Egypt Analgesics Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Systemic Analgesics (Adult Analgesics, Paediatric Analgesics, Combined Systemic Analgesics), Topical Analgesics/Anaesthetic), By Drug Type (Opioid Analgesics (Strong Opioids, Weak Opioids), Non-opioid Analgesics (Acetaminophen, Aspirin, Combination Products, Diclofenac, Dipyrone, Ibuprofen, Ketoprofen, Naproxen, OTC Triptans), Compound/Combination Analgesics (Opioid + Non-Opioid Combinations, Multi-Ingredient Non-Opioid Combinations)), By Route of Administration (Oral, Parenteral/Injectable, Topical/External, Transdermal, Rectal/Other), By Pain Type (Acute Pain, Chronic Pain, Breakthrough Pain), By Application (Surgical & Post-operative Pain, Musculoskeletal Pain, Neuropathic Pain, Cancer Pain, Migraine/Headache, Dental Pain, Others), By Sales Channel (Retail Offline (Offline Pharmacies, Hospital Pharmacies), Retail Online (Online Pharmacies)), By Prescription Type (Prescription, OTC), By Formulation (Tablets, Capsules, Liquids, Injectables, Gels/Creams, Patches), By End User (Hospitals, Clinics/ASCs, Homecare), By Region (Cairo, Alexandria, Others) ... Read more

|

Major Players

|

Egypt Analgesics Market Statistics and Insights, 2026

- Market Size Statistics

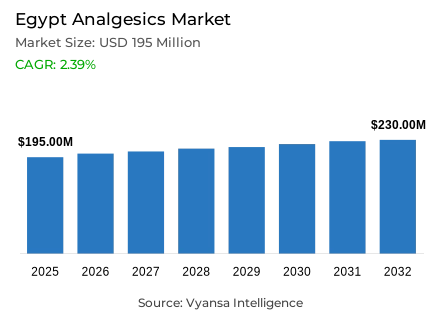

- Analgesics market size in Egypt was valued at USD 195 million in 2025 and is estimated at USD 205 million in 2026.

- The market size is expected to grow to USD 230 million by 2032.

- Market to register a CAGR of around 2.39% during 2026-32.

- Product Shares

- Systemic analgesics grabbed market share of 85%.

- Competition

- More than 20 companies are actively engaged in producing analgesics in Egypt.

- Top 5 companies acquired around 65% of the market share.

- Egyptian International Pharmaceutical Industries Co SAE (EIPICO), Amriya for Pharmaceutical Industries, Bayer Ltd Egypt LLC, GSK Consumer Healthcare, Abbott Laboratories Inc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Egypt Analgesics Market Outlook

Egypt analgesics market size was valued at USD 195 million in 2025 and is projected to grow from USD 205 million in 2026 to USD 230 million by 2032, exhibiting a CAGR of 2.39% during the forecast period. Growth is supported by the regular use of pain relief products for headaches, fever, muscle pain, and other day to day discomforts, along with steady access to these products through Egypt’s licensed pharmacy network.

Demand remains supported by the wide availability of medicines through pharmacies and the country’s large consumer base. Easy access keeps pain relief products visible for routine healthcare needs, while the formal retail system continues to strengthen medicine availability across the country. This supports frequent and practical use of analgesics in daily self care, especially for common pain conditions that do not always require immediate clinical treatment.

By product, systemic analgesics hold the leading share at around 85%, supported by their familiar use, simple administration, and strong household acceptance for everyday pain management. At the same time, affordability remains an important factor shaping buying behavior, as inflation and cautious household spending keep consumers focused on price, pack size, and lower cost options when purchasing routine healthcare products.

By sales channel, retail offline continues to dominate with 90% market share, as physical pharmacies remain the main purchase point for immediate and regular medicine needs. Trust in pharmacist interaction, quick walk in access, and strong retail presence keep this channel ahead. Alongside this, digital connectivity is becoming more visible in medicine purchasing, helping analgesics gain wider online visibility and supporting a more convenient omnichannel path for consumers across the country.

Egypt Analgesics Market Growth DriverBroad Pharmacy Reach Supports Everyday Pain Relief

Easy access to medicines through licensed pharmacies continues to support analgesics demand in Egypt. A large consumer base and steady pharmacy availability keep pain relief products visible for daily needs such as headache, fever, muscle pain, and other routine discomfort. This matters in a country where the population clock reaches 108,865,807 on 31 March 2026, making quick access OTC categories important in everyday healthcare buying.

