Belgium Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Belgium Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

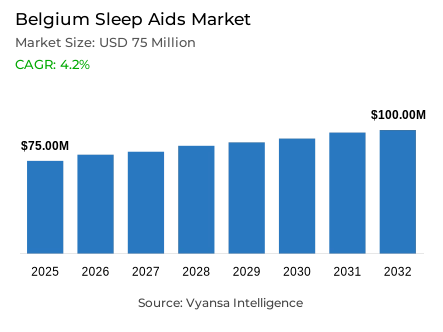

- Sleep aids market size in Belgium was estimated at USD 75 million in 2025.

- The market size is expected to grow to USD 100 million by 2032.

- Market to register a CAGR of around 4.2% during 2026-32.

- Product Shares

- Single ingredient grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing sleep aids in Belgium .

- Top 5 companies acquired around 70% of the market share.

- Arkopharma Belux SA, Forté Pharma SA Laboratoires, Procter & Gamble Health Belgium NV, Melisana SA, Tilman SA etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 70% of the market.

Belgium Sleep Aids Market Outlook

The Belgium sleep aids market will experience a phase of healthy growth, as health awareness increases and the number of stress-related disorders such as burnout grows dramatically. The market is estimated to be USD 75 million in 2025 and USD 100 million in 2032 with a compound annual growth rate of about 4.2 percent between 2026 and 2032. Uncertainty in the economy, inflation and social restlessness have placed quality sleep on the agenda of many Belgians who want to remain mentally healthy.

The market is moving resolutely towards natural and non-addictive solutions. The end users are abandoning the use of traditional benzodiazepines because of the safety concerns raised by health authorities and instead they are using plant-based products that contain valerian root, passionflower, and saffron. Supplements based on melatonin are also becoming very popular in terms of their ability to control sleep-wake cycles. This has promoted innovation, with brands such as Tilman introducing stronger natural formulas to satisfy the need to have effective but safe alternatives.

There is a wide competitive environment with the established players such as Melisana SA and Tilman SA experiencing growing competition with the emerging brands such as Metagenics and Forte Pharma. The market is also diversifying into other forms like gummies, syrups and sprays which are becoming popular as opposed to the traditional tablets. These products are also becoming more accessible to price-sensitive shoppers due to the emergence of retailer-created private labels such as Kruidvat, which is further driving market volume.

In the future, distribution is becoming multi-channel. Although the traditional pharmacies are still the main source of reliable guidance, the non-pharmaceutical sources such as supermarkets and online retailing platforms are growing at a very high rate. The convenience and diversity of platforms such as Amazon are making them a major destination of melatonin-based products. With the sleep health being holistically incorporated into the Belgian wellness routine, the market is projected to continue its positive trend until 2032.

Belgium Sleep Aids Market Growth Driver

Burnout and Depression Surge Reinforcing Preventive Sleep Support Spending

Sleep support is actively pursued by Belgian end users since the problem of daily stress and burnout is still evident. According to official disability statistics published by the National Institute of Health and Disability Insurance in Belgium, 137,454 individuals are in long-term work incapity because of depression or burnout by end-2023, and the number of cases increased 44 percent between 2018 and 2023, indicating a long-term mental burden that frequently disrupts sleep. This stress is reflected in the consistent demand of available sleep aids, particularly those that are marketed as safe and non-addictive.

Sleep disturbances remain on the agenda in 2025 due to increasing anxiety, inflation concerns, and job insecurity. The same National Institute of Health and Disability Insurance data indicate that expenditure on long-term incapability associated with depression or burnout is over EUR 2 billion in 2023, which reinforces the emphasis on prevention and recovery behaviours, such as improved sleep habits. This high economic cost supports the business case of sleep support products as a necessity wellness product and not a luxury item, which grounds long-term baseline demand of available, over-the-counter sleep support products during the forecast period. :

Belgium Sleep Aids Market Challenge

Tight Regulatory Oversight and Reclassification Risks Elevating Compliance Complexity

The environment of compliance is complex because the Belgian authorities threaten to stop long-term reliance on prescription sleep medicines, which compels end users to resort to non-pharmaceutical alternatives. On 21 March 2025, the Federal Agency for Medicines and Health Products of Belgium officially made the benzodiazepine withdrawal programme permanent, highlighting the official questioning of sleep-related treatments and the importance of cautious claims and usage advice in all product categories.

Simultaneously, regulations on ingredients like melatonin and herbal extracts restrict the extent to which companies can push in the creation and marketing of more potent formulas, despite the end user requiring greater efficacy. As National Institute for Health and Disability Insurance records a 9.37 percent annual increase in long-term incapity due to depression or burnout in 2023, the demand is high but competition is growing as dietary supplements and mood enhancers flood the same need state, making differentiation more difficult without leaving regulatory guardrails or causing reclassification.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Belgium Sleep Aids Market Trend

Natural-First Formulations and User-Friendly Formats Broadening Category Appeal

The preference of end users is moving to natural, non-invasive sleep support, which elevates plant-based extracts of valerian and lemon balm and boosts the appeal of melatonin supplements marketed as wellness products. This health-driven change is reflected in product development with more robust natural versions and clean-label positioning, but without compromising on safety and transparency that appeals to the wary Belgian end users.

