Brazil Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients), By Region (North, Center-West, Northeast, Southeast, South) ... Read more

|

Major Players

|

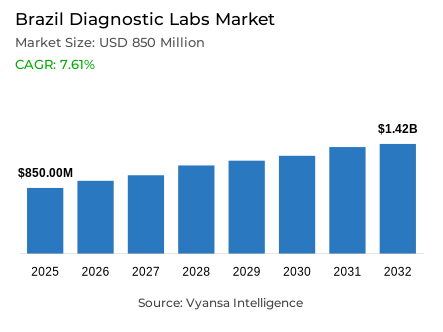

Brazil Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

- Diagnostic labs in Brazil is estimated at USD 850 million in 2025.

- The market size is expected to grow to USD 1.42 billion by 2032.

- Market to register a cagr of around 7.61% during 2026-32.

- Lab Type Shares

- Single/independent laboratories grabbed market share of 55%.

- Competition

- Diagnostic labs in Brazil is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 60% of the market share.

- Hospital Israelita Albert Einstein (Diagnostic Medicine), Alliar (Alliança Saúde), Boris Berenstein Diagnostic Center, Diagnosticos da America S.A. (DASA / Dasa Labs), Quest Diagnostics Incorporated etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Brazil Diagnostic Labs Market Outlook

Brazil's diagnostic labs market is set for steady expansion, valued at $850 million in 2025 and projected to reach $1.42 billion by 2032, growing at a CAGR of approximately 7.61% during 2026-32. This growth is fueled by rising private health insurance enrollment, which reached 53.2 million beneficiaries in December 2025, covering 25% of the population. As more Brazilians gain insurance access, laboratories experience predictable demand from chronic disease monitoring, preventive screenings, and routine diagnostic services, creating stable revenue streams across reimbursed provider networks.

The market structure remains highly fragmented, with Single/Independent Laboratories holding 55% market share. These standalone facilities compete through convenient locations, quick turnaround times, and personalized service for local clinics and corporate accounts. General & Clinical Testing dominates the service mix at 45%, reflecting the essential role of routine chemistry panels, hematology profiles, and basic microbiology in everyday healthcare. This high-volume testing forms the financial backbone that enables laboratories to invest in specialized capabilities and advanced technologies.

Brazil's chronic disease burden drives sustained testing demand, with 61.4% of adults having excess weight, 24.3% living with obesity, and significant populations managing diabetes and hypertension. These conditions generate repeat testing patterns for glucose monitoring, lipid panels, and cardiovascular risk assessments, making automation, quality controls, and digital result delivery critical for operational efficiency.

Emerging from the modernization of public health are fresh opportunities in the form of the rollout of the DNA-HPV molecular testing strategy across 12 states in 2025, which provides laboratories an opportunity to maximize the utilization of resources in the development and delivery of women's healthcare. Included in these trends towards an expanded and better-run market is the government investment in the R$2.4 billion PMAE program to develop further consultation and exams.

Brazil Diagnostic Labs Market Growth Driver

Expanding Private Health Insurance Penetration Fuels Consistent Testing Demand

The private health insurance base in Brazil keeps on growing steadily, directly supportive of continued demand for laboratory testing services through reimbursed provider networks. According to the ANS, there were 53,180,646 beneficiaries enrolled in medical-hospital plans as of December 2025, compared with 52,014,285 in December 2024 and 51,290,303 in December 2023-a coverage rate for medical plans of 25.0%. This has been an upward trajectory with a gradual but relentless migration toward insured pathways to healthcare, where the end user increasingly relies on cover for even routine diagnostic services.

As private insurance penetration deepens, Laboratories are witnessing increased regular order flows from chronic disease monitoring, pre-procedural workups, and preventive health screenings. The evolution compels providers to elevate their operational standards of reporting accuracy, billing compliance, and turnaround times to maintain their positions on the payer panels. Quality systems and operational efficiency take the center stage in competitive differentiators as labs align service delivery with operator rules, authorization protocols, and reimbursement frameworks to ensure continuity and satisfaction of revenue streams and end users in an increasingly formalized market environment.

