China Room Air Conditioners Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Split Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Window Air Conditioners (Up to 9,000 BTU/h, 9,001-12,000 BTU/h, 12,001-18,000 BTU/h, 18,001-24,000 BTU/h, Above 24,000 BTU/h), Others), By Technology (Inverter, Non-Inverter), By Price (Up to USD 300, USD 301 to USD 600, USD 601 to USD 1,000, Above USD 1,000), By End User (Residential (Individual Households, Apartments/Condominiums, Vacation/Secondary Homes), Commercial (Offices, Retail Stores/Showrooms, Hospitality, Healthcare Facilities, Educational Institutions, Small Commercial Establishments, Others)), By Sales Channel (Retail Online (Brand-Owned Websites/D2C, E-Commerce Marketplaces), Retail Offline (Exclusive Brand Stores, Multi-Brand Electronics & Appliance Stores, Specialty Stores, Hypermarkets/Supermarkets, Home Improvement Stores, Dealer/Distributor Network, Direct Sales/Institutional Sales, Local Independent Retailers)), By Refrigerant Type (R-32, R-410A, R-290, R-454B, Others), By Connectivity (Smart/Connected, Conventional/Non-Smart), By Energy Efficiency (1 Star, 2 Star, 3 Star, 4 Star, 5 Star), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Room Air Conditioners Market Statistics and Insights, 2026

- Market Size Statistics

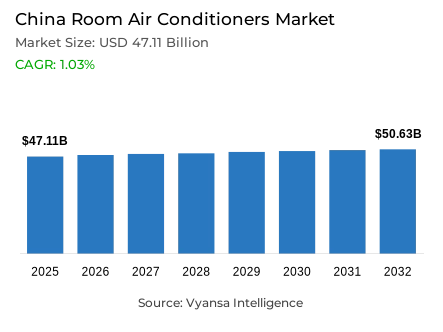

- Room air conditioners market size in China was valued at USD 47.11 billion in 2025 and is estimated at USD 48.6 billion in 2026.

- The market size is expected to grow to USD 50.63 billion by 2032.

- Market to register a CAGR of around 1.03% during 2026-32.

- Product Type Shares

- Split air conditioner grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing room air conditioners in China.

- Top 5 companies acquired around 80% of the market share.

- Hisense Group, AUX Group Co Ltd, Changhong Electric Co Ltd, Midea Group Co Ltd, Gree Electric Appliances Inc of Zhuhai etc., are few of the top companies.

- Technology

- Inverter grabbed 90% of the market.

China Room Air Conditioners Market Outlook

China room air conditioners market was estimated to be USD 47.11 billion in 2025 and it is projected to grow from USD 48.6 billion in 2026 to USD 50.63 billion by 2032, reflecting a CAGR of 1.03%. This trajectory indicates a large, mature market where expansion is driven by replacement cycles rather than rapid new demand creation. The category demonstrates long-term stability, supported by its essential role in household comfort.

The demand structure is very concentrated around mainstream residential patterns of use. Split room air conditioners account for approximately 90% of total product demand, reflecting a strong end-user preference for practical, easy-to-install solutions. This concentration indicates that the market is heavily anchored in standardized household cooling needs rather than diversified product experimentation. It also reinforces the dominance of proven formats in sustaining volume consistency.

Technology adoption is equally consolidated, with inverter systems representing nearly 90% of the market. This reflects strong prioritization of energy efficiency, smoother temperature control, and long-term operating cost savings among end users. As a result, inverter technology has transitioned from a premium feature to a baseline expectation. This shift elevates performance refinement and efficiency optimization as the primary competitive levers across manufacturers.

The market outlook remains stable through 2032, supported by replacement demand and efficiency-led upgrades. Value expansion from USD 48.6 billion in 2026 to USD 50.63 billion by 2032 reflects incremental growth rather than aggressive scaling. This indicates a category that continues to benefit from essential demand while evolving through technology improvement, policy alignment, and structured replacement cycles.

China Room Air Conditioners Market Growth Driver

Rising Heat Keeps Cooling Demand Activ

Rising temperature patterns remain the primary growth driver sustaining demand in China’s room air conditioners market. Increasing frequency and intensity of high-temperature days are making cooling a daily necessity rather than a seasonal convenience. This shift strengthens baseline demand as households require consistent indoor climate control. It also reinforces the role of air conditioners as essential appliances within urban living environments.

