Europe 155mm Artillery Shells Market Report: Trends, Growth and Forecast (2026-2032)

By Shell Type (High-Explosive (HE\HE-FRAG) Shell, Smoke Shell, Illumination Shell, Training/Practice Shell, Other Special-Purpose Shell), By Guidance (Unguided, Precision-Guided), By Range Class (Standard Range, Extended Range, Assisted Range (Base Bleed, Rocket-Assisted (RAP))), By Operational Use (Training Consumption, Routine Peacetime Stockpile Replenishment, Active Conflict Replenishment\Urgent Operational Demand, Strategic Reserve\Surge Inventory Build), By Artillery Platform Type (Towed Howitzers, Self-Propelled Howitzers, Truck-Mounted Howitzers), By Country (Germany, France, UK, Italy, Spain, Rest of Europe) ... Read more

|

Major Players

|

Europe 155mm Artillery Shells Market Statistics and Insights, 2026

- Market Size Statistics

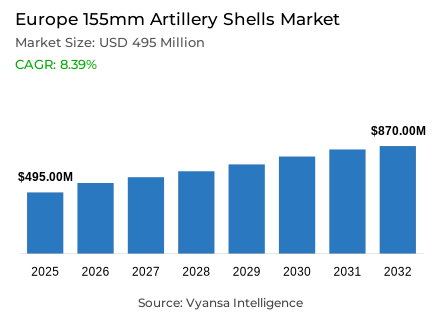

- 155mm artillery shells market size in Europe was estimated at USD 495 million in 2025.

- The market size is expected to grow to USD 870 million by 2032.

- Market to register a CAGR of around 8.39% during 2026-32.

- Shell Type Shares

- High-explosive (he/he-frag) shell grabbed market share of 65%.

- Competition

- 155mm artillery shells in Europe is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 70% of the market share.

- Elbit Systems, General Dynamics Ordnance & Tactical Systems, Thales, Rheinmetall, Nexter (KNDS) etc., are few of the top companies.

- Guidance

- Unguided grabbed 80% of the market.

- Country

- Germany leads with a 30% share of the Europe market.

Europe 155mm Artillery Shells Market Outlook

The Europe 155mm artillery shells market is estimated at $495 million in 2025 and is forecast to reach $870 million by 2032, growing at a CAGR of approximately 8.39% over 2026-32. This robust trajectory is anchored by the EU's SAFE instrument, which provides up to €150 billion in long-maturity loans with ammunition and artillery systems designated as priority procurement categories, creating sustained and policy-backed demand momentum across the continent.

Procurement patterns reveal clear volume preferences. High-Explosive (HE/HE-FRAG) shells account for 65% of total demand, driven by their versatility across training, stockpiling, and active fire missions and their seamless compatibility with standard NATO platforms. Within the 155mm artillery shells segment, unguided ammunition commands an even larger 80% share, valued for lower unit costs, faster production cycles, and straightforward qualification across multiple allied platforms - characteristics that align directly with SAFE's emphasis on urgent, large-scale standardised deliveries.

Supply-side constraints remain a significant structural challenge. Input shortages spanning metals, energetic chemicals, and propellants, combined with a limited subcontractor base, keep EU production at roughly 50% of required capacity. EDIP's €1.5 billion grant programme for 2025-2027 is designed to address these gaps by opening funded pathways for SMEs, mid-caps, and emerging suppliers to scale capacity in shell casings, propellant charges, and energetic materials - all while complying with European-preference sourcing rules that cap non-EU component costs at 35%.

Germany anchors regional demand with a 30% share, supported by a combined 2026 defence budget of €108.2 billion and consistent delivery on NATO's 2% GDP spending benchmark. Its €8.5 billion Rheinmetall framework contract for 155mm ammunition reinforces both domestic industrial output and broader allied supply chain resilience, cementing the country's role as Europe's central node for artillery ammunition procurement and industrial coordination.

Europe 155mm Artillery Shells Market Growth Driver

Policy-Driven Procurement Momentum and Rising Defence Investment

The 155mm artillery shells market in Europe is experiencing significant demand acceleration which is supported by the strategic financing frameworks of the European Union. The Security Action for Europe (SAFE) tool of the EU offers up to EUR 150 billion long-term loans, which allow Member States to conduct urgent, large-scale procurement programmes to bridge critical capability gaps. SAFE specifically names ‘Ammunition and Missiles’ and ‘Artillery Systems’ as priority product categories, thus directly directing financing to 155mm shell replenishment on the continent.

In addition to SAFE, Germany, the largest end user in the market, with largest share of demand, has pledged a total defence budget of about EUR 108.2 billion in 2026, including EUR 82.69 billion of regular defence spending and EUR 25.51billion of Bundeswehr special fund. This long-term financial investment guarantees further acquisition and replenishment of stocks on a large scale, which strengthens a stable and increasing demand in the wider European artillery ammunition ecosystem.

