Australia Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

Australia Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

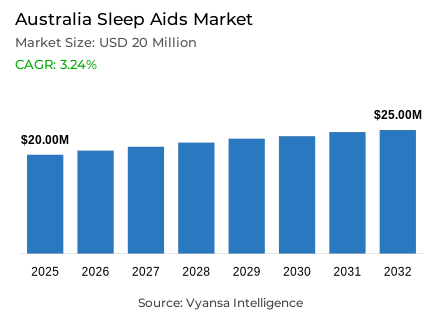

- Sleep aids market size in Australia was estimated at USD 20 million in 2025.

- The market size is expected to grow to USD 25 million by 2032.

- Market to register a CAGR of around 3.24% during 2026-32.

- Product Shares

- Single ingredient grabbed market share of 52%.

- Competition

- More than 5 companies are actively engaged in producing sleep aids in Australia .

- Top 5 companies acquired around 55% of the market share.

- Paladin Labs Inc, Aspen Pharmacare Australia Pty Ltd, Havenhall Pty Ltd, Key Pharmaceuticals Pty Ltd, Brauer Natural Medicine Pty Ltd etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 70% of the market.

Australia Sleep Aids Market Outlook

The Australia sleep-aid market is on the brink of stable growth due to the emergence of stress, anxiety, and interrupted routines as major health issues among the population. The market is expected to grow to USD 20 million in 2025 and USD 25 million in 2032 with a compound annual growth rate of about 3.24% within the 2026–2032 forecast period. Despite the fact that growth rates have slowed down since 2023, demand is still strong, especially among young adults between 18 and 30 years old and those who are economically strained due to inflation and unstable jobs.

The key trends influencing the future is the movement towards lifestyle and multifunctional products. Australias are shifting towards calming dietary supplements and herbal teas that provide sleep support in addition to stress relief and immunity benefits instead of traditional pharmacist-only medications under Schedule 3, including doxylamine. This change is also justified by the fact that some melatonin products have been down-scheduled to Schedule 3 to be used in certain applications, including jet lag relief in adults and insomnia in people over 55, which makes these solutions more available to consumers.

In the future, innovation will play a central role, with emphasis on new ingredients like magnesium, kava, and specific melatonin preparations. Moreover, female health is becoming a key growth sector, and the effects of perimenopause and menopause on sleep quality are becoming more popular. Manufacturers have significant potential to create specialised aids that can deal with these hormonal changes, which may result in long-term positive awareness and market growth.

In general, the market is becoming a dynamic ecosystem where sleep health is becoming more integrated into overall mental and physical health. With increasing awareness of the long-term dangers of sleep deprivation, the industry is poised to enjoy science-based solutions within available wellness offerings by 2032.

Australia Sleep Aids Market Growth Driver

Escalating Mental Health Burden Sustaining Structural Sleep Aid Demand

The growing pressure of stress in Australia keeps fueling the need of sleep-support products. Over 3.4 million Medicare-subsidised mental-health-specific services were processed, over 12.5 million mental-health-related prescriptions were dispensed, and Lifeline received almost 257,000 calls in the September quarter of 2025, indicating long-term stress on well-being. This stress is a result of long working hours, financial stress, and disturbed schedules, especially in younger adults, which makes it difficult to achieve high-quality sleep.

Since sleep disturbance is becoming harder to control with lifestyle modifications alone, consumers continue to look to convenient, fast-acting sleep aids. The combination of increasing mental-health issues and ongoing sleep-quality problems provides a consistent base level of demand of sleep aids in various product categories. This dynamic allows sleep aids to maintain a sense of relevance despite the overall value growth leveling off, and sleep issues related to stress becoming increasingly normalized in Australia families. The mental-health burden is a successful way of placing the sleep-aid category in the category of necessary wellness spending.

Australia Sleep Aids Market Challenge

Cost-of-Living Pressures and Pharmacist-Gated Access Constraining OTC Uptake

The financial pressure of the cost of living lowers the discretionary spending on wellness, forcing buyers to be more discerning about the paid sleep solutions. The Australia Bureau of Statistics reported that the Consumer Price Index increased by 3.8% in the twelve months to the December 2025 quarter, which further supports the household vigilance despite the prevalence of sleep issues. Such an inflationary situation forces end users to focus on value and reevaluate premium sleep-aid purchases, especially in the presence of lower-price substitutes in related wellness segments.

At the same time, access friction directs end users to traditional sleep aids. The most important over-the-counter products fall under Schedule 3, requiring the intervention of a pharmacist at the point of sale, which restricts impulse and casual purchases. This regulatory hurdle pushes consumers to mood-and-relaxation dietary supplements and herbal teas that are highly accessible in supermarkets, pharmacies, and health stores without consultation conditions. These options are seen as softer and also contribute to alleviating stress, which puts a substitution pressure on the traditional pharmacist-mediated sleep aids during the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Sleep Aids Market Trend

Indication-Specific Melatonin Solutions Driving Clinical Retail Innovation

Sleep aid product development is becoming more specific to use case than general insomnia. An example is Voquily Jet Lag Relief, a 2 mg melatonin capsule in a blister pack, which was registered on the Australia Register of Therapeutic Goods on 10 April 2025, making jet-lag relief an over-the-counter, pharmacist-only offer. This regulatory acceptance is an indication of manufacturer acknowledgment that consumers are more responsive to clearly defined problem-solution models than general sleep-enhancement claims.

This change is indicative of a more clinical, purpose-driven innovation pipeline whereby formulations are focused on quick sleep onset and circadian rhythm correction during travel as opposed to chronic insomnia treatment. Brands distinguish themselves with indication-based messaging and narrowly specified pack designs, rather than competing with general calming supplements or conventional sleep drugs. This provides a better problem-solution framing in a saturated wellness shelf, allowing manufacturers to not compete directly on price but create different usage occasions. The specificity trend is a structural change in the development, regulation, and marketing of sleep aids in Australia.

Australia Sleep Aids Market Opportunity

International Travel Recovery Expanding Jet Lag–Focused OTC White Space

The long-haul travel patterns provide a viable gap to specific sleep-reset supplements. In February 2025, Australia registered 764,120 short-term resident departures, which highlights the magnitude of travellers who are at risk of experiencing time-zone changes and broken sleep patterns. This represents a large untapped market of products specifically designed to counter jet lag and circadian rhythm disruption, not chronic insomnia therapy or generic relaxation supplements.

By considering jet lag as a unique clinical requirement, manufacturers can develop travel-focused propositions based on pharmacist-only melatonin and neighboring sleep-support formulations without having to directly compete with established insomnia drugs. In April 2025, Voquily Jet Lag Relief was registered on the Australia Register of Therapeutic Goods as a 2 mg melatonin capsule product, which indicates that there are clear regulatory pathways to travel-specific positioning and market development. This blank space enables brands to achieve category leadership in a high-frequency use case, which is backed by rising volumes of international travel and rising awareness of circadian health-management strategies among end-users.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Doxylamine Succinate

- Diphenhydramine

- Melatonin

- Combination Ingredient

- Diphenhydramine + Acetaminophen

- Other Antihistamine-Based Combinations

- