Global Automotive Digital Cockpit Market Report: Trends, Growth and Forecast (2026-2032)

By Display Technology (LCD, TFT-LCD, OLED), By Application (Semi-Autonomous Vehicles, Autonomous Vehicles, Advanced Driver Assistance Systems), By Equipment (Digital Instrument Cluster, Head-Up Display (HUD), Camera Based Driver Monitoring), By Vehicle Type (Passenger Vehicle, Commercial Vehicle), By Electric Vehicle Type (Plug-in Hybrid Electric Vehicle (PHEV), Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV)), By Region (North America, South America, Europe, Asia Pacific) ... Read more

|

Major Players

|

Global Automotive Digital Cockpit Market Statistics and Insights, 2026

- Market Size Statistics

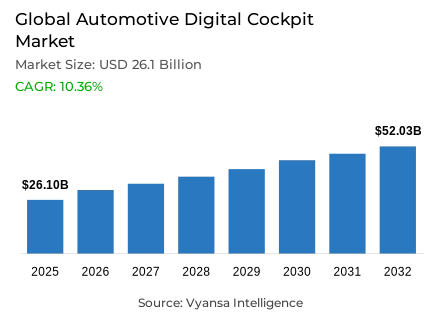

- Automotive Digital Cockpit market size was valued at USD 26.1 billion in 2025 and is estimated at USD 28.04 billion in 2026.

- The market size is expected to grow to USD 52.03 billion by 2032.

- Market to register a CAGR of around 10.36% during 2026-32.

- Display Technology Shares

- Tft-lcd grabbed market share of 40%.

- Competition

- Global automotive digital cockpit market is currently being catered to by more than 20 companies.

- Top 5 companies acquired around 35% of the market share.

- Panasonic Automotive Systems Co. Ltd., Aptiv Plc(Aptiv Global Operations Limited), LG Electronics Inc., Continental AG, Robert Bosch GmbH etc., are few of the top companies.

- Application

- Advanced driver assistance systems grabbed 45% of the market.

- Region

- Asia Pacific leads with a 40% share of the global market.

Global Automotive Digital Cockpit Market Outlook

The automotive digital cockpit market covers digital clusters, infotainment, head-up displays, cockpit domain controllers, in-cabin sensing, connected software, and automotive HMI used by manufacturers. The market is valued at USD 26.1 Billion in 2025, reaches USD 28.04 Billion in 2026, and is projected to reach USD 52.03 Billion by 2032, growing at a CAGR of 10.36% from 2026 to 2032. The global automotive digital cockpit industry consolidates navigation, diagnostics, entertainment, driver assistance, and connectivity.

Electrification, software-defined vehicle programs, ADAS penetration, and cloud-connected infotainment are raising the cockpit’s role in architecture. According to the International Energy Agency, electric car sales exceeded 17 million in 2024 and represented more than 20% of new car sales, strengthening demand for EV visualization, safety alerts, and OTA-enabled functions. The global automotive digital cockpit market benefits from platforms requiring software updates and cross-domain data presentation. The global automotive digital cockpit industry is shaped by cybersecurity, display durability, and compute scalability.

Economic impact is visible in platform sourcing, semiconductor demand, display panel procurement, and Tier-1 integration programs. The global automotive digital cockpit industry improves OEM efficiency by shifting multiple cabin functions toward centralized electronics. For suppliers, this supports higher-value content per vehicle across smart cockpit platform design, automotive display system integration, audio processing, connectivity, and safety-critical visualization. The global automotive digital cockpit market strengthens competitive positioning because cockpit usability influences fleet procurement, premium vehicle differentiation, and software monetization.

The 2026 trajectory points toward AI-powered digital cockpit interfaces, multi-screen layouts and cockpit high-performance computing. The global automotive digital cockpit market forecast remains linked to automaker investment in software-defined platforms, electric vehicle digital cockpit programs, and ADAS-integrated cockpit visualization. Global automotive digital cockpit industry suppliers combining display hardware, cockpit processors, cybersecurity compliance, and cloud update capability are better positioned as OEMs standardize cockpit architectures across brands and regions.

Global Automotive Digital Cockpit Market Growth Driver

Software-Defined Vehicle Architectures Are Expanding Cockpit Integration

Software-defined vehicle programs are moving cockpit procurement from isolated hardware selection toward integrated compute, display, connectivity, and software stacks. This shift supports global automotive digital cockpit market growth because automakers need interfaces that can combine navigation, infotainment, diagnostics, driver monitoring, and ADAS alerts without redesigning every vehicle line. Centralized cockpit architecture also improves feature reuse, update management, and supplier standardization across premium, electric, and connected models, while reducing integration duplication and validation exposure across vehicle lines.

Qualcomm stated in January 2026 that its Snapdragon Digital Chassis momentum included new collaborations, including Google, to support next-generation software-defined vehicles and agentic AI-driven personalization. This strengthens global automotive digital cockpit industry demand by expanding the role of cockpit processors, AI assistants, OTA-enabled cockpit functions, and cloud-connected development environments. As OEMs prioritize scalable platforms, Tier-1 suppliers with integrated cockpit domain controller capability gain stronger procurement visibility, faster program penetration, and deeper software lifecycle participation.

Global Automotive Digital Cockpit Market Challenge

Cybersecurity and Software Validation Are Intensifying Platform Complexity

Cybersecurity validation, software update governance, and functional-safety assurance are increasing cockpit development complexity as displays, voice assistants, ADAS visualization, and connectivity converge on centralized computing. global automotive digital cockpit industry suppliers must protect multiple operating systems, data flows, and user interfaces while meeting OEM launch timing. This raises engineering cost, extends test cycles, and can slow adoption among manufacturers that lack mature software compliance processes across global vehicle programs.

The European Union’s 2025 publication of UN Regulation No. 155 states that manufacturers need a valid certificate of compliance for the Cyber Security Management System covering the vehicle type. This creates a tougher approval environment for the automotive digital cockpit market because connected cockpit functions interact with cloud services, diagnostics, user data, and OTA updates. Suppliers unable to evidence cyber resilience, secure software maintenance, and traceable risk management face weaker platform eligibility and lower market participation in regulated vehicle platforms.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Automotive Digital Cockpit Market Trend

AI-Enabled, Multi-Display Cockpits Are Reshaping Vehicle HMI

AI-enabled cockpit computing is reshaping digital cockpit trends by moving user interaction beyond static cockpit displays toward predictive, voice-based, context-aware, and multimodal interfaces. The automotive digital cockpit market trends are increasingly defined by cockpit high-performance computers that can run instrument clusters, infotainment, passenger screens, driver monitoring, and personalized assistance within one software-defined environment. This favors suppliers with automotive SoC integration, safety isolation, scalable UX frameworks, and connected software roadmaps across regional vehicle portfolios.

Visteon announced in January 2026 a production-ready high-performance compute solution on Snapdragon Cockpit Elite, citing 3X CPU performance and 12X NPU AI performance advances versus previous cockpit platforms. This development strengthens AI-powered digital cockpit adoption because higher compute density supports richer graphics, in-cabin intelligence, and faster response across multiple displays. It also shifts competitive positioning toward suppliers that can combine hardware acceleration, generative AI assistants, safety-compliant domain integration, and lifecycle update readiness for OEM vehicle programs.

Global Automotive Digital Cockpit Market Opportunity

Electric Mobility Platforms Create Higher-Value Cockpit Integration Space

Electric vehicle programs in high-growth production hubs create an underpenetrated integration space for cockpit suppliers that can deliver display-rich, software-updateable, and AI-ready platforms at scale. The global automotive digital cockpit industry can capture higher content per vehicle when EV architectures combine range visualization, charging information, navigation, entertainment, driver assistance, and connected services inside unified interfaces. Localization of cockpit electronics also improves pricing power, sourcing flexibility and continuity.

Qualcomm reported in January 2025 that Mahindra’s new electric-origin SUVs use Snapdragon Cockpit Platform technology designed to power three 31.24 cm infotainment screens, augmented reality displays, and AI-driven in-car experiences. This supports global automotive digital cockpit market expansion by showing how EV launches require advanced cockpit processors, large displays, and next-generation vehicle cockpit functionality. Suppliers aligned with electric vehicle digital cockpit programs can improve demand capture through platform reuse, regional OEM partnerships, and faster localization decisions across export platforms.

Global Automotive Digital Cockpit Market Regional Analysis

By Region

- North America

- South America

- Europe

- Asia Pacific

Asia Pacific holds a 40% share because vehicle production scale, EV model launches, electronics manufacturing depth, and connected mobility investment are concentrated across China, Japan, South Korea, and India. Regional cockpit adoption is supported by dense OEM supply chains, strong display panel ecosystems, semiconductor packaging capability, and fast localization of infotainment, ADAS visualization, and smart cabin features. These conditions strengthen supplier access to high-volume programs across regional production lines.

China’s State Council Information Office reported in January 2026 that China’s new energy vehicle production and sales reached 16.626 million and 16.49 million units in 2025, with year-on-year increases of 29% and 28.2%. This production base supports Asia Pacific cockpit demand because NEV platforms typically require larger display areas, EV energy dashboards, connected infotainment, advanced driver assistance visualization, and OTA software capability. Regional suppliers benefit from shorter development cycles, localized sourcing, and stronger integration with automaker platform roadmaps and export programs.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Automotive Digital Cockpit Market Segmentation Analysis

By Display Technology

- LCD

- TFT-LCD

- OLED

TFT-LCD retains a 40% share under Display Technology because it offers a proven balance of cost efficiency, automotive-grade durability, brightness, temperature tolerance, and large-scale supply availability. In the global automotive digital cockpit market size structure, this position reflects OEM preference for scalable display systems across instrument clusters, center information displays, rear-seat infotainment, and head-up display support. TFT-LCD also supports multi-vehicle platform planning where predictable yields and established supplier ecosystems matter for procurement teams and cockpit planners.

