Brazil Passenger Car Tire Market Report: Trends, Growth and Forecast (2026-2032)

By Vehicle Type (Sedan, SUV, Hatchback), By Best Selling Car (Hyundai HB20, Volkswagen GoI, Chevrolet Onix, FIAT Strada, Volkswagen Polo, Others), By Demand Type (OEM, Aftermarket), By Sales Channel (Direct Sales, Multi Brand Stores & Exclusive Outlets, Online), By Tire Type (Radial, Bias), By Tire Size (Tire Size 1, Tire Size 2, Tire Size 3, Tire Size 4, Tire Size 5), By Price Category (Budget, Economy, Premium), By Region (North (Pará, Amazonas, Rondônia, Others), Northeast (Ceará, Pernambuco, Bahia, Maranhão, Others), Southeast (São Paulo, Minas Gerais, Others), South (Paraná, Rio Grande do Sul, Others), Center-West (Mato Grosso, Goiás, Others)) ... Read more

|

Major Players

|

Brazil Passenger Car Tire Market Statistics and Insights, 2026

- Market Size Statistics

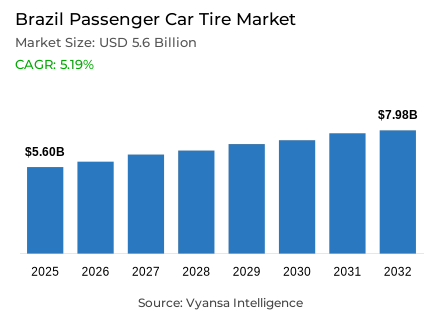

- Brazil passenger car tire market is estimated at USD 5.6 billion in 2025.

- The market size is expected to grow to USD 7.98 billion by 2032.

- Market to register a cagr of around 5.19% during 2026-32.

- Vehicle Type Shares

- SUV grabbed market share of 60% in terms of units sold.

- Competition

- Brazil passenger car tire market is currently being catered to by more than 25 companies.

- Top 5 companies acquired around 45% of the market share.

- Yokohama; Nexen; Giti; Pirelli Tyre S.p.A; Goodyear etc., are few of the top companies.

- Tire Type

- Radial grabbed 95% of the market in terms of units sold.

- Faster Growing Tire Size Segment

- 215/65 R16 segment to register 8.5% CAGR during 2026-32.

Brazil Passenger Car Tire Market Outlook

In 2025, Brazil's passenger car tire market is valued at USD 5.60 billion and is projected to reach USD 7.98 billion by 2032, growing at a 5.19% CAGR. This growth is driven by rising replacement demand for passenger car tires and increased localization of car production. Strong recovery in new vehicle sales in 2025, with over 2.4 million cars, has boosted both OEM (first-fit) and aftermarket tire demand, according to ANFAVEA.

Automakers are expanding local assembly capacities, with major players like Stellantis committing multibillion-dollar investments, which will increase the volume of vehicles entering the replacement cycle. Meanwhile, trade policies have tightened import competition through tariffs and remedies, supporting domestic manufacturers by raising the landed cost of low-cost imports. This has enabled local tire producers to invest in capacity upgrades and product enhancements.

Shifting consumer preferences toward SUVs and larger wheel sizes are also driving market value. These vehicle types typically use higher-priced, premium tires. The aftermarket remains the largest revenue generator, fueled by a growing vehicle parc and increased miles driven as urban mobility returns to pre-pandemic norms.

Although raw material costs, especially for natural and synthetic rubber, have been volatile, manufacturers have managed cost pressures through pricing strategies negotiated with OEMs and aftermarket distributors. Additionally, international automakers are prioritizing regional sourcing, enhancing long-term demand certainty for local tire suppliers.

Brazil Passenger Car Tire Market Growth Driver

Consumer and Vehicle Fleet Shift to Sport Utility Vehicles and Larger Wheel Sizes

The dominant driver of Brazil’s passenger car tire market is the structural shift toward sport utility vehicles (SUVs) and crossovers, which boosts both original equipment and replacement demand. Over the past decade, Brazil consumers have increasingly favored SUVs for their safety, versatility, and road presence. This shift raises the average tire size and selling price, as SUV tires are larger and built for higher load and speed ratings. With each SUV requiring four larger, often premium-branded tires, total market revenue increases significantly.

In 2025, Brazil's car sales are expected to exceed 2.4 million units, with monthly production averaging over 220,000 vehicles. Popular models include the Volkswagen Polo, Fiat Argo, and Toyota Corolla. In the SUV category, the Jeep Compass, Caoa Chery Tiggo 7, and Volkswagen Taos saw strong consumer demand.

Automakers are reinforcing this trend by investing heavily in local SUV and hybrid production. These investments drive original equipment tire demand, while a growing vehicle parc and rising annual kilometers traveled continue to support the replacement segment, shortening tire replacement cycles and sustaining long-term market growth.

