Global Clinical Laboratory Services Market Report: Trends, Growth and Forecast (2026-2032)

By Test Type (Clinical Chemistry (Routine Chemistry Testing, Therapeutic Drug Monitoring Testing, Endocrinology Chemistry Testing, Specialized Chemistry Testing, Other Clinical Chemistry Testing), Hematology Testing, Medical Microbiology (Infectious Disease Testing, Transplant Diagnostic Testing, Other Microbiology Testing), Immunology & Serology Testing, Molecular Diagnostics, Genetic Testing, Pathology (Cytopathology, Histopathology), Blood Banking & Transfusion Services, Toxicology & Drug Abuse Testing, Other Specialty/Esoteric Tests), By Service Provider (Hospital-based Laboratories, Independent/Standalone Clinical Laboratories, Clinic/Physician Office Laboratories, Public Health Laboratories, Specialty Laboratories), By Application (Routine Diagnostic Testing, Chronic Disease Testing, Infectious Disease Testing, Oncology Testing, Preventive/Screening Testing, Specialized/Genetic Testing), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Clinical Laboratory Services Market Statistics and Insights, 2026

- Market Size Statistics

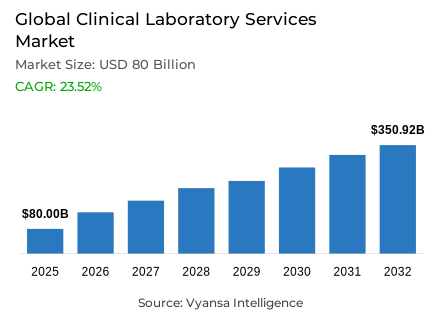

- Clinical laboratory services market size in Global was valued at USD 80 billion in 2025 and is estimated at USD 198 billion in 2026.

- The market size is expected to grow to USD 350.92 billion by 2032.

- Market to register a CAGR of around 23.52% during 2026-32.

- Test Type Shares

- Clinical chemistry grabbed market share of 25%.

- Competition

- More than 25 companies are actively engaged in producing clinical laboratory services.

- Top 5 companies acquired around 15% of the market share.

- Unilabs, Cerba HealthCare, Mayo Clinic Laboratories, Labcorp, Quest Diagnostics etc., are few of the top companies.

- Service Provider

- Hospital-based laboratories grabbed 40% of the market.

- Region

- North America leads with a 40% share of the global market.

Global Clinical Laboratory Services Market Outlook

The Global clinical laboratory services market was valued at USD 80 billion in 2025, establishing a commercially dynamic and clinically well-anchored foundation within the world's most rapidly expanding diagnostic testing and precision medicine ecosystem. Projected to advance from USD 198 billion in 2026 to USD 350.92 billion by 2032, the sector registers a CAGR of 23.52% across the forecast horizon. This exceptional and structurally supported expansion trajectory reflects the convergence of escalating global disease burden recognition, the systematic advancement of diagnostic testing capabilities, and the deepening institutional commitment to diagnostic-driven clinical decision-making whose testing requirements are generating consistent and compounding adoption of advanced clinical laboratory services across hospitals, specialty diagnostic centers, and primary care environments worldwide. Growth is anchored in genuine clinical necessity and healthcare system imperative rather than discretionary service adoption, giving this market a commercial resilience that sustains consistent testing volume and laboratory infrastructure investment across diverse patient populations and healthcare delivery contexts.

The test architecture defining this market's commercial structure is anchored in clinical chemistry methodologies. Clinical Chemistry commands approximately 25% of total test type market share, reflecting the consistent and deeply embedded clinical preference for chemistry-based analytical approaches whose versatility, diagnostic breadth, and established reliability make them the reference testing modality across routine disease evaluation, patient monitoring, and general health assessment workflows globally. This test concentration confirms that healthcare providers and clinical laboratories continue to prioritize proven, chemistry-based testing approaches whose performance credentials and methodological familiarity sustain disproportionate testing volume share across both primary care and specialist diagnostic applications within the global clinical laboratory services landscape.

