adoption is advancing at a pace that consistently expands the organizational base requiring structured cloud service management capabilities. The most common cloud use cases already include email, office software, and file storage, confirming that cloud-based business process dependency has moved well beyond peripheral application adoption into the core operational systems whose reliable performance and structured support management are mission-critical organizational requirements. This cloud adoption trajectory is expected to sustain structural cloud ITSM demand expansion across European enterprise and public-sector buyer segments.

Europe Cloud ITSM Market Challenge

ICT Talent Shortages Constrain Platform Implementation Quality and Adoption Velocity

The persistent shortage of qualified ICT specialists across European organizations represents the most consequential structural challenge confronting the Europe cloud ITSM market, creating systematic platform implementation quality, workflow optimization capability, and service maturity development constraints that moderate adoption velocity and limit the operational value realization that organizations achieve from cloud service management platform investments. In a market where cloud ITSM platform effectiveness depends directly on the competency of the teams managing workflow configuration, automation design, integration architecture, and user support delivery, the availability and retention of qualified digital talent functions as a binding operational constraint on platform adoption quality across the most digitally ambitious European enterprise environments.

The structural depth and organizational specificity of this talent challenge are quantified with precision by Eurostat and the European Commission. More than 10 million people work as ICT specialists in the EU in 2024, representing 5.0% of total employment, yet this specialist workforce remains insufficient for the pace of digital expansion across the region's enterprise technology landscape. A total of 57.5% of companies that recruited or tried to recruit ICT specialists in 2023 report difficulties filling those roles, confirming that hiring pressure across the digital talent market is both widespread and structurally persistent rather than cyclically temporary. For cloud ITSM providers, this talent constraint creates a strategic imperative to develop platforms that deliver maximum service management value with minimum specialist configuration complexity, positioning automation depth and deployment simplicity as primary competitive differentiators.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Cloud ITSM Market Trend

EU Data Act Interoperability Requirements Reshape Platform Selection Criteria

The applicability of the EU Data Act from 12 September 2025 represents the defining regulatory trend reshaping cloud ITSM platform selection criteria across European enterprise and public-sector buyer segments, fundamentally elevating portability, interoperability, and multi-provider switching ease from optional platform features into operational requirements whose absence creates meaningful procurement disqualification risk for non-compliant solution providers. This regulatory evolution is moving the competitive differentiation axis in the Europe cloud ITSM market decisively beyond traditional service management functionality and workflow control into the domain of data portability architecture, open integration standards compliance, and contractual switching rights transparency, dimensions that are progressively redefining what European organizations consider baseline platform capability within cloud service management procurement evaluations.

The regulatory specificity and commercial implications of this interoperability trend are documented with authority by the European Commission. The EU Data Act becomes applicable on 12 September 2025, establishing a regulatory framework that explicitly addresses cloud switching rights, data portability obligations, and interoperability requirements across cloud computing contracts. The European Commission's publication of non-binding standard contractual clauses for cloud computing contracts provides additional implementation guidance that is progressively standardizing the contractual transparency expectations that cloud ITSM providers must satisfy to access the most compliance-sensitive European enterprise and public-sector buyer segments. As regulatory and operational expectations around cloud interoperability mature, European organizations are placing progressively greater procurement weight on service management platforms whose architecture supports multi-provider environments and smoother service transitions without creating operational lock-in or workflow continuity risk.

Europe Cloud ITSM Market Opportunity

Public Sector Digital Transformation Creates a Structurally Expanding Cloud ITSM Adoption Wave

The large-scale and institutionally committed public-sector digital transformation programs being executed across European Member States represent the most commercially significant and structurally durable growth opportunity within the Europe cloud ITSM market, delivering a policy-backed demand expansion dynamic whose investment scale, long-horizon execution commitments, and service management platform requirements generate cloud ITSM adoption opportunities of exceptional commercial value and revenue visibility across the region's most organizationally complex public-sector environments. This public-sector opportunity is distinguished from private enterprise demand by its institutional investment certainty, multi-year execution horizon, and the structured procurement processes through which public authorities evaluate and adopt cloud service management platforms at organizational scales that generate high-value, long-duration platform contracts.

The quantitative scale and institutional specificity of this public-sector opportunity are documented with precision by Eurostat and the European Commission. A total of 71.9% of EU residents use websites or apps of public authorities in 2025, up 1.9 percentage points from 2024, confirming that digital public service delivery has reached the population penetration scale at which structured cloud-based service management becomes an operational necessity for the agencies and institutions responsible for maintaining service quality, request handling efficiency, and citizen-facing support responsiveness. Member States outline 1,910 measures worth EUR 288.6 billion in their digital roadmaps, confirming the institutional investment scale and long-horizon execution commitment that sustains public-sector cloud ITSM adoption momentum across the region's diverse national administrations. cloud ITSM providers that combine EU regulatory compliance credentials, public-sector procurement process alignment, and platform capabilities optimized for citizen-facing service delivery environments will capture disproportionate value from this structurally significant and geographically broad opportunity through 2032.

Europe Cloud ITSM Market Country Analysis

By Country

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

Germany leads the Europe cloud ITSM market with around 20% share, making it the most prominent country-level contributor to the regional landscape. This position reflects a strong enterprise technology base and a favorable environment for service management modernization. Its leading share shows that Germany remains an important demand center and continues to influence the broader direction of industry development across Europe.