Brazil Passenger Car Tire Market Challenge

Volatility in Raw Material Prices and Supply Chain Constraints

The fluctuating price of natural and synthetic materials is the area that is alarming for the for tire manufacturers in Brazil. It is being governed by global trends and exchange rates. While certain rubber-related products are produced domestically in Brazil, the global market impacts the industry, and this results in price volatility. To offset this, it is essential that the industry use optimized procurement practices and share the burden with consumers.

They are also further being made complicated by supply chain disruptions. For example, port congestion and a shortage of shipping containers might increase landed costs and push back production schedules. Further, unpredictable changes in tariffs and trade policies might create uncertainties for companies that carry out international sourcing.

Macroeconomic variables such as high interest rates and economic turmoils are also increasing the cost of capital for capital-intensive projects. This makes it difficult for the local manufacturers, especially those who are smaller in size, to invest in the latest technologies or R&D in tire compounds. To address these challenges, tire makers are advised to invest in procurement hedging, build local supply chains, or implement flexible manufacturing systems. Otherwise, the sector may face threats such as price erosion, decelerated innovations, or delayed premiumization.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Passenger Car Tire Market Trend

Localization and Policy Led Protection Supporting Mid-Tier and Premium Local Production

One of the most prominent trends in the Brazil passenger car tire market is localization of manufacturing, which is being encouraged by favorable trade policies. Changes in import duties and the beginning of anti-dumping duties against imports of tires have made it more expensive for imports and thereby opened up the market for Brazil tire manufacturers and given MNCs the incentive to set up their manufacturing facilities in Brazil.

This will be evident through the increase in investment by car makers in local manufacturing and through the commitment of the main global tire makers to alter or adjust manufacturing capacity to cater to the needs of the region. Localization not only minimizes delivery time with respect to original equipment (first-fit) tires, but it also minimizes vulnerability to fluctuations with respect to foreign exchange.

Many of the leading Brazil tire makers have adopted hybrid approaches, with the production of high-volume basic sizes in the country, in combination with the import of specialized tires. Another recently noticed feature in this regard relates to adapting the tread patterns and rubber compositions according to the conditions in Brazil.

Brazil Passenger Car Tire Market Opportunity

Premiumization in Replacement and First Fit for Sport Utility Vehicles

One of the main opportunities for tire makers in Brazil is the premium-ization of the replacement market, also known as the after-market, and the first-fit market, specifically for the SUV category. With the growing trend in the country to favor the usage of SUVs, the demand for bigger tires with latest technology, such as reinforced radial tires, all-season tires, and run-flat tires, is also on the increase. These tires have premium pricing, resulting in better profit margins for the makers.

In order for the trend to be leveraged, global and domestic tire manufacturing firms can invest in the production of popular tire size categories, for instance, the 215/65 R16 tire size. Moreover, collaboration with domestic service chains can add value and support tire presence in the market.

Opportunities in 2025 continued to widen with the announcement of BYD injecting USD 1 billion into the construction of its largest electric vehicle production base outside of the Asian continent in Brazil, with an expected EV output of 300,000 units per year. BYD further unveiled its new flagship EV SUV, Song Pro COP30. At about the same time, another Chinese EV leader committed USD 1.06 billion for EV production and regional exports. The EV SUV market is emerging as a strategic growth area for luxury tire makers in Brazil.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Passenger Car Tire Market Segmentation Analysis

By Vehicle Type

- Sedan

- SUV

- Hatchback

The SUV segment dominates Brazil’s passenger car tire market, accounting for 60% of revenue, driven by strong and sustained consumer preference across urban and peri-urban areas. This dominance is underpinned by automaker strategies that introduced a wide range of SUV and crossover models tailored to local tastes, including flexible fuel and hybrid variants. Between 2017 and 2021, the surge in compact and affordable SUVs reshaped consumer preferences, with buyers increasingly choosing SUVs over sedans and hatchbacks for their spacious interiors and perceived safety benefits.

OEMs such as General Motors, Volkswagen, Hyundai, and Stellantis (Jeep and Fiat) have significantly boosted first fit demand through aggressive SUV launches. According to Fenabrave and industry sources, SUV market penetration surged in 2021 and remained in the high 40% range by 2024. This coincided with a 14% rise in total vehicle sales to 2.63 million units, including a 13.2% increase in passenger car sales, signaling robust momentum in both OEM and aftermarket tire channels.

Looking ahead, Stellantis’ USD 6 billion investment (2025–2030) for over 40 new models—including hybrids—reinforces the long-term growth outlook. Combined with Brazil’s supportive “Mover” program and favorable trade policies, these factors will drive continued expansion of SUV tire demand, particularly for premium and larger-sized products in both first fit and replacement markets.

By Tire Type

- Radial

- Bias

Radial tires account for 95% of Brazil’s passenger car tire market, underscoring their global adoption and long-term performance benefits over bias-ply alternatives. Radial construction provides superior tread contact, reduced rolling resistance, and longer tread life—attributes that align with consumer expectations for fuel efficiency, safety, and lower total cost of ownership. This near-total market share has driven widespread alignment of domestic production infrastructure toward radial ply manufacturing. Most factories in Brazil are configured specifically for radial tires, and the supporting supply chain for materials and reinforcements is well established across local and regional networks.

