Canada Weight Management and Wellbeing Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Meal Replacement Products (Shakes, Bars, Ready-to-Drink (RTD) Beverages, Powder Mixes), OTC Obesity Products (Fat Absorption Inhibitors, Appetite Suppressants, Metabolism Boosters), Supplement Nutrition Drinks, Slimming Teas, Weight Loss Supplements), By Application (Obesity Management, Diabetes-Associated Weight Control, Cardiovascular Risk Reduction, Post-Bariatric Surgery Weight Maintenance, General Fitness & Lifestyle Weight Control), By End User (Hospitals, Specialty & Bariatric Clinics, Weight Loss Centers, Homecare/Individual Consumers), By Sales Channel (Retail Offline (Pharmacies & Drug Stores, Supermarkets/Hypermarkets, Specialty Nutrition Stores), Retail Online (E-commerce Platforms, Brand-Owned Websites)) ... Read more

|

Major Players

|

Canada Weight Management and Wellbeing Market Statistics and Insights, 2026

- Market Size Statistics

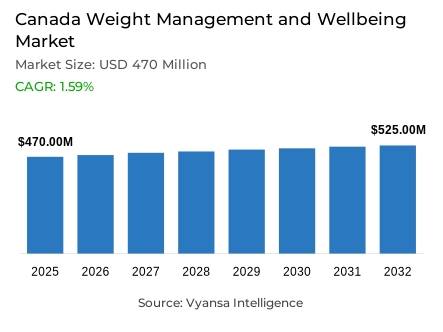

- Weight management and wellbeing market size in Canada was estimated at USD 470 million in 2025.

- The market size is expected to grow to USD 525 million by 2032.

- Market to register a CAGR of around 1.59% during 2026-32.

- Category Shares

- Supplement nutrition drinks grabbed market share of 70%.

- Competition

- More than 10 companies are actively engaged in producing weight management and wellbeing in Canada.

- Top 5 companies acquired around 75% of the market share.

- Iovate Health Sciences International Inc, Herbalife Nutrition Ltd, WN Pharmaceuticals Ltd, Abbott Laboratories Inc, Nestle Health Science SA etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Canada Weight Management and Wellbeing Market Outlook

The Canada weight management and wellbeing market size was valued at USD 470 million in 2025 and is expected to grow from USD 477 million in 2026 to USD 525 million by 2032, at a CAGR of approximately 1.59% from 2026 to 2032. The market growth in 2026 is driven by a high and rising prevalence of excess weight. Data from Statistics Canada’s Canadian Health Measures Survey, released October 2, 2025, indicates that 68% of adults aged 18-79 are overweight or living with obesity, with 33% obesity prevalence, and 31% of children and youth aged 5-17 are overweight/obese. Further, 49% of adults have a waist circumference above abdominal obesity thresholds.This sustains everyday demand within weight management and wellbeing for practical, non-prescription nutrition support.

One of the most important substitution threats is from GLP-1 products. Health Canada indicates that WEGOVY is approved (status date: 2024-10-25), and the Ontario government changed Ozempic to “Limited Use” coverage as of January 31, 2024. The PMPRB indicates that sales of patented medicines reached $22.1 billion in 2024, a 10.9% increase from the previous year, further increasing the competitive pressure on traditional packaged products.

One of the most important trends in 2026 is healthy aging driving preference. According to Statistics Canada (July 1, 2025), 19.5% of the population is 65+ years, totaling 8,108,467 Canadians, an increase of 3.4% from the previous year. Older households value functional nutrition, easy-to-consume formats, and regular maintenance over intense, short-term treatment approaches.

One of the most important opportunities in 2026 is partnerships in prevention. The Public Health Agency of Canada granted $11,843,608 to the Healthy Canadians and Communities Fund to enhance food environments and physical activity access. Segmentation analysis indicates that supplement nutrition drinks has a 70% market share, and retail offline has a 90% share, indicating a preference for ready-to-drink support purchased through trusted grocery and pharmacy channels.

