China Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

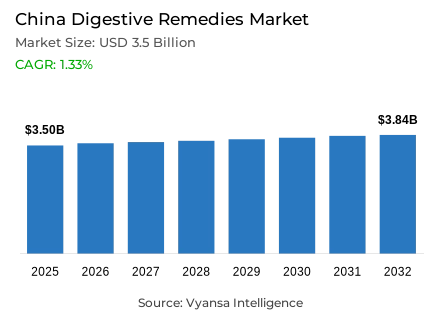

- Digestive remedies market size in China was valued at USD 3.5 billion in 2025 and is estimated at USD 3.68 billion in 2026.

- The market size is expected to grow to USD 3.84 billion by 2032.

- Market to register a CAGR of around 1.33% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing digestive remedies in China.

- Top 5 companies acquired around 25% of the market share.

- Bayer Healthcare Co Ltd, Yangtze River Pharmacy Co Ltd, AstraZeneca China Pharm Co Ltd, CR Jiangzhong Pharmaceutical Group Co Ltd, CR Sanjiu Medical & Pharmaceutical Co Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 65% of the market.

China Digestive Remedies Market Outlook

The China digestive remedies market size was valued at USD 3.5 billion in 2025 and is projected to grow from USD 3.68 billion in 2026 to USD 3.84 billion by 2032, exhibiting a CAGR of around 1.33% during the forecast period. Growth remains steady as digestive discomfort linked to modern lifestyles continues to affect a large share of the population. Sedentary routines, irregular meals, and higher consumption of processed and spicy foods contribute to indigestion, bloating, and irregularity. These factors sustain the routine use of fast-acting relief options such as antacids and antiflatulents, especially in convenient formats like chewables and granules that suit busy daily routines.

Demographic and urban changes also support long-term demand. The National Bureau of Statistics reports that people aged 60 and above account for 23.0% of the population by the end of 2025, while the urbanisation rate reaches 67.89%. These trends contribute to digestive discomfort associated with ageing and urban lifestyles, encouraging regular use of digestive remedies. Within product categories, indigestion and heartburn remedies hold the largest share at around 60%, reflecting the widespread occurrence of mild stomach discomfort and bloating that consumers often manage with accessible over-the-counter treatments.

At the same time, the category faces competition from preventive gut-health products. Probiotics and other wellness solutions are gaining wider recognition among middle-aged and older consumers, which may gradually reduce reliance on symptom-based treatments. According to the National Health Commission, China’s health literacy rate reaches 33.69% in 2025, rising by 1.82% points year on year. As awareness improves, some consumers increasingly focus on prevention and routine gut health management rather than depending solely on digestive remedies for relief.

Distribution patterns also continue to evolve. Pharmacies remain the main channel because consumers trust pharmacists for guidance and access to familiar brands, keeping retail offline dominant with about 65% share. However, online channels are expanding rapidly through livestreaming, AI-driven recommendations, and stronger platform visibility. The National Bureau of Statistics reports that online retail sales reach 9,982.8 billion yuan from January to August 2025, with online sales of physical goods accounting for 25.0% of total consumer goods retail sales, helping digital platforms become an increasingly important route for digestive remedies.

China Digestive Remedies Market Growth DriverUrban Lifestyles Keep Everyday Relief in Demand

One of the reasons why the Chinese market is growing in the digestive remedies is the ongoing increase in the number of lifestyle-related digestive discomfort. The lack of exercise, unhealthy eating habits, and the consumption of more processed and spicy food are all contributing to the occurrence of indigestion, bloating, and irregularity, which are in turn supporting the daily use of fast-acting digestive relief. Self-medication is on the rise, especially in convenient forms like antacids and antiflatulants, and chewable and granule forms improve absorption by becoming part of the daily routine.

This demand base is supported by the demographic and urban profile of China. The National Bureau of Statistics reports that the proportion of people aged 60 and above will reach 23.0% of the population by the end of 2025, while the urbanisation rate will rise to 67.89%. These statistics are in line with the larger strains of an ageing and urbanising society that still perpetuates digestive unease and a consistent need of relief products.

China Digestive Remedies Market ChallengePreventive Gut-Health Products Are Intensifying Competition

One of the threats facing the Chinese market of digestive remedies is the increasing competition of probiotics and other preventive gut-health products. Probiotics are no longer targeted at younger consumers, but are increasingly becoming popular among middle-aged and older adults. With the increasing number of consumers perceiving probiotics and natural formulations as safer, gentler and more appropriate to daily use, long-term dependence on the traditional OTC digestive remedies is being watered down.

The change is supported by the increased health awareness. The National Health Commission reports that China’s health literacy rate reached 33.69% in 2025, up 1.82% points year on year. The more consumers are informed on health management, the more they will opt to use preventive or wellness-based solutions before the symptoms become acute. This poses greater indirect competition to digestive remedies, particularly in those categories that are taken to provide long-term management as opposed to acute relief.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Digestive Remedies Market TrendDigital Buying Is Reshaping Category Access

One of the trends that are evident in the Chinese market of digestive remedies is the fast growth of digital access. The pharmacies are still the leading channel in terms of value, but the retail e-commerce is becoming more rapidly developed with livestreaming, AI-based recommendations, flash deals, and enhanced platform visibility. This simplifies the process of finding and buying digestive remedies, especially among younger urban consumers and users in lower-tier cities who are becoming more dependent on online health retail.

This trend is supported by official retail data. The National Bureau of Statistics reports that China’s online retail sales reached 9,982.8 billion yuan from January to August 2025, up 9.6% year on year. Within total retail sales, online retail sales of physical goods reached 8,096.4 billion yuan, accounting for 25.0% of total consumer goods retail sales. This electronic measure can be used to understand why online platforms are gaining more significance in OTC digestive remedies.

China Digestive Remedies Market OpportunityMild and Accessible Solutions Open the Clearest Growth Space

One of the opportunities in the Chinese market of digestive remedies is the availability of mild products that can be included in daily self-care. The demand on chewable antacids, herbal preparations, and other mild preparations is growing as the digital health awareness increases and more consumers opt to intervene earlier in the disease instead of waiting until it manifests in severe symptoms. The products are particularly well-positioned since they align with the increasing affordability, increased coverage in lower end cities, and the increasing consumer interest in milder digestive products.

The broader health-conscious development in China justifies this introduction. The National Health Commission reports that the national health literacy rate reached 33.69% in 2025, while the rate among urban residents rose to 36.68%. At the same time, the National Bureau of Statistics reports an urbanisation rate of 67.89% in 2025. Collectively, these numbers justify a larger market of available, self-managed digestive solutions that can be incorporated into daily health management.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share by product type within the category, with indigestion and heartburn remedies capturing 60% of the market. This top spot suggests that indigestion, bloating, and slight stomach pain are still prevalent in urban lifestyles and changing eating patterns. These products are core as consumers tend to find fast and convenient solutions to daily digestive problems and are already accustomed to the available forms of chewables and granules.

The split in consumer behaviour also works to the advantage of this segment. Herbal and TCM-based alternatives are commonly used in the case of long-term care, whereas non-herbal medications like antacids and H2 blockers are used in more urgent cases. That wide applicability continues to place indigestion and heartburn remedies in the middle of the digestive care demand.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share by sales channel, where retail offline accounts for 65% of the market. This indicates that pharmacies are still the most dominant channel of distribution in terms of value since consumers still trust pharmacists and use physical stores to access, consult and well-known brands of digestives. In the tier-2 and tier-3 cities, offline channels are also significant, as the presence of pharmacies and in-store trust still influence OTC buying behaviour.

Meanwhile, online shopping is growing rapidly.The National Bureau of Statistics reports that China’s online retail sales reach 9,982.8 billion yuan in the first eight months of 2025, showing how strongly digital channels are developing. Nevertheless, physical retail continues to dominate in the digestive remedies category since it is the most established point of sale of daily OTC relief.

List of Companies Covered in China Digestive Remedies Market

The companies listed below are highly influential in the China digestive remedies market, with a significant market share and a strong impact on industry developments.

- Bayer Healthcare Co Ltd

- Yangtze River Pharmacy Co Ltd

- AstraZeneca China Pharm Co Ltd

- CR Jiangzhong Pharmaceutical Group Co Ltd

- CR Sanjiu Medical & Pharmaceutical Co Ltd

- Jilin Xiuzheng Pharmaceutical Co Ltd

- Xian Janssen Pharmaceutical Ltd

- Zhejiang CONBA Pharmaceutical Co Ltd

- Livzon Pharmaceutical Group Inc

- Wellso Pharmaceutical Holding Co Ltd

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in China was led by CR Jiangzhong Pharmaceutical Group Co Ltd with an 8.5% retail value share, followed closely by CR Sanjiu Medical & Pharmaceutical Co Ltd with 8.2%. CR Jiangzhong maintains its leadership through well-established brands such as Jiangzhong and Jiangzhong Children's Jianwei Xiaoshi Pian, supported by strong distribution networks, pharmacy-level promotion and consumer trust in traditional Chinese medicine-based digestive solutions. However, the company is facing increasing pressure to refresh its product portfolio and accelerate innovation to sustain growth. Meanwhile, CR Sanjiu continues to strengthen its position through a diversified portfolio and strong presence in digestive healthcare products. The market is further shaped by growing demand for herbal and mild formulations, rising self-medication practices and the rapid expansion of retail e-commerce platforms, which are increasing accessibility and visibility of digestive remedies across urban and lower-tier city consumers.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Digestive Remedies Market Policies, Regulations, and Standards

- China Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- Southwest

- Northwest

- North East

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- China Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- CR Jiangzhong Pharmaceutical Group Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CR Sanjiu Medical & Pharmaceutical Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jilin Xiuzheng Pharmaceutical Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xian Janssen Pharmaceutical Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zhejiang CONBA Pharmaceutical Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Healthcare Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yangtze River Pharmacy Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AstraZeneca China Pharm Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Livzon Pharmaceutical Group Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wellso Pharmaceutical Holding Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CR Jiangzhong Pharmaceutical Group Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.