The country’s strong role also highlights its importance for vendors aiming to build stronger regional presence and long-term business opportunities. As enterprises continue to improve digital workflows and service efficiency, cloud ITSM remains closely tied to markets that offer stronger adoption potential and higher operational maturity. With around 20% share already in place, Germany continues to act as a key focus area for solution providers across the regional market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Cloud ITSM Market Segmentation Analysis

By Component

- Solutions

- ITSM Platform Solutions

- IT Visibility & Control Solutions

- Intelligent Automation Solutions

- Services

- Consulting & Deployment Services

- Integration & Migration Services

- Support & Managed Services

The segment with highest market share under the Component is Solutions, accounting for approximately 70% of the total market. This commanding position reflects the deep organizational preference for integrated platform capabilities that consolidate service desk operations, incident handling, workflow automation, and IT asset visibility within a unified deployment structure that eliminates the operational fragmentation and integration complexity of point-solution procurement approaches. With seven-tenths of total market value concentrated within a single component category, Solutions define the commercial priorities, product development investments, and competitive differentiation frameworks of the Europe cloud ITSM market. The preference for unified platforms is being actively reinforced by the rising cloud workload complexity that Eurostat documents across EU enterprises, where the most common cloud use cases of email, office software, and file storage are progressively expanding into core business process environments that require structured incident management, change coordination, and service continuity governance.

The structural leadership of Solutions is being further sustained by the EU Data Act's applicability from September 2025, which is elevating enterprise expectations for platform interoperability and data portability across cloud service management environments. As organizations place greater operational value on platforms that can work across multi-provider cloud ecosystems without creating workflow friction or service continuity risk, solution providers whose platform architecture natively supports interoperability standards and open integration frameworks will attract disproportionate share of enterprise platform investment. The segment's structural dominance as the market's primary revenue contributor and competitive differentiation focal point is expected to consolidate.

By Deployment

- Public Cloud

- Private Cloud

- Hybrid Cloud

The segment with highest market share under the deployment is public cloud, accounting for approximately 45% of the total market. This leading position reflects the consistent organizational preference for deployment environments that deliver faster implementation timelines, reduced infrastructure management overhead, continuous platform improvement through automated updates, and flexible scaling across distributed service teams and user populations. Public cloud's alignment with the digital modernization priorities of European enterprises is being actively reinforced by Eurostat's documentation of steadily rising paid cloud computing service adoption across EU organizations, where the transition of core business processes into cloud environments creates proportionally expanding requirements for cloud-native service management platforms capable of supporting the operational complexity of digitally mature organizational environments.

The structural leadership of Public Cloud is further reinforced by the European Commission's regulatory evolution around cloud computing contractual standards, which is progressively building enterprise confidence in public cloud deployment pathways by establishing clearer frameworks for data portability, switching rights, and service continuity obligations. As regulatory clarity around cloud computing contracts improves and interoperability standards mature, the compliance-related hesitancy that historically moderated public cloud ITSM adoption among more cautious European enterprise buyers is progressively diminishing. This regulatory confidence-building dynamic is expanding the addressable public cloud ITSM market by converting previously undecided buyer segments into active platform adoption candidates. The segment's structural leadership as the market's primary deployment standard is expected to strengthen.

Various Market Players in Europe Cloud ITSM Market

The companies mentioned below are highly active in the Europe cloud itsm market, occupying a considerable portion of the market and shaping industry progress.

- Zoho Corporation (ManageEngine)

- Freshworks

- SolarWinds

- ServiceNow

- BMC Software

- Atlassian

- Ivanti

- Broadcom

- Zendesk

- OpenText

- Microsoft

- GoTo

Market News & Updates

- Atlassian, 2025:

At Team ’25 Europe in October 2025, Atlassian introduced Service Collection as an AI-first service management suite designed to unify internal and external service delivery across IT, Ops, HR, and customer support, with Jira Service Management as the foundation, Customer Service Management for external support, Assets for service context, and Rovo agents as embedded AI teammates. For the European Cloud ITSM market, this is especially significant because the launch was positioned directly in Europe and reflects growing regional demand for consolidated, cloud-native service platforms that reduce tool sprawl, accelerate AI adoption, and improve service resilience across both employee and customer-facing workflows.

- Freshworks, 2025:

In July 2025, Freshworks announced a multi-year partnership with the McLaren Formula 1 Team, stating that AI-powered Freshservice already accelerates the team’s IT operation, and that the partnership would be visible from the Belgian Grand Prix onward on McLaren cars and team kits. For the European Cloud ITSM market, this is a meaningful strategic validation because it places Freshservice at the center of a high-speed, UK-based operational environment where uptime, rapid incident resolution, and real-time support are mission-critical, strengthening Freshworks’ credibility among European enterprises evaluating agile cloud ITSM platforms for complex and performance-sensitive operations

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Cloud ITSM Market Policies, Regulations, and Standards

- Europe Cloud ITSM Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- ITSM Platform Solutions- Market Insights and Forecast 2022-2032, USD Million

- IT Visibility & Control Solutions- Market Insights and Forecast 2022-2032, USD Million

- Intelligent Automation Solutions- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Consulting & Deployment Services- Market Insights and Forecast 2022-2032, USD Million

- Integration & Migration Services- Market Insights and Forecast 2022-2032, USD Million

- Support & Managed Services- Market Insights and Forecast 2022-2032, USD Million

- By Deployment

- Public Cloud- Market Insights and Forecast 2022-2032, USD Million

- Private Cloud- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Cloud- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- SMEs- Market Insights and Forecast 2022-2032, USD Million

- By End User

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- IT & Telecom- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Government & Public Sector- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Country

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- UK Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Russia Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- ServiceNow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BMC Software

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Atlassian

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ivanti

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Broadcom

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zoho Corporation (ManageEngine)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Freshworks

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SolarWinds

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zendesk

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OpenText

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GoTo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ServiceNow

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Deployment |

|

| By Enterprise Size |

|

| By End User |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.