The service provider architecture reinforces the structural centrality of hospital-based laboratories as the category's dominant delivery platform. Hospital-Based Laboratories account for approximately 40% of total service provider market share, reflecting the foundational role of integrated hospital laboratory systems in supporting high patient volumes, enabling rapid diagnostic turnaround, and facilitating coordinated clinical care across acute care and specialty treatment environments globally. This provider concentration signals that hospital-anchored laboratory services remain the primary commercial driver of diagnostic testing volume globally, where institutional clinical demands, integrated care workflows, and immediate testing access generate the highest-value and most strategically important laboratory service procurement activity.

The future outlook is defined by four converging structural forces whose combined commercial impact creates a clinical laboratory services market of sustained and exceptionally strong expansion momentum. The World Health Organization's documentation of noncommunicable diseases accounting for 43 million deaths in 2021, representing 75% of non-pandemic-related global mortality, with cardiovascular diseases accounting for 19 million deaths and cancer at 10 million deaths, establishes the disease burden scale that sustains persistent institutional and clinical demand for advanced diagnostic testing across disease screening, diagnosis, and ongoing treatment monitoring. The WHO's documentation that approximately 70% of healthcare decisions are informed by diagnostic test results establishes the clinical centrality of laboratory testing to contemporary medical practice and the structural demand foundation that sustains continuous testing volume expansion. The WHO's documentation that an estimated 4.7 billion people worldwide still lack access to safe, affordable, quality-assured diagnostic services establishes the global access gap opportunity whose closure through expanded laboratory service deployment will sustain market growth across diverse geographic and economic contexts. The FDA's AI-Enabled Medical Device List documentation of 1,430 entries current as of March 4, 2026, combined with the WHO's April 2025 update to tuberculosis diagnosis guidelines introducing two new TB diagnostic technology classes, confirms the accelerating pace of diagnostic methodology innovation whose implementation requires expanded laboratory infrastructure and advanced testing capability deployment over the forecast period.

Global Clinical Laboratory Services Market Growth Driver

Escalating Global Disease Burden Sustains Diagnostic Testing Necessity

The escalating and institutionally documented global burden of noncommunicable diseases represents the primary structural driver of clinical laboratory services demand, functioning as a persistent clinical and institutional testing imperative that sustains consistent diagnostic testing volume, laboratory infrastructure investment, and testing capability expansion across both developed and emerging healthcare systems worldwide. This disease burden-driven demand dynamic transcends healthcare budget cycle fluctuations, reflecting a durable clinical necessity whose testing volume generation is structurally anchored in the irreducible requirement for diagnostic confirmation, disease monitoring, and treatment response assessment that advanced laboratory testing enables across the full spectrum of patient populations.

The quantitative evidence validating this disease burden-driven demand dynamic is documented with precision by the World Health Organization and global health surveillance organizations. The WHO documents that noncommunicable diseases accounted for 43 million deaths in 2021, representing 75% of non-pandemic-related global mortality, with cardiovascular diseases accounting for 19 million deaths and cancer accounting for 10 million deaths. The WHO further documents that approximately 70% of healthcare decisions rely on diagnostic test results, confirming that laboratory testing has become central to contemporary clinical decision-making across all major disease categories and patient populations. These disease and testing metrics validate a diagnostic demand foundation of sufficient global scale and clinical urgency to sustain structural clinical laboratory services market growth over the forecast period.

Global Clinical Laboratory Services Market Challenge

Uneven Diagnostic Access Creates Global Capacity Constraints

The substantial global disparity in diagnostic testing access and laboratory service availability represents the most consequential structural challenge confronting the clinical laboratory services market, creating systematic expansion constraints and commercial accessibility barriers that moderate market expansion beyond developed healthcare systems and limit the breadth of patient populations that advanced diagnostic testing can serve across lower-resource healthcare environments. In a healthcare environment where laboratory testing has become central to clinical decision-making yet remains inaccessible to billions of people globally, the unmet diagnostic opportunity carries both significant public health implications and substantial market expansion potential whose realization depends on systemic infrastructure investment and service delivery model innovation.

