Chile Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)) ... Read more

|

Major Players

|

Chile Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

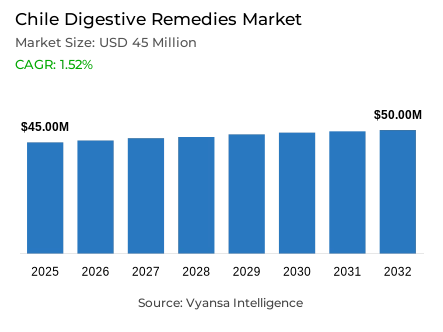

- Digestive remedies market size in Chile was valued at USD 45 million in 2025 and is estimated at USD 47 million in 2026.

- The market size is expected to grow to USD 50 million by 2032.

- Market to register a CAGR of around 1.52% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 45%.

- Competition

- More than 15 companies are actively engaged in producing digestive remedies in Chile.

- Top 5 companies acquired around 65% of the market share.

- Laboratorio Chile SA (LABCHILE), Laboratorio Esp Med Knop Ltda, Sanofi-Aventis de Chile SA, GlaxoSmithKline Chile Farmaceutica Ltda, Laboratorios Saval SA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Chile Digestive Remedies Market Outlook

The Chile digestive remedies market size was valued at USD 45 million in 2025 and is projected to grow from USD 47 million in 2026 to USD 50 million by 2032, exhibiting a CAGR of around 1.52% during the forecast period. Growth is supported by steady demand for products that provide relief from everyday digestive discomfort and support digestive wellness in routine self-care. Although expansion remains gradual, consistent use of over-the-counter solutions and the availability of trusted pharmacy products continue to support category stability during the forecast period.

Demand is supported by the growing overlap between ageing and everyday digestive discomfort. Consumers increasingly treat digestive health as part of overall wellbeing, while older adults remain more exposed to recurring stomach issues that require quick relief. According to the 2024 Census, people aged 65 or over represent 14% of the population, rising from 11.4% in 2017, confirming a clear ageing trend. The census also reports an ageing index of 79 older adults for every 100 people aged 14 or under, reinforcing the relevance of digestive remedies for consumers managing recurring digestive concerns in daily life.

Product demand remains strongly concentrated in solutions offering quick symptom relief. Indigestion & heartburn remedies hold about 45% of total sales, making them the largest product type in the category. Their leading position reflects the continued relevance of fast-acting treatments for common digestive discomfort, particularly during heavy meals and festive occasions. Familiarity, easy access, and immediate relief keep digestive remedies such as antacids widely used in routine self-care compared with newer or more specialised digestive solutions.

Distribution patterns also shape the outlook, with retail offline accounting for around 90% of total sales. Pharmacies remain the dominant purchase point because they provide trusted guidance, broad product availability, and immediate access to digestive remedies when symptoms occur. At the same time, omnichannel strategies are gradually expanding as online pharmacy platforms introduce delivery services, subscriptions, and digital promotions, while physical stores continue to anchor purchasing behaviour across the country.

Chile Digestive Remedies Market Growth DriverAgeing Lifestyles Keep Digestive Relief Relevant

One of the main forces of digestive remedies in Chile is the growing overlap between ageing and everyday digestive unease. Consumers are increasingly considering digestive health as part of the overall wellbeing, whilst older adults still face a disproportionate rate of recurrent gastrointestinal disorders that require quick, recognizable relief. At the same time, the category still enjoys the modern trends of eating out and the frequent use of antacids, proton pump inhibitors, and other modesty in suppressing the symptoms.

This demand base is supported by the demographic profile of Chile. According to the 2024 Census, individuals aged 65 or older comprise 14% of the population, an increase from 11.4% in 2017, thereby confirming a pronounced ageing trend. Another census also indicates an ageing index of 79 older adults per 100 individuals aged 14 or below in 2024. This older consumer group supports the need to have digestive aid in daily living.

Chile Digestive Remedies Market ChallengeNatural and Preventive Options Slow Traditional Self-Medication

One of the main issues of the digestive remedies in Chile is the slow transition of the traditional self-medication to the natural one and the increased focus on preventive health behaviours. Herb-based, probiotic, and holistic gut-health plans are becoming increasingly important, and more consumers are now seeking direct medical consultation instead of rushing to the over-the-counter symptomatic relief. This shift changes the growth curve of the category, with digestive remedies still being sold, but now facing more competition with less overt, preventive, and lifestyle-based solutions.

This pressure is further enhanced by a wider wellness culture where consumers are becoming more and more associated with digestive balance with dietary quality, routine, and prevention as opposed to treatment alone. Traditional over-the-counter digestive products are therefore facing a more complex market landscape. Their role is more than symptom relief, since they are now competing with products and practices that consumers consider more gentle, holistic, and consistent with long-term health care.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Digestive Remedies Market TrendDigital Pharmacy Access Is Reshaping the Purchase Journey

One of the visible trends in Chile is the growing popularity of retail e-commerce in digestive remedies. Pharmacy chains are constantly improving their omnichannel approaches, which makes online ordering, same-day delivery, subscription, and online promotions more visible. This change is altering consumer buying patterns in the over-the-counter digestive products, especially among younger buyers who are already skilled in the ability to compare products and buy through mobile apps or pharmacy websites.