Canada Weight Management and Wellbeing Market Growth DriverRising Excess-Weight Burden Sustains Preventive Demand

Demand for weight management and wellness solutions remains strong, as obesity is a prevalent and growing issue. Direct data from the Canadian Health Measures Survey indicates that 68% of adults aged 18-79 are overweight or have obesity, up from 60% and obesity alone at 33%. In children and youth aged 5-17, 31% are overweight or have obesity.

Risk factors also remain high, with 49% of adults having a waist circumference above the thresholds for abdominal obesity, which is strongly linked to increased cardiometabolic risk. This keeps households engaged in seeking real-world approaches to weight management, dietary improvement, and maintaining healthier habits, driving continuous purchases of OTC weight management solutions and nutritional support products.

Canada Weight Management and Wellbeing Market ChallengeGLP-1 Prescription Therapies Intensify Competitive Pressure

Prescription GLP-1 treatments increase substitution pressure on traditional packaged weight management products. Health Canada recognizes WEGOVY as a legitimate drug product, and provincial insurers restrict access to similar products. Ontario changes Ozempic coverage to “Limited Use” as of January 31, 2024, illustrating the rapid evolution of clinical guidelines and coverage policies in real-world practice.

Spend momentum in prescription products increases this substitution threat: sales of patented drugs in Canada are $22.1 billion in 2024, up 10.9% from last year, and account for 47% of total medicine sales. As GLP-1 performance sets a new standard for rapid and extensive outcomes, brands must prove their relevance in benefit statements, safety, and patient-friendly formulations, rather than “quick fix” weight loss.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Weight Management and Wellbeing Market TrendAging Demographics Shift Priorities Toward Everyday Wellbeing

Healthy Aging is increasingly influencing the end user in the wellbeing space. Aging of the population is already a reality, nearly one in five individuals (19.5%) are 65+ as of July 1, 2025, and the number of individuals aged 65+ is 8,108,467, up 3.4% year over year. This trend is structural and continues to expand the base for products that address strength, energy, and functional needs.

As households with aged people experience more chronic conditions and mobility issues, they seek consistent patterns over short bursts of activity. This changes focus to solutions that emphasize functional nutrition, ease of use, and clinical relevance. It also draws attention to muscle maintenance and nutrient sufficiency while addressing weight management, particularly for individuals with appetite changes and constrained daily schedules across regions across the country.

Canada Weight Management and Wellbeing Market OpportunityGovernment-Funded Healthy Eating Programs Open Partnership Space

Government prevention budgets present a real partnership opportunity for brands and businesses. Under the Healthy Canadians and Communities Fund, the Public Health Agency of Canada invests $11,843,608 in ten organizations to enhance healthier food environments and improve access to healthy food for populations experiencing health inequities.

This initiative addresses upstream drivers of risk such as unhealthy diets and a lack of physical activity, making it a pre-emptive intervention that reaches end users before issues become serious. These initiatives are typically conducted in schools, community centers, and healthcare-related settings, which expands the geography of where individuals access nutrition education and behavior change support. Brands that develop co-created evidence-based assets, support food skills programs, or provide compliant products can gain trial and credibility while meeting public health objectives in 2026 and beyond.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Canada Weight Management and Wellbeing Market Segmentation Analysis

By Category

- Meal Replacement Products

- OTC Obesity Products

- Supplement Nutrition Drinks

- Slimming Teas

- Weight Loss Supplements

The segment has the leading share in terms of product type; for this in supplement nutrition drinks account for approximately 70% share in 2025. This leading share is a result of the strong pull of the end user for ready-to-drink nutrition support that is perceived as easy to incorporate into one’s lifestyle, particularly for individuals seeking convenient protein and nutrient intake.

Meal replacements are still around but are under greater pressure to be substituted by prescription-driven weight management solutions and general dietary supplements. Brands in the leading segment rely on broad national retail distribution and established medical-style positioning, which helps end users perceive these products as “safe, everyday” solutions rather than a quick fix.

By Sales Channel

- Retail Offline

- Retail Online

The segment has the greatest market share by sales channel; for this in retail offline accounts for approximately 90% market share in 2025. This is because end users tend to favor purchasing these products in conjunction with regular grocery and pharmacy trips, and offline visibility helps drive trial and repeat business.