The structural depth and geographic breadth of this diagnostic access challenge are quantified with precision by the World Health Organization and global health surveillance data. The WHO documents that an estimated 4.7 billion people worldwide still cannot access safe, affordable, quality-assured diagnostic services, confirming that diagnostic access remains deeply unequal across global health systems and geographies. The WHO further documents that although approximately 70% of healthcare decisions rely on diagnostic test results, only 3% to 5% of healthcare budgets are allocated to diagnostic services, and many clinicians still lack access to basic laboratory tests. This funding and access disparity creates a structural opportunity for clinical laboratory services providers investing in affordable, scalable, and evidence-based diagnostic solutions designed specifically for lower-resource and emerging healthcare environments over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Clinical Laboratory Services Market Trend

AI-Enabled Diagnostics Reshape Laboratory Workflow and Clinical Integration

The accelerating integration of artificial intelligence and advanced digital tools into diagnostic testing workflows represents the defining structural trend reshaping clinical laboratory services design priorities, analytical platform expectations, and competitive differentiation parameters across the global market. This artificial intelligence integration trend is progressively transforming the functional role of clinical laboratory services from standalone diagnostic reporting into intelligent clinical decision support, where AI-enabled result interpretation, predictive analytics, and integrated clinical guidance enhance the value of laboratory testing beyond traditional analytical reporting.

The institutional momentum and regulatory specificity of this artificial intelligence integration trend are documented with authority by the FDA and the World Health Organization. The FDA's AI-Enabled Medical Device List documentation of 1,430 entries current as of March 4, 2026 confirms that software-led and AI-supported diagnostic tools are advancing at an accelerating pace into clinical deployment, creating institutional expectations for intelligent diagnostic interpretation alongside traditional analytical capability. The WHO's April 2025 update to tuberculosis diagnosis guidelines introducing two new diagnostic technology classes and expanded sample testing recommendations confirms that international clinical practice is progressively incorporating advanced diagnostic methodologies whose implementation depends on laboratory infrastructure and testing sophistication. As artificial intelligence becomes more deeply integrated into diagnostic workflows and institutional expectations for intelligent decision support advance, clinical laboratory providers whose platforms support AI-enabled interpretation will capture disproportionate share of healthcare system investment over the forecast period.

Global Clinical Laboratory Services Market Opportunity

Essential Diagnostics Expansion Creates Structured Service Growth Pathways

The formal expansion of essential in-vitro diagnostics at national and global levels creates a structurally significant and commercially compelling opportunity for clinical laboratory services providers whose capabilities align with the specific diagnostic needs and quality standards established by the WHO Model List of Essential In Vitro Diagnostics and national essential diagnostics lists. This essential diagnostics opportunity is distinguished from routine diagnostic demand by its policy backing, its international standardization framework, and its direct alignment with government health priorities whose implementation timelines create predictable procurement pipelines and service expansion requirements across diverse healthcare contexts.

The quantitative scale and policy-implementation specificity of this essential diagnostics opportunity are documented with precision by the World Health Organization. The WHO's 2025 update to the Model List of Essential In Vitro Diagnostics adds therapeutic drug monitoring tests for methotrexate, phenytoin, and lithium, alongside 13 additional tests including monoclonal gammopathy screening, Clostridioides difficile, lead, Bordetella pertussis, testosterone, and hepatitis D virus diagnostics. The WHO further documents that by December 2024, seven countries had published national essential diagnostics lists, while 26 additional countries were actively developing national lists by May 2025. This progressive national adoption creates a policy-backed demand expansion framework whose implementation will require systematic laboratory infrastructure investment, testing capability development, and diagnostic service standardization across diverse healthcare systems. For clinical laboratory services providers that invest in essential diagnostics capability, quality assurance infrastructure, and developing-market service delivery models, this policy-supported diagnostic expansion represents a commercially attractive and structurally guaranteed growth opportunity over the forecast period.