The shift is strongly supported by the digital infrastructure of Chile. The 2025 Subtel internet survey indicates that 96.6% of households possess dedicated internet access, and 68.4% of internet users engage in e‑commerce activities online. In addition, the 2025 registry of approved electronic commerce by the ISP demonstrates a broad network of pharmacy-related digital sales channels that are already active in the country. These conditions explain why e-commerce is still taking off in digestive remedies.

Chile Digestive Remedies Market OpportunityTravel Recovery Opens Space for Motion Sickness Remedies

Another opportunity in Chile is in the motion sickness remedies, which is enabled by the increased travel activity. The more consumers travel by air, automobile, and sea to places like Patagonia, the Atacama Desert, and the Lake District, the more they are exposed to travel-related nausea and dizziness. This offers motion-sickness therapies with greater opportunities, especially as pharmacies increasingly become more accessible over-the-counter and consumer-awareness of travel-health requirements.

This development is supported by official tourism statistics. Sernatur reports 6,004,567 foreign tourist arrivals in 2025, representing a 14.61% increase from 2024. National Institute of Statistics (INE) additionally records 20,874,389 overnight stays in tourist accommodation in 2025, a 3.5% year‑on‑year growth, with December 2025 overnight stays alone rising 3.4%. This increased tourist traffic supports larger usage events of motion-sickness remedies in domestic and international travel.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Chile Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

Within the category, the section with the greatest share pertains to product type, with indigestion & heartburn remedies commanding 45% of that share. This leadership is in line with the current architecture of the category, where indigestion and heartburn are still key issues in Chile, especially in a market where consumers still value quick-acting relief to regular digestive discomfort. Antacids are still especially entrenched in local buying behavior and benefit through frequent use at large meals and celebrations.

This segment is strong due to its combination of familiarity, accessibility, and instant symptom relief. Compared to newer or more specialised digestive segments, remedies of indigestion and heartburn remain central elements of self-care. Their exaggerated role is indicative of a category where quick relief, cultural usage, and repetitive use still have a greater impact on purchasing behaviour than product novelty.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment commanding the highest share concerning sales channel is retail offline, which captures 90% of the market. This dominance reflects the pharmacy-based over-the-counter system in Chile, where licensed physical stores remain the main channel of distribution of digestive remedies. The strong consumer confidence, expert advice, wide product range, and wide geographic reach are advantages to pharmacies, which continue to support store-based purchasing as the primary channel despite the growing relevance of digital channels.

At the same time, offline leadership coexists with augmented omnichannel behaviour. Online pharmacy platforms are more often compared and reordered by consumers, but physical stores continue to be the reference point to the category, due to their ability to provide immediate access and their status as the most familiar place of purchase of digestive health products. This keeps the retail offline in a strong position, despite the growth of e-commerce surrounding it.

List of Companies Covered in Chile Digestive Remedies Market

The companies listed below are highly influential in the Chile digestive remedies market, with a significant market share and a strong impact on industry developments.

- Laboratorio Chile SA (LABCHILE)

- Laboratorio Esp Med Knop Ltda

- Sanofi-Aventis de Chile SA

- GlaxoSmithKline Chile Farmaceutica Ltda

- Laboratorios Saval SA

- Laboratorio Garden House SA

- Laboratorios Andromaco SA

- Laboratorio Maver Ltda

- Bayer de Chile SA

- Laboratorio Valma Ltda

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in Chile was led by GlaxoSmithKline Chile Farmaceutica Ltda with a 20.6% retail value share, followed by Laboratorios Saval SA with 14.6%. GlaxoSmithKline maintains its leadership mainly through well-established brands such as Gaviscon and Sal de Fruta Eno, which benefit from strong consumer recognition and consistent demand for antacids, particularly during festive periods when rich food and alcohol consumption lead to digestive discomfort. Meanwhile, Laboratorios Saval continues to gain ground by offering competitively priced bioequivalent medicines produced at its modern manufacturing facility, appealing to price-sensitive consumers seeking effective treatments for heartburn, indigestion and diarrhoea. Despite steady category growth, demand dynamics are gradually shifting as more consumers turn to natural remedies, herbal treatments and probiotic supplements for preventive digestive health, increasing competition for traditional OTC digestive remedies.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Chile Digestive Remedies Market Policies, Regulations, and Standards

- Chile Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Chile Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Chile Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GlaxoSmithKline Chile Farmaceutica Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorios Saval SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Garden House SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorios Andromaco SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Maver Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Chile SA (LABCHILE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Esp Med Knop Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis de Chile SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer de Chile SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorio Valma Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline Chile Farmaceutica Ltda

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.