Brazil Diagnostic Labs Market Challenge

Public System Capacity Constraints and Service Delivery Timelines Present Operational Hurdles

The pressure for access in the public healthcare system in Brazil keeps diagnostic infrastructure tight, especially regarding specialized examinations that involve tertiary care pathways. The "Mais Acesso a Especialistas-PMAE" program of the Ministry of Health has the objective of expanding the supply of specialized consultations and exams available in the SUS by 30%, and this will be accompanied by R$ 2.4 billion in funding through the end of 2025. Such large investment underlines the dimension of the currently accumulated waiting lists and the imperative for better scheduling and referral routing mechanisms across the diagnostic network.

For laboratory operators, these systemic challenges translate into an execution-focused set of operational demands, rather than straightforward demand growth. Providers need to manage high referral peaks, meet stringent service-time requirements-delivery of consultations and exams within 30 or 60 days based on case complexity-and make sure documentation aligns with public contracting models and regulatory standards. This environment creates considerable administrative overhead, with process discipline critical across sample logistics, appointment capacity management, and result delivery workflows. Labs that cannot adhere to these operational standards face exclusion from public contracts and thus are constrained in their capacity to serve a considerable part of the end user population.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Diagnostic Labs Market Trend

Growing Chronic Disease Prevalence Drives Recurring Clinical Pathology Volumes

Ongoing demand for routine clinical pathology testing can be assured as Brazil's population dynamics continue along their current lines. As can be seen from the Ministry of Health's Vigitel survey 2023, about 61.4% of the population in the 27 state capitals and Federal District register excess weight, and another 24.3% register obesity. In addition to these statistics, diabetics comprise 10.2%, and hypertensives comprise 27.9% of the population. These figures reflect a population-wide shift toward metabolic and cardiovascular risk conditions.

The chronic disease state creates a repeat testing’ pattern by which individual end users repeatedly access facility services for routine monitoring of blood glucose, lipid determinations, renal and liver chemistries, as well as cardiovascular risk factor evaluations. It is no surprise, then, that laboratories emphasize "automated high throughput platforms" as well as quality pre-analytical design elements and "swift digital reporting solutions" as a means of efficiently managing these repeat test strategies. This, in essence, creates a state by which routine clinical pathology serves as the basic platform from which laboratory business strategies can begin. Small operational inefficiencies compound quickly at chronic-care scale, making standardization and technological investment critical.

Brazil Diagnostic Labs Market Opportunity

Molecular HPV Screening Implementation Creates Scalable Women's Health Service Expansion

Brazil's modernization of public health screening points to significant growth opportunities, especially in the shift toward using molecular diagnostic methods in its preventive care programs. In August 2025, the Ministry of Health launched the implementation of the DNA-HPV molecular test in SUS, with support from PAHO/WHO, where the Health Minister confirmed that this had already been deployed in 12 Brazilian states. This test will detect 14 HPV genotypes and can thus identify infection much sooner before lesions or invasive cancer have developed, marking a fundamental shift in the paradigm of cytology-based screening approaches. Scaling DNA-HPV testing provides diagnostic laboratories with a real-world avenue to realize value from the molecular testing infrastructure put in place during the pandemic and helps extend service lines in women's health beyond cytology.

Success lies in implementing robust sample collection and transport routines, validated PCR workflows, and transparent reporting formats that interface with organized screening programs. When implemented successfully, such public screening programs translate into regular, high-volume workflows for the laboratory with strong clinical value, allowing revenue diversification and capacity utilization on molecular platforms. The opportunity goes beyond immediate testing volumes to positioning providers as strategic partners in population health.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

The Brazil diagnostic labs market exhibits a highly fragmented provider landscape, with Single/Independent Laboratories commanding approximately 55% market share in the Lab Type segmentation. This dominance reflects a service delivery structure characterized by numerous standalone facilities and small networks operating across local markets, competing primarily on convenience, proximity to referring physicians, and rapid turnaround capabilities. The fragmented nature of the market underscores the persistence of regional and neighborhood-based diagnostic service models.