Meanwhile, the delivery formats are becoming more diverse as the shoppers are looking to find simpler routines than the conventional pills. Tablets are still leading, but gummies, syrups, and sprays become more noticeable as they are convenient and soft to use regularly. National Institute for Health and Disability Insurance reports the highest annual increase in long-term incapity due to depression or burnout is among individuals under 30, increasing by 21.6 percent in 2023, which supports the need to offer simple, accessible sleep solutions that can fit busy, stressed lifestyles and meet the preferences of younger end users to modern, user-friendly formats.

Belgium Sleep Aids Market Opportunity

Multi-Channel Retail Expansion Unlocking Affordable Evidence-Led Positioning

Retail is launching new routes to create scale outside of pharmacies as health and personal care chains, supermarkets, and online retail platforms expand access to sleep solutions. This opens space to brands and own label that combines trusted efficacy with keen pricing, particularly where products are readily accessible, comparative and re-orderable via retail online listing and reviews that facilitate informed buying choices.

The size of the underlying need state magnifies the opportunity. According to National Institute for Health and Disability Insurance, 37.57 percent of individuals in long-term work incapity are absent on 31 December 2023 because of mental disorders, and 69.48 percent of that group has depression or burnout. This context underpins the need to have safe, non-addictive sleep support that is an adjunct to overall mental wellbeing strategies, which will provide long-term commercial opportunities to brands that manage to negotiate regulatory demands and provide accessible, affordable solutions across the growing retail channels over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Belgium Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Doxylamine Succinate

- Diphenhydramine

- Melatonin

- Combination Ingredient

- Diphenhydramine + Acetaminophen

- Other Antihistamine-Based Combinations

- Herbal & Traditional Sleep Aids

- Valerian root

- Passionflower

- Chamomile

- Kava

- Multi-Herbal Sleep Blends

The Product Type category is dominated by Single Ingredient products, which have a market share of 45 percent. This supremacy is greatly backed by the increasing demand of melatonin-based dietary supplements and high-potency herbal extracts. These products are becoming more popular among the Belgian end users as they are seen as natural, safe, and effective in certain applications, like in controlling sleep cycles or offering a non-invasive alternative to pharmaceutical drugs.

This single-ingredient preference is part of a larger trend of transparency and clean-label formulas. Although multi-ingredient relaxation blends are on the rise, many users are drawn to the specific efficacy of products that contain a single active ingredient such as valerian root or melatonin. This segment is likely to be the market leader as the market shifts to 2032, especially with the increasing availability of generic and own-label versions of these popular single-ingredient products in retail outlets and online channels.

By Sales Channel

- Retail Online

- Retail Offline

Retail Offline channels are the most dominant in the classification of sales channels with 70 percent of the market. The robust network of conventional pharmacies and health-oriented shops such as Medi-Market maintains this leadership. Belgians still use physical stores to get professional advice that they trust, particularly when they need safe alternatives to prescription drugs. Supermarkets such as Colruyt are also contributing more by making plant-based sleep more accessible to ordinary customers.

Despite the fact that retail offlineis the main channel, it is under pressure due to the rapid development of online retail platforms. Online platforms are now very popular due to their competitive prices and the possibility to buy a greater range of formulations in a discreet manner. Nevertheless, the established trust and the growing number of personal care chains such as Kruidvat guarantee that the retail offlinesegment will still occupy the largest portion of the market share by 2032.

List of Companies Covered in Belgium Sleep Aids Market

The companies listed below are highly influential in the Belgium sleep aids market, with a significant market share and a strong impact on industry developments.

- Arkopharma Belux SA

- Forté Pharma SA Laboratoires

- Procter & Gamble Health Belgium NV

- Melisana SA

- Tilman SA

- Therabel Pharma SA

- EG NV/SA

- Metagenics Belgium NV SA

- Bio-Life Laboratory Sprl

- Pharma Nord sprl

Competitive Landscape

Belgium’s sleep aids market is led by Melisana (Sediplus), supported by strong pharmacy distribution and brand trust, though share erosion reflects intensifying competition from Tilman (Sedistress, Sedistress Forte) and fast-growing Metagenics (Metasleep), which capitalise on demand for plant-based valerian and lemon balm formulations. Forté Pharma (FortéNight) and Arkopharma add momentum through alternative formats such as gummies and sprays, while private labels from Kruidvat and emerging generics from EG and Nutrimed heighten price competition. Supermarkets (Colruyt) and health chains (Medi-Market) are expanding access, and e-commerce accelerates melatonin uptake. Key differentiation opportunities lie in clinically substantiated natural formulas, child-specific variants, CBD-based solutions within EU limits, and digitally integrated sleep support, as regulatory constraints limit disruptive pharmaceutical innovation.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Belgium Sleep Aids Market Policies, Regulations, and Standards

4. Belgium Sleep Aids Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Belgium Sleep Aids Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Melatonin- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Valerian root- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Passionflower- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Chamomile- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.4. Kava- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.5. Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sleep Disorder

5.2.2.1. Insomnia- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Age Group

5.2.3.1. Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Hospitals- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Formulation

5.2.6.1. Tablets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Gummies- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Capsules- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Liquid- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Sublingual- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Belgium Single Ingredient Sleep Aids Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Formulation- Market Insights and Forecast 2022-2032, USD Million

7. Belgium Combination Ingredient Sleep Aids Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Formulation- Market Insights and Forecast 2022-2032, USD Million

8. Belgium Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Formulation- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Melisana SA

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Tilman SA

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Therabel Pharma SA

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.EG NV/SA

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Metagenics Belgium NV SA

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Arkopharma Belux SA

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Forté Pharma SA Laboratoires

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Procter & Gamble Health Belgium NV

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Bio-Life Laboratory Sprl

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Pharma Nord sprl

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.