Europe 155mm Artillery Shells Market Challenge

Supply-Side Bottlenecks and Production Capacity Limitations

The market of Europe 155mm artillery shells has continued to experience supply-side limitations that hinder volume scaling despite strong procurement intent by end users and governments. The European Parliament has pointed to severe shortages in key production materials, such as metals, energetic chemicals, and propellants, and a small number of specialised subcontractors, which has been a bottleneck even in the production of standard artillery ammunition. These organizational weaknesses reduce the speed at which producers can react to the soaring demand.

To make the situation even more difficult, most manufacturers operate on a build-to-order basis due to financial risk considerations, which means that delivery times are long unless governments can give predictable and multi-year demand signals. Defence Commissioner Kubilius has admitted that the EU is still only generating half the required capacity, which keeps the market in a state of chronic undersupply. The reconstruction or the expansion of production infrastructure is still slow and capital-intensive, which restricts the growth of output in the short term, despite the favorable policy tailwinds.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe 155mm Artillery Shells Market Trend

European Content Localisation and Evolving Procurement Architecture

The growing focus on European-preference sourcing regulations within procurement systems is a characteristic structural trend that is transforming the Europe 155mm artillery shells market. In the case of SAFE, contracts must ensure that no more than 35% of component costs originate from outside the EU, EEA-EFTA, or Ukraine. This threshold directly guides sourcing decisions to European suppliers of energetics, metalworking components, and fuze systems, speeding up supply-chain reconfiguration along the ammunition value chain.

This trend is reinforced by the European Defence Industry Programme (EDIP) which introduces the same 35 % ceiling and an EU-wide security-of-supply framework. This has seen prime contractors and subcontractors increasingly focusing on EU-based qualification, dual sourcing, and capacity development in sensitive input areas, such as propellants, explosives, and certified testing facilities, to remain eligible to compete on publicly funded tenders. These dynamics are essentially transforming the way the 155mm supply chain is organized and managed in Europe.

Europe 155mm Artillery Shells Market Opportunity

Grant Financing and Industrial Expansion Pathways for New Entrants

The introduction of EDIP creates measurable expansion opportunities for mid-tier and emerging suppliers seeking a foothold in the Europe 155mm artillery shells market. EDIP provides €1.5 billion in grants for 2025-2027, including €300 million earmarked for a dedicated Ukraine Support Instrument to integrate Ukrainian industrial capacity into Europe's defence ecosystem. These grant mechanisms open funded pathways for capacity upgrades in artillery ammunition sub-segments such as shell casings, modular propellant charges, energetic materials handling, and certified testing.

EDIP's explicit mandate to facilitate market access for SMEs, mid-caps, and start-ups further broadens participation across the 155mm value chain. End users - including national armed forces and procurement agencies - stand to benefit from a more diversified and resilient supplier base as a result. For suppliers aligned with EU preference rules, EDIP-backed common procurement actions provide a structured route to scale operations, reduce per-unit costs through larger order volumes, and establish long-term supply relationships with defence ministries and prime contractors across the region.

Europe 155mm Artillery Shells Market Country Analysis

By Country

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

Germany dominates the European 155mm artillery-shell market with a 30% market share, supported by a long-term increase in defence spending, and by the structural policy change that is part of its historic strategy, the Zeitenwende. NATO 2025 Defence Expenditure Report indicates that Germany spent 2.12% of its GDP on defence in 2024, the first time the country has consistently spent 2% of its GDP on defence as required by NATO. This achievement is a paradigm change in the strategic position of Berlin, which is a long-term investment in military preparedness and the rapid re-equipment of artillery reserves that were lost in the changing security needs of the continent.

Systematically delivering on the 2% GDP threshold significantly enhances Germany's ability to fund high-volume procurement schemes and support scaling efforts within its domestic defence sector. As one of the biggest absolute defence spenders in 2024, Germany maintains a stable long-horizon procurement pipeline that directly supports artillery stock rebuilds and interoperability obligations with allies. This set of fiscal and strategic strengths further cements Germany's leading regional role in the 155mm artillery shells market and positions it as the key regional anchor of European artillery ammunition demand.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe 155mm Artillery Shells Market Segmentation Analysis

By Shell Type

- High-Explosive (HE\HE-FRAG) Shell

- Smoke Shell

- Illumination Shell

- Training/Practice Shell

- Other Special-Purpose Shell

Under the shell type segmentation, the High-Explosive (HE/HE-FRAG) shell category holds the dominant position in the Europe 155mm artillery shells market, accounting for approximately 65% of total demand. HE rounds maintain their leading share owing to their unmatched versatility as a 'default' munition suitable for training exercises, strategic stockpiling, and sustained fire missions. Their compatibility with standard NATO 155mm artillery systems, without requiring specialised mission planning or platform modifications, makes them the preferred choice for end users seeking operational flexibility and logistical simplicity.