Independent laboratories maintain market relevance through flexible specimen collection options, localized presence in residential and commercial areas, and customized service packages tailored to private clinics and corporate health accounts. However, their smaller scale often limits automation depth, quality accreditation investments, and integrated IT systems compared to large chains. Consequently, many independent providers increasingly establish partnerships for reference testing, specialized assays, and digital reporting capabilities. The 55% market share held by independent labs signals that successful market strategies must function effectively across thousands of individual touchpoints rather than relying solely on centralized national networks or large chain operations.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General & Clinical Testing represents approximately 45% of the Testing Services mix in the Brazil diagnostic labs market, establishing routine diagnostic panels as the fundamental service offering across the sector. This leadership position reflects the central role that chemistry panels, hematology profiles, and basic microbiology testing play in initial diagnosis, chronic disease monitoring, and pre-procedural medical clearance across both outpatient clinics and hospital settings. These routine services form the backbone of laboratory operations.

The high frequency and fast turnaround requirements of general and clinical tests drive laboratories to prioritize automation investments, standardized pre-analytical procedures, and consistent reference ranges to minimize repeat testing and operational inefficiencies. Beyond this core 45% segment, the remaining service portfolio encompasses higher-complexity diagnostic modalities—including molecular diagnostics, anatomic pathology, and imaging-linked workflows—where test volumes are lower but clinical decision-making impact is substantially higher. This segmentation distribution demonstrates that achieving scale and efficiency in everyday testing provides the financial foundation that enables laboratories to invest in specialized capabilities and advanced diagnostic technologies.

List of Companies Covered in Brazil Diagnostic Labs Market

The companies listed below are highly influential in the Brazil diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Hospital Israelita Albert Einstein (Diagnostic Medicine)

- Alliar (Alliança Saúde)

- Boris Berenstein Diagnostic Center

- Diagnosticos da America S.A. (DASA / Dasa Labs)

- Quest Diagnostics Incorporated

- SYNLAB (SYNLAB-Solutions in Diagnostics)

- Grupo Fleury

- Grupo Sabin

- Clínica da Imagem do Tocantins

- Abramed (BP Medicina Diagnóstica)

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Brazil Diagnostic Labs Market Policies, Regulations, and Standards

4. Brazil Diagnostic Labs Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Brazil Diagnostic Labs Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Lab Type

5.2.1.1. Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Testing Services

5.2.2.1. Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Disease

5.2.3.1. Cardiology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Oncology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Neurology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Orthopedics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Gynecology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. Odontology- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Revenue Source

5.2.4.1. Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Public System- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Test Type

5.2.5.1. Pathology- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Radiology- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Referrals- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Walk-ins- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Region

5.2.7.1. North

5.2.7.2. Center-West

5.2.7.3. Northeast

5.2.7.4. Southeast

5.2.7.5. South

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Brazil Single/Independent Laboratories Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

7. Brazil Hospital-based Laboratories Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

8. Brazil Physician Office Laboratories Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Testing Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Disease- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Test Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Diagnosticos da America S.A. (DASA / Dasa Labs)

9.1.1.1. Business Description

9.1.1.2. Service Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Quest Diagnostics Incorporated

9.1.2.1. Business Description

9.1.2.2. Service Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.SYNLAB (SYNLAB-Solutions in Diagnostics)

9.1.3.1. Business Description

9.1.3.2. Service Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Grupo Fleury

9.1.4.1. Business Description

9.1.4.2. Service Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Grupo Sabin

9.1.5.1. Business Description

9.1.5.2. Service Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Hospital Israelita Albert Einstein (Diagnostic Medicine)

9.1.6.1. Business Description

9.1.6.2. Service Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Alliar (Alliança Saúde)

9.1.7.1. Business Description

9.1.7.2. Service Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Boris Berenstein Diagnostic Center

9.1.8.1. Business Description

9.1.8.2. Service Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Clínica da Imagem do Tocantins

9.1.9.1. Business Description

9.1.9.2. Service Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Abramed (BP Medicina Diagnóstica)

9.1.10.1. Business Description

9.1.10.2. Service Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.