The pharmacy system is also expanding in a formal and regulated way. The Egyptian Drug Authority says it carried out more than 7,200 licensing procedures for pharmacies, drug stores, and storage outlets during 2025, issued 2,343 new licenses for public and private pharmacies and affiliated storage outlets, and granted 49,860 professional and administrative certificates for pharmacists. This wider legal access supports regular analgesics purchases across the country.

Egypt Analgesics Market ChallengeHousehold Budget Pressure Limits Brand Expansion

Affordability remains a clear challenge in Egypt because routine healthcare purchases are still sensitive to changes in household spending. Analgesics are bought frequently, so even small price movements can affect brand choice, pack size, and repeat buying. This keeps the category exposed to downtrading, especially where consumers compare low cost options more closely before purchase.

Official data reflects that pressure. Central Agency for Public Mobilization and Statistics (CAPMAS) shows that monthly inflation rises 1.3% in October 2025, while unemployment stands at 6.1% in Q2 2025. In this environment, buyers stay cautious on everyday medicine spending, which makes it harder for higher priced analgesics to build stronger momentum. Price remains a practical decision point across both urban and lower income consumer groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Analgesics Market TrendDigital Access Starts Shaping Purchase Behavior

Digital connectivity is becoming more visible in medicine purchasing across Egypt. As consumers spend more time on mobile internet and home broadband, product discovery, ordering, and refill behavior are becoming easier across healthcare categories. This supports a gradual shift toward more convenient and faster access models, especially for OTC products that do not require a complex buying journey.

The communications data shows why this pattern is strengthening. The Ministry of Communications and Information Technology reports 12.18 million active fixed broadband subscriptions in April–June 2025, 88.51 million data and voice mobile broadband subscriptions, and 117.52 million mobile subscriptions, with mobile penetration at 106.66%. This stronger digital base supports wider online visibility and easier omnichannel access for analgesics.

Egypt Analgesics Market OpportunityFaster Formalization Opens New Room for Distribution

A stronger formal pharmacy system creates room for wider OTC reach in Egypt. As more pharmacies and related outlets move through organized licensing and digital service channels, analgesics can benefit from better retail presence, smoother replenishment, and more consistent availability. This matters for products that depend on repeat purchases and fast access at neighborhood level.

The Egyptian Drug Authority says it launched its Electronic Services Platform during 2025 and processed 2,700 ownership transfer licenses, 793 engineering drawing amendment licenses, and 396 warehouse license renewals, alongside the new pharmacy licenses issued during the year. This formal expansion creates a clearer opening for broader distribution and stronger availability of commonly used pain relief products across the retail system.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Egypt Analgesics Market Segmentation Analysis

By Product

- Systemic Analgesics

- Adult Analgesics

- Paediatric Analgesics

- Combined Systemic Analgesics

- Topical Analgesics/Anaesthetic

The segment with the highest share under the product is systemic analgesics, holding around 85% of the Egypt analgesics market in value terms. This segment remains ahead because oral pain relief products are the most familiar choice for headaches, fever, muscle pain, and other day to day discomforts. Their simple use and broad household acceptance keep them central to routine self care across the country.

Systemic analgesics continue to lead because they match fast and practical pain management needs and remain widely available through Egypt’s licensed pharmacy network. The Egyptian Drug Authority completed more than 7,200 licensing procedures in 2025 and issued 2,343 new licenses for pharmacies and affiliated storage outlets, helping keep commonly used pain relief products visible and easy to access in daily retail buying.

By Sales Channel

- Retail Offline

- Offline Pharmacies

- Hospital Pharmacies

- Retail Online

- Online Pharmacies

The segment with the highest share under the sales channel is retail offline with 90%, and this channel continues to dominate the Egypt analgesics market in value terms. Physical pharmacies remain the main purchase point because consumers still rely on quick availability, pharmacist interaction, and easy walk in access when buying pain relief products for immediate or regular use.

Retail offline stays ahead because Egypt continues to strengthen pharmacy professionalism and consumer oversight across the medicine retail system. In 2025, the Egyptian Drug Authority issued 49,860 professional and administrative certificates for pharmacists and handled 5,364 complaints and inquiries with rapid response. This stronger professional support and regulatory follow up help keep store based medicine access trusted and active across the country.

List of Companies Covered in Egypt Analgesics Market

The companies listed below are highly influential in the Egypt analgesics market, with a significant market share and a strong impact on industry developments.