Radial dominance also allows manufacturers to achieve economies of scale in developing optimized compounds and tread patterns tailored to Brazil’s road surfaces and climate variations. Automakers overwhelmingly favor radial tires for original equipment (OE) fitments in both passenger cars and SUVs due to regulatory compliance and consistent performance standards.

Leading manufacturers are further advancing radial technology through investments in high-modulus reinforcements and silica-rich compounds. As the market matures, competition will increasingly center on compound performance, tread wear, wet grip, and noise levels. Companies with local production and R&D capabilities will be best positioned to capture premium demand in this evolving landscape.

List of Companies Covered in Brazil Passenger Car Tire Market

The companies listed below are highly influential in the Brazil passenger car tire market, with a significant market share and a strong impact on industry developments.

- Yokohama

- Nexen

- Giti

- Pirelli Tyre S.p.A

- Goodyear

- Continental AG

- Michelin

- Bridgestone Corporation

- Kumho

Recent Developments

- Linglong, 2025:

In 2025, Shandong Linglong Tire and Sunset S.A. launched a $1.2 billion joint venture to build a tire plant in Ponta Grossa, Brazil. The facility will produce 14.7 million high-performance radial tires annually, including 12 million passenger car tires, 2.4 million truck and bus tires, 200,000 engineering tires, and 100,000 retreaded tires

- Pirelli Tyre S.p.A, 2023-2025:

Pirelli acquired Hevea-Tec, Brazil's largest independent natural rubber processor, in 2023 to strengthen its sustainable supply chain. Following this strategic move, the company launched the Pirelli P Zero tire in 2025, made with over 70% bio-based and recycled materials, including FSC-certified natural rubber, advancing its commitment to eco-friendly tire production.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Brazil Passenger Car Tire Market Policies, Regulations, and Standards

4. Brazil Passenger Car Tire Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Brazil Passenger Car Tire Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold (Thousand Units)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Vehicle Type

5.2.1.1. Sedan- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. SUV- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Hatchback- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Best Selling Car

5.2.2.1. Hyundai HB20- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Volkswagen GoI- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Chevrolet Onix- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. FIAT Strada- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Volkswagen Polo- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Demand Type

5.2.3.1. OEM- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Aftermarket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Direct Sales- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Multi Brand Stores & Exclusive Outlets- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Tire Type

5.2.5.1. Radial- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Bias- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Tire Size

5.2.6.1. Tire Size 1- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Tire Size 2- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Tire Size 3- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Tire Size 4- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Tire Size 5- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Price Category

5.2.7.1. Budget- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.7.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Region

5.2.8.1. North- Market Insights and Forecast 2022-2032, USD Million

5.2.8.1.1. Pará- Market Insights and Forecast 2022-2032, USD Million

5.2.8.1.2. Amazonas- Market Insights and Forecast 2022-2032, USD Million

5.2.8.1.3. Rondônia- Market Insights and Forecast 2022-2032, USD Million

5.2.8.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2. Northeast- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2.1. Ceará- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2.2. Pernambuco- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2.3. Bahia- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2.4. Maranhão- Market Insights and Forecast 2022-2032, USD Million

5.2.8.2.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.8.3. Southeast- Market Insights and Forecast 2022-2032, USD Million

5.2.8.3.1. São Paulo- Market Insights and Forecast 2022-2032, USD Million

5.2.8.3.2. Minas Gerais- Market Insights and Forecast 2022-2032, USD Million

5.2.8.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.8.4. South- Market Insights and Forecast 2022-2032, USD Million

5.2.8.4.1. Paraná- Market Insights and Forecast 2022-2032, USD Million

5.2.8.4.2. Rio Grande do Sul- Market Insights and Forecast 2022-2032, USD Million

5.2.8.4.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.8.5. Center-West- Market Insights and Forecast 2022-2032, USD Million

5.2.8.5.1. Mato Grosso- Market Insights and Forecast 2022-2032, USD Million

5.2.8.5.2. Goiás- Market Insights and Forecast 2022-2032, USD Million

5.2.8.5.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.9.By Competitors

5.2.9.1. Competition Characteristics

5.2.9.2. Market Share & Analysis

6. Brazil Sedan Tire Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold (Thousand Units)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Best Selling Car- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Demand Type- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Tire Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Tire Size- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Brazil SUV Tire Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold (Thousand Units)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Best Selling Car- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Demand Type- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Tire Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Tire Size- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Brazil Hatchback Tire Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Units Sold (Thousand Units)

8.2. Market Segmentation & Growth Outlook

8.2.1.By Best Selling Car- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Demand Type- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Tire Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Tire Size- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.7.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Bridgestone Corporation

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Michelin

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Continental AG

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Pirelli Tyre S.p.A

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Goodyear

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Nexen

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Yokohama

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Giti

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Kumho

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Linglong

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Vehicle Type |

|

| By Best Selling Car |

|

| By Demand Type |

|

| By Sales Channel |

|

| By Tire Type |

|

| By Tire Size |

|

| By Price Category |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.