Global Clinical Laboratory Services Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

The segment with highest market share under the Region is North America, accounting for approximately 40% of the total market. This dominant regional position reflects the convergence of the world's highest per-capita healthcare spending base, the most sophisticated diagnostic testing infrastructure, the largest concentration of advanced laboratory technology deployment, and a healthcare environment whose clinical standards and reimbursement frameworks systematically favor diagnostic testing adoption across all patient populations and care settings. With two-fifths of total global market value concentrated within a single regional block, North America defines the commercial scale, innovation direction, and competitive positioning parameters of the global clinical laboratory services market.

The structural dominance of North America is sustained by healthcare spending and testing utilization operating across multiple commercial dimensions simultaneously. The Centers for Medicare and Medicaid Services' documentation of healthcare spending growth of 7.2% reaching USD 5.3 trillion in 2024, with hospital expenditures reaching USD 1,634.7 billion and physician and clinical services reaching USD 1,109.7 billion, establishes the healthcare spending scale that sustains continuous and high-volume clinical laboratory services demand across North American healthcare systems. The FDA's AI-Enabled Medical Device List documentation of 1,430 entries current as of March 2026 confirms that advanced diagnostic innovation is concentrated within North America's regulatory and commercial environment, attracting continuous technology investment and early-stage methodology adoption. North America's structural leadership as the global market's dominant demand center and highest-value innovation hub is expected to remain intact over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Clinical Laboratory Services Market Segmentation Analysis

By Test Type

- Clinical Chemistry

- Routine Chemistry Testing

- Therapeutic Drug Monitoring Testing

- Endocrinology Chemistry Testing

- Specialized Chemistry Testing

- Other Clinical Chemistry Testing

- Hematology Testing

- Medical Microbiology

- Infectious Disease Testing

- Transplant Diagnostic Testing

- Other Microbiology Testing

- Immunology & Serology Testing

- Molecular Diagnostics

- Genetic Testing

- Pathology

- Cytopathology

- Histopathology

- Blood Banking & Transfusion Services

- Toxicology & Drug Abuse Testing

- Other Specialty/Esoteric Tests

The segment with highest market share under the Test Type is Clinical Chemistry, accounting for approximately 25% of the total market. This commanding position reflects the deep structural alignment between clinical chemistry testing capabilities and the specific diagnostic requirements of the global healthcare community, where routine chemistry-based analysis supports general disease evaluation, treatment monitoring, and comprehensive patient assessment across primary care, specialist care, and hospital-based clinical environments. With one-quarter of total market value concentrated within a single test category, Clinical Chemistry defines the testing methodology priorities, laboratory infrastructure investment frameworks, and competitive positioning strategies of the global clinical laboratory services market.

The structural leadership of Clinical Chemistry is sustained by the diagnostic versatility and methodological maturity that have established chemistry-based testing as the gold standard for routine clinical assessment across diverse patient populations and healthcare settings worldwide. As precision medicine research advances and disease-specific diagnostic algorithms become more sophisticated, clinical chemistry platforms are progressively evolving to support expanded analyte menus, improved measurement accuracy, and more seamless integration with specialized testing modalities. This methodological evolution positions established clinical chemistry laboratory providers to capture both sustained testing volume from routine care and expanding diagnostic breadth from emerging precision medicine applications. The segment's structural dominance as the market's primary test type revenue contributor is expected to consolidate over the forecast period.

By Service Provider

- Hospital-based Laboratories

- Independent/Standalone Clinical Laboratories

- Clinic/Physician Office Laboratories

- Public Health Laboratories

- Specialty Laboratories

The segment with highest market share under the Service Provider is Hospital-Based Laboratories, accounting for approximately 40% of the total market. This dominant position reflects the foundational role of integrated hospital laboratory systems in supporting comprehensive patient care, enabling rapid diagnostic turnaround, and facilitating seamless coordination between laboratory testing and clinical treatment decisions across acute care, emergency, and specialty treatment environments globally. With two-fifths of total market value anchored in hospital-based service delivery, this provider segment defines the testing capacity requirements, laboratory technology standards, and service integration expectations that shape clinical laboratory services demand and supplier competitive advantage across the global market.