LG Display stated in August 2025 that its 57-inch pillar-to-pillar LCD for cockpits was the largest automotive display then available, providing information and entertainment across the vehicle interior. This reinforces TFT-LCD’s procurement relevance by showing that LCD technology continues moving into wider, premium cockpit formats rather than remaining limited to basic digital clusters. For suppliers, large LCD capability supports design flexibility, cost-managed upgrades, and stronger adoption across connected and electric vehicle platform programs globally.

By Application

- Semi-Autonomous Vehicles

- Autonomous Vehicles

- Advanced Driver Assistance Systems

Advanced driver assistance systems hold a 45% share under Application because digital cockpits increasingly serve as the driver-facing layer for safety alerts, lane guidance, speed assistance, camera feeds, driver monitoring, and hazard visualization. In the global automotive digital cockpit market, ADAS-led demand is strengthened by OEM efforts to reduce information fragmentation and present safety-critical prompts through intuitive, low-distraction cockpit interfaces during complex driving conditions and urban traffic.

The European Commission stated that new General Safety Regulation requirements apply to all new motor vehicles sold in the EU from 7 July 2024, introducing advanced driver assistance systems including intelligent speed assistance, reversing detection, drowsiness attention warning, and advanced driver distraction warning. This supports ADAS application demand because safety functions require reliable display logic, visual prioritization, audible alerts, and driver interaction paths. Cockpit suppliers with safety-focused HMI, camera-view integration, compliance-ready visualization, and software validation capacity can strengthen competitive positioning in OEM programs.

Market Players in Global Automotive Digital Cockpit Market

These market players maintain a significant presence in the Global automotive digital cockpit market and contribute to its ongoing evolution.

- Panasonic Automotive Systems Co. Ltd.

- Aptiv Plc(Aptiv Global Operations Limited)

- LG Electronics Inc.

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Visteon Corporation

- HARMAN International

- Hyundai Mobis Co. Ltd.

- FORVIA SE

- Marelli Holdings Co. Ltd.

- Pioneer Corporation

- Alps Alpine Co. Ltd.

- Valeo SA

- Qualcomm Technologies Inc.

Market News & Updates

- HARMAN International, 2026:

HARMAN launched production-ready intelligent display solutions in January 2026 for automotive cockpit applications. The new displays are designed to improve visual clarity, power efficiency, and safety across cockpit environments. The update expands HARMAN’s in-cabin display portfolio for digital cockpit platforms requiring adaptive visual performance and driver-facing information delivery.

- Hyundai Mobis Co. Ltd., 2026:

Hyundai Mobis announced that it would unveil 29 advanced technologies at CES 2026. The technology showcase included next-generation mobility systems linked to smart vehicle interiors, connected displays, and software-defined vehicle functions. The update supports Hyundai Mobis’ positioning in digital cockpit, in-cabin electronics, and advanced vehicle interface technologies.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Automotive Digital Cockpit Market Policies, Regulations, and Standards

- Global Automotive Digital Cockpit Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology

- LCD- Market Insights and Forecast 2022-2032, USD Million

- TFT-LCD- Market Insights and Forecast 2022-2032, USD Million

- OLED- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Semi-Autonomous Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Autonomous Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Advanced Driver Assistance Systems- Market Insights and Forecast 2022-2032, USD Million

- By Equipment

- Digital Instrument Cluster- Market Insights and Forecast 2022-2032, USD Million

- Head-Up Display (HUD)- Market Insights and Forecast 2022-2032, USD Million

- Camera Based Driver Monitoring- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Vehicle- Market Insights and Forecast 2022-2032, USD Million

- Commercial Vehicle- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type

- Plug-in Hybrid Electric Vehicle (PHEV)- Market Insights and Forecast 2022-2032, USD Million

- Battery Electric Vehicle (BEV)- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Electric Vehicle (HEV)- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Display Technology

- Market Size & Growth Outlook

- North America Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Spain

- Italy

- Poland

- Rest of Europe

- Germany Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- The UAE

- Egypt

- Nigeria

- South Africa

- Rest of Middle East & Africa

- Saudi Arabia Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UAE Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Automotive Digital Cockpit Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Display Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Electric Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Continental AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DENSO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Visteon Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HARMAN International

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Automotive Systems Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aptiv Plc(Aptiv Global Operations Limited)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hyundai Mobis Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FORVIA SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Marelli Holdings Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pioneer Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alps Alpine Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valeo SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qualcomm Technologies Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Continental AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Display Technology |

|

| By Application |

|

| By Equipment |

|

| By Vehicle Type |

|

| By Electric Vehicle Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.