The structural composition of European procurement further consolidates HE dominance. SAFE's financing mechanism is designed to support urgent, large-scale purchases of standardised ammunition, incentivising governments and allied procurement bodies to prioritise interoperable rounds that manufacturers can produce at volume and deliver on accelerated timelines. As European nations work to replenish depleted stocks and build sustainable reserve levels, HE/HE-FRAG shells continue to anchor procurement programmes, ensuring this segment retains its majority demand share throughout the forecast horizon.

By Guidance

- Unguided

- Precision-Guided

Within the guidance segmentation, unguided ammunition holds an commanding 80% share of the Europe 155mm artillery shells market. The dominance of unguided rounds is rooted in their significant advantages in large-scale procurement contexts: they are simpler and faster to manufacture, easier to qualify across diverse artillery platforms, and substantially cheaper to procure and stockpile for readiness maintenance and routine training cycles. These attributes make unguided shells the pragmatic default for end users managing broad-based replenishment requirements across multiple allied nations.

European policy design reinforces this volume-first procurement approach. SAFE's emphasis on financing urgent, large-scale ammunition deliveries favours rounds that can be produced and fielded immediately without complex integration requirements. Common procurement frameworks organised under SAFE and EDIP further incentivise standardised, interoperable unguided shells that satisfy the requirements of multiple end users in a single contract action. While precision-guided munitions remain strategically relevant, their higher unit cost and longer qualification timelines position unguided variants as the backbone of European 155mm artillery shell demand for the foreseeable future.

Various Market Players in Europe 155mm Artillery Shells Market

The companies mentioned below are highly active in the Europe 155mm artillery shells market, occupying a considerable portion of the market and shaping industry progress.

- Elbit Systems

- General Dynamics Ordnance & Tactical Systems

- Thales

- Rheinmetall

- Nexter (KNDS)

- Nammo

- BAE Systems

- Eurenco

- PGZ

- MSM Group

Market News & Updates

- Rheinmetall, 2026:

Rheinmetall announced a seven-year Danish framework agreement covering multiple ammunition classes including 155mm artillery ammunition, with initial call-offs described in the three-digit million-euro range and a signing ceremony on 30 January 2026; for the European 155mm market, this is a clear demand signal that reinforces multi-year procurement behavior among NATO/EU customers, supports suppliers’ willingness to lock in raw materials and expand lines, and can tighten near-term availability/pricing as framework-driven call-offs convert into firm production slots across Europe’s already constrained artillery-ammunition industrial base.

- Rheinmetall, 2025:

Rheinmetall’s “Plant Lower Saxony” materials (Unterlüß) outline a step-change in sovereign European 155mm output, targeting capacity of up to 25,000 rounds in 2025, 140,000 rounds/year in 2026, and up to 350,000 rounds/year in 2027, with production ramp starting via LAP in Q2/2025 and shell production in Q3/2025, alongside ~€500m total investment and a large jobs footprint; market-wide, this is one of the most material European capacity additions because it vertically integrates key steps (shell manufacturing, explosive filling, finishing/packaging), which should progressively ease structural shortages and improve delivery certainty for European buyers—but only after the 2025–2026 ramp period during which demand continues to outpace supply.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Europe 155mm Artillery Shells Market Policies, Regulations, and Standards

4. Europe 155mm Artillery Shells Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Europe 155mm Artillery Shells Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Shell Type

5.2.1.1. High-Explosive (HE\HE-FRAG) Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Smoke Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Illumination Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Training/Practice Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Other Special-Purpose Shell- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Guidance

5.2.2.1. Unguided - Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Precision-Guided - Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Range Class

5.2.3.1. Standard Range - Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Extended Range - Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Assisted Range- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.1. Base Bleed- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.2. Rocket-Assisted (RAP)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Operational Use

5.2.4.1. Training Consumption- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Routine Peacetime Stockpile Replenishment- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Active Conflict Replenishment\Urgent Operational Demand- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Strategic Reserve\Surge Inventory Build- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Artillery Platform Type

5.2.5.1. Towed Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Self-Propelled Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Truck-Mounted Howitzers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Country

5.2.6.1. Germany

5.2.6.2. France

5.2.6.3. UK

5.2.6.4. Italy

5.2.6.5. Spain

5.2.6.6. Rest of Europe

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Germany 155mm Artillery Shells Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Shell Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Guidance- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Range Class - Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

7. France 155mm Artillery Shells Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Shell Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Guidance- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Range Class - Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

8. UK 155mm Artillery Shells Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Shell Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Guidance- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Range Class - Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

9. Italy 155mm Artillery Shells Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Shell Type- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Guidance- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Range Class - Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Operational Use - Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

10. Spain 155mm Artillery Shells Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Shell Type- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Guidance- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Range Class - Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Operational Use - Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Rheinmetall

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Nexter (KNDS)

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Nammo

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. BAE Systems

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Eurenco

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Elbit Systems

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. General Dynamics Ordnance & Tactical Systems

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Thales

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. PGZ

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. MSM Group

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Shell Type |

|

| By Guidance |

|

| By Range Class |

|

| By Operational Use |

|

| By Artillery Platform Type |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.