- Egyptian International Pharmaceutical Industries Co SAE (EIPICO)

- Amriya for Pharmaceutical Industries

- Bayer Ltd Egypt LLC

- GSK Consumer Healthcare

- Abbott Laboratories Inc

- Novartis Egypt (Healthcare) SAE

- Chemical Industries Development (CID)

- Alexandria Co for Pharmaceuticals & Chemical Industries

- Misr for Pharmaceutical Industries

- Julphar Gulf Pharmaceuticals

Competitive Landscape

In 2025, analgesics in Egypt recorded robust growth driven by strong consumer reliance on self-medication for both common and chronic pain, with widespread use of single-ingredient products such as acetaminophen and ibuprofen, alongside rising demand for combination analgesics offering more effective relief. GSK Consumer Healthcare led the market with a 38.1% value share, supported by strong brands like Panadol, Voltaren, and Cataflam, benefiting from high consumer trust and broad accessibility, while Abbott Laboratories Inc followed with a 15.2% share, driven by its Brufen brand despite increasing competitive pressure. Purchasing behaviour varied between urban and rural consumers, with affordability influencing brand choice, while pharmacies remained the dominant channel although e-commerce continued to expand, supporting convenience and accessibility, and overall growth was reinforced by rising chronic pain prevalence, ageing demographics, and increasing awareness of pain management solutions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Egypt Analgesics Market Policies, Regulations, and Standards

- Egypt Analgesics Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Egypt Analgesics Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Systemic Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Adult Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Combined Systemic Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Topical Analgesics/Anaesthetic- Market Insights and Forecast 2022-2032, USD Million

- Systemic Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Drug Type

- Opioid Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Strong Opioids- Market Insights and Forecast 2022-2032, USD Million

- Weak Opioids- Market Insights and Forecast 2022-2032, USD Million

- Non-opioid Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Combination Products- Market Insights and Forecast 2022-2032, USD Million

- Diclofenac- Market Insights and Forecast 2022-2032, USD Million

- Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Ketoprofen- Market Insights and Forecast 2022-2032, USD Million

- Naproxen- Market Insights and Forecast 2022-2032, USD Million

- OTC Triptans- Market Insights and Forecast 2022-2032, USD Million

- Compound/Combination Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Opioid + Non-Opioid Combinations- Market Insights and Forecast 2022-2032, USD Million

- Multi-Ingredient Non-Opioid Combinations- Market Insights and Forecast 2022-2032, USD Million

- Opioid Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Route of Administration

- Oral- Market Insights and Forecast 2022-2032, USD Million

- Parenteral/Injectable- Market Insights and Forecast 2022-2032, USD Million

- Topical/External- Market Insights and Forecast 2022-2032, USD Million

- Transdermal- Market Insights and Forecast 2022-2032, USD Million

- Rectal/Other- Market Insights and Forecast 2022-2032, USD Million

- By Pain Type

- Acute Pain- Market Insights and Forecast 2022-2032, USD Million

- Chronic Pain- Market Insights and Forecast 2022-2032, USD Million

- Breakthrough Pain- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Surgical & Post-operative Pain- Market Insights and Forecast 2022-2032, USD Million

- Musculoskeletal Pain- Market Insights and Forecast 2022-2032, USD Million

- Neuropathic Pain- Market Insights and Forecast 2022-2032, USD Million

- Cancer Pain- Market Insights and Forecast 2022-2032, USD Million

- Migraine/Headache- Market Insights and Forecast 2022-2032, USD Million

- Dental Pain- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Offline Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type

- Prescription- Market Insights and Forecast 2022-2032, USD Million

- OTC- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquids- Market Insights and Forecast 2022-2032, USD Million

- Injectables- Market Insights and Forecast 2022-2032, USD Million

- Gels/Creams- Market Insights and Forecast 2022-2032, USD Million

- Patches- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics/ASCs- Market Insights and Forecast 2022-2032, USD Million

- Homecare- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Cairo

- Alexandria

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Egypt Systemic Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Drug Type- Market Insights and Forecast 2022-2032, USD Million

- By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

- By Pain Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Topical Analgesics/Anaesthetic Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Drug Type- Market Insights and Forecast 2022-2032, USD Million

- By Route of Administration- Market Insights and Forecast 2022-2032, USD Million

- By Pain Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Prescription Type- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Novartis Egypt (Healthcare) SAE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chemical Industries Development (CID)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alexandria Co for Pharmaceuticals & Chemical Industries The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Egyptian International Pharmaceutical Industries Co SAE (EIPICO)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amriya for Pharmaceutical Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Ltd Egypt LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Misr for Pharmaceutical Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Julphar Gulf Pharmaceuticals

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Drug Type |

|

| By Route of Administration |

|

| By Pain Type |

|

| By Application |

|

| By Sales Channel |

|

| By Prescription Type |

|

| By Formulation |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.