The structural leadership of Hospital-Based Laboratories is being actively sustained by the accelerating institutional emphasis on integrated care delivery and the clinical imperative for immediate diagnostic access that characterizes contemporary hospital operations across developed and emerging healthcare systems. Hospitals' combination of high patient volume, urgent testing requirements, specialist care coordination, and integrated medical record systems creates testing demand conditions that consistently favor centralized laboratory infrastructure over decentralized testing models. As diagnostic methodology advances and disease complexity deepens, hospital laboratories are progressively investing in advanced instrumentation, specialized testing capability, and data integration infrastructure that position them to capture expanding shares of specialist and complex diagnostic testing. The Hospital-Based Laboratories segment's position as the market's dominant service provider anchor and primary revenue driver is expected to strengthen over the forecast period.

Market Players in Global Clinical Laboratory Services Market

These market players maintain a significant presence in the Global clinical laboratory services market sector and contribute to its ongoing evolution.

- Unilabs

- Cerba HealthCare

- Mayo Clinic Laboratories

- Labcorp

- Quest Diagnostics

- Eurofins Scientific

- Sonic Healthcare

- SYNLAB

- ARUP Laboratories

- KingMed Diagnostics

- ADICON

- BGI Genomics/BGI Group

- Dasa

- Dr Lal PathLabs

- Agilus Diagnostics

Market News & Updates

- Labcorp, 2026:

Labcorp launched the first FDA-cleared blood test for Alzheimer’s disease assessment in primary care, making the test available nationwide for symptomatic patients aged 55 and older. For the global clinical laboratory services market, this is a major service innovation because it expands blood-based neurodiagnostic testing from specialist settings into broader routine-care pathways, improving access and raising the bar for clinically deployable lab-led dementia assessment services.

- Quest Diagnostics, 2026:

Quest Diagnostics launched a flow cytometry minimal residual disease blood test for multiple myeloma, which the company said delivers sensitivity comparable to next-generation sequencing while also offering five-day specimen stability. This is a meaningful market upgrade because it improves the practicality of advanced oncology monitoring in real-world lab networks by making high-sensitivity myeloma testing easier to transport, process, and scale.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Clinical Laboratory Services Market Policies, Regulations, and Standards

- Global Clinical Laboratory Services Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- Routine Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic Drug Monitoring Testing- Market Insights and Forecast 2022-2032, USD Million

- Endocrinology Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Clinical Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Hematology Testing- Market Insights and Forecast 2022-2032, USD Million

- Medical Microbiology- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Transplant Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Microbiology Testing- Market Insights and Forecast 2022-2032, USD Million

- Immunology & Serology Testing- Market Insights and Forecast 2022-2032, USD Million

- Molecular Diagnostics- Market Insights and Forecast 2022-2032, USD Million

- Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Cytopathology- Market Insights and Forecast 2022-2032, USD Million

- Histopathology- Market Insights and Forecast 2022-2032, USD Million

- Blood Banking & Transfusion Services- Market Insights and Forecast 2022-2032, USD Million

- Toxicology & Drug Abuse Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Specialty/Esoteric Tests- Market Insights and Forecast 2022-2032, USD Million

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Independent/Standalone Clinical Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Clinic/Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Public Health Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Specialty Laboratories- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Routine Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Chronic Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Oncology Testing- Market Insights and Forecast 2022-2032, USD Million

- Preventive/Screening Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized/Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Test Type

- Market Size & Growth Outlook

- North America Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- US Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

- Brazil Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Colombia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- France

- Spain

- Italy

- Netherlands

- Rest of Europe

- Germany Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- UAE

- South Africa

- Egypt

- Rest of Middle East & Africa

- Saudi Arabia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- Australia

- South Korea

- Thailand

- Indonesia

- Singapore

- Rest of Asia Pacific

- China Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Labcorp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quest Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eurofins Scientific

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sonic Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SYNLAB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unilabs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cerba HealthCare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mayo Clinic Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ARUP Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KingMed Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ADICON

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BGI Genomics/BGI Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dasa

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dr Lal PathLabs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agilus Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Labcorp

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Test Type |

|

| By Service Provider |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.