Offline, pharmacies and large-format retailers enjoy the benefits of trust, strong point-of-sale presence, and common promotions or loyalty rewards, which are important when budgets are constrained. Retail e-commerce continues to evolve as a convenience extension, but this is largely a supplement to offline shopping rather than a replacement for most households.

List of Companies Covered in Canada Weight Management and Wellbeing Market

The companies listed below are highly influential in the Canada weight management and wellbeing market, with a significant market share and a strong impact on industry developments.

- Iovate Health Sciences International Inc

- Herbalife Nutrition Ltd

- WN Pharmaceuticals Ltd

- Abbott Laboratories Inc

- Nestle Health Science SA

- Premier Nutrition Co LLC

- Glanbia Plc

- Loblaw Cos Ltd

- Stella Pharmaceutical Canada Inc

- USANA Health Sciences Inc

Competitive Landscape

The competitive landscape in 2025 is led by Abbott Laboratories Inc with 37.1% and Nestle Health Science SA with 21.4%, reflecting strong concentration in supplement nutrition drinks. Abbott maintains leadership through its Ensure and Glucerna brands, which benefit from wide national distribution across pharmacies, hypermarkets, warehouse clubs, and retail e-commerce platforms such as Walmart Canada and Shoppers Drug Mart. Ensure’s broad variant range, including high-protein and calorie-support options, strengthens its appeal among middle-aged and elderly consumers seeking convenient liquid nutrition. Nestlé Health Science competes primarily through Boost, which is similarly well distributed and positioned around active lifestyles and healthy ageing. Both players leverage strong retail visibility, trusted medical-style positioning, and extensive flavour portfolios to drive repeat purchases. Their scale advantages, brand recognition, and pharmacy presence reinforce competitive barriers, while smaller players rely more heavily on niche positioning and protein-focused messaging to sustain share in a substitution-pressured environment.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Canada Weight Management and Wellbeing Market Policies, Regulations, and Standards

- Canada Weight Management and Wellbeing Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Canada Weight Management and Wellbeing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Category

- Meal Replacement Products- Market Insights and Forecast 2022-2032, USD Million

- Shakes- Market Insights and Forecast 2022-2032, USD Million

- Bars- Market Insights and Forecast 2022-2032, USD Million

- Ready-to-Drink (RTD) Beverages- Market Insights and Forecast 2022-2032, USD Million

- Powder Mixes- Market Insights and Forecast 2022-2032, USD Million

- OTC Obesity Products- Market Insights and Forecast 2022-2032, USD Million

- Fat Absorption Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Appetite Suppressants- Market Insights and Forecast 2022-2032, USD Million

- Metabolism Boosters- Market Insights and Forecast 2022-2032, USD Million

- Supplement Nutrition Drinks- Market Insights and Forecast 2022-2032, USD Million

- Slimming Teas- Market Insights and Forecast 2022-2032, USD Million

- Weight Loss Supplements- Market Insights and Forecast 2022-2032, USD Million

- Meal Replacement Products- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Obesity Management- Market Insights and Forecast 2022-2032, USD Million

- Diabetes-Associated Weight Control- Market Insights and Forecast 2022-2032, USD Million

- Cardiovascular Risk Reduction- Market Insights and Forecast 2022-2032, USD Million

- Post-Bariatric Surgery Weight Maintenance- Market Insights and Forecast 2022-2032, USD Million

- General Fitness & Lifestyle Weight Control- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Specialty & Bariatric Clinics- Market Insights and Forecast 2022-2032, USD Million

- Weight Loss Centers- Market Insights and Forecast 2022-2032, USD Million

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies & Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Nutrition Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Canada Meal Replacement Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada OTC Obesity Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Supplement Nutrition Drinks Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Slimming Teas Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Weight Loss Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Abbott Laboratories Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestle Health Science SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Premier Nutrition Co LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Glanbia Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Loblaw Cos Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Iovate Health Sciences International Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Herbalife Nutrition Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WN Pharmaceuticals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Stella Pharmaceutical Canada Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- USANA Health Sciences Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories Inc

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Application |

|

| By End User |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.