Climate data validates the structural strength of this demand driver. China’s average temperature reached 10.9°C in 2024, which is 1.01°C above normal and the highest since 1951. High-temperature days were above normal levels by 6.6 days, and it was the second highest since 1961. These conditions directly increase cooling requirements, supporting both replacement demand and first-time adoption in warmer regions through 2032.

China Room Air Conditioners Market Challenge

Housing Weakness Slows Fresh Installations

The main structural problem of the market is weak in the residential real estate sector. The first-time appliance installations are directly affected by new housing activity, which is a key driver of demand. Declines in new residential construction reduce opportunities for fresh air conditioner adoption. As a result, the market becomes increasingly dependent on replacement demand rather than expansion through new housing supply.

Housing data confirms the extent of this constraint across the market landscape. Floor space of newly built residential buildings sold declined by 14.1% in 2024, while sales value dropped by 17.6%. New residential construction starts also fell by 23.0%. These declines limit installation-linked demand and intensify competition for replacement cycles, creating a more constrained growth environment through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Room Air Conditioners Market Trend

Efficiency-Led Cooling Moves to the Forefront

Energy efficiency is becoming the new trend that is defining product development and competitive positioning. The regulatory frameworks and changing standards are driving manufacturers to more efficient technologies and better performance standards. This trend is an indication of the change in the growth based on volume to value based innovation that is geared towards sustainability and operating efficiency.

The structural significance of this transition is reinforced by policy developments. Revised energy-efficiency standards were presented in 2024 and apply to various product types and focus on meeting more stringent standards. An update to room air conditioner efficiency standards was also launched in April 2025 with a systematic development schedule. These efforts hasten the transition to more advanced inverter systems and more performance-oriented specifications, influencing the development of products up to 2032.

China Room Air Conditioners Market Opportunity

Trade-In Push Opens the Replacement Window

Government-supported appliance replacement programs present a significant opportunity for value expansion in the market. Trade-in programs motivate consumers to upgrade their old models with newer and more efficient models. This creates a pathway for manufacturers to drive premiumization and maintain the aggregate market demand. The opportunity is particularly relevant in a mature market where replacement cycles dominate growth dynamics.

Policy data highlights the scale of this opportunity across consumer engagement. Over 34.5 million consumers took part in appliance trade-in programmes in January-April 2025, buying more than 51.5 million units and making sales of 174.5 billion yuan. Additional support of 300 billion yuan in 2025 further strengthens this initiative. These programs enable brands to promote energy-efficient upgrades and capture higher-value demand up to 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Room Air Conditioners Market Segmentation Analysis

By Product Type

- Split Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Window Air Conditioners

- Up to 9,000 BTU/h

- 9,001-12,000 BTU/h

- 12,001-18,000 BTU/h

- 18,001-24,000 BTU/h

- Above 24,000 BTU/h

- Others

The segment with highest market share under the Product Type is Split Air Conditioner, accounting for approximately 90% of the total market. This leadership is indicative of a high degree of conformity to residential cooling needs, with split systems providing a performance, flexibility and installation convenience balance. Their ability to fit in with the normal home designs strengthens their use and thus they are the default option in most households.

This leadership also influences the competitive forces in the market. The split segment is where manufacturers focus on product development, pricing policies and feature improvements since it is the largest segment of demand. Consequently, innovation, differentiation, and marketing activities are highly focused on this category, which strengthens its position as the main standard of overall market performance up to 2032.

By Technology

- Inverter

- Non-Inverter

The segment with highest market share under the Technology is Inverter, accounting for approximately 90% of the total market. This leadership indicates high end-user preference in energy-efficient operation and constant temperature. Inverter systems save on electricity and enhance comfort, which makes them very compatible with regulatory requirements and household cost factors.

The dominance of the segment also shows that competition in technology has shifted to performance optimisation rather than adoption. Instead of marketing alternative technologies, manufacturers are concentrating on efficiency level refinement, cooling precision, and user experience in inverter systems. This makes inverter-based solutions the new standard of innovation, defining the future product development and end user expectations by 2032.

List of Companies Covered in China Room Air Conditioners Market

The companies listed below are highly influential in the China room air conditioners market, with a significant market share and a strong impact on industry developments.

- Hisense Group

- AUX Group Co Ltd

- Changhong Electric Co Ltd

- Midea Group Co Ltd

- Gree Electric Appliances Inc of Zhuhai

- Haier Group

- Xiaomi Corp

- TCL Corp

- Panasonic Corp

- Daikin Industries Ltd

Market News & Updates

- Xiaomi Corp, 2025:

Xiaomi’s official China store lists the “Ju Sheng Dian” 3HP Mijia Air Conditioner (2025) and related Pro models as 2025 room-AC launches, highlighting new-generation energy-saving positioning and super first-class energy efficiency in floor-standing formats. This is important for the China room air conditioners market because it strengthens Xiaomi’s push in smart, inverter-led residential cooling while expanding premium large-capacity options for living-room and apartment use.

- TCL Corp, 2025:

TCL’s official China design pages show the TCL Xiaolanyi P7 Ultra series air conditioners as a 2025 release, with the dated design-history entry on December 19, 2025 and the detailed story highlighting features such as AI sleep, double-circulation fresh air, negative-ion waterfall sterilization, and AI good-air mode. This is a meaningful market update because it shows TCL pushing room ACs beyond basic cooling into smart air-quality and comfort-led innovation for Chinese households.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Room Air Conditioners Market Policies, Regulations, and Standards

- China Room Air Conditioners Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Room Air Conditioners Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Product Type

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Window Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- Up to 9,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 9,001-12,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 12,001-18,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- 18,001-24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Above 24,000 BTU/h- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Split Air Conditioners- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Inverter- Market Insights and Forecast 2022-2032, USD Million

- Non-Inverter- Market Insights and Forecast 2022-2032, USD Million

- By Price

- Up to USD 300- Market Insights and Forecast 2022-2032, USD Million

- USD 301 to USD 600- Market Insights and Forecast 2022-2032, USD Million

- USD 601 to USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- Above USD 1,000- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Individual Households- Market Insights and Forecast 2022-2032, USD Million

- Apartments/Condominiums- Market Insights and Forecast 2022-2032, USD Million

- Vacation/Secondary Homes- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Offices- Market Insights and Forecast 2022-2032, USD Million

- Retail Stores/Showrooms- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Facilities- Market Insights and Forecast 2022-2032, USD Million

- Educational Institutions- Market Insights and Forecast 2022-2032, USD Million

- Small Commercial Establishments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites/D2C- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Exclusive Brand Stores- Market Insights and Forecast 2022-2032, USD Million

- Multi-Brand Electronics & Appliance Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Home Improvement Stores- Market Insights and Forecast 2022-2032, USD Million

- Dealer/Distributor Network- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales/Institutional Sales- Market Insights and Forecast 2022-2032, USD Million

- Local Independent Retailers- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type

- R-32- Market Insights and Forecast 2022-2032, USD Million

- R-410A- Market Insights and Forecast 2022-2032, USD Million

- R-290- Market Insights and Forecast 2022-2032, USD Million

- R-454B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity

- Smart/Connected- Market Insights and Forecast 2022-2032, USD Million

- Conventional/Non-Smart- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency

- 1 Star- Market Insights and Forecast 2022-2032, USD Million

- 2 Star- Market Insights and Forecast 2022-2032, USD Million

- 3 Star- Market Insights and Forecast 2022-2032, USD Million

- 4 Star- Market Insights and Forecast 2022-2032, USD Million

- 5 Star- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- Southwest

- Northwest

- North East

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- China Split Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Window Air Conditioners Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Price- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Insights and Forecast 2022-2032, USD Million

- By Connectivity- Market Insights and Forecast 2022-2032, USD Million

- By Energy Efficiency- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Midea Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Inc of Zhuhai

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haier Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xiaomi Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TCL Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AUX Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Changhong Electric Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Technology |

|

| By Price |

|

| By End User |

|

| By Sales Channel |

|

| By Refrigerant Type |

|

| By Connectivity |

|

| By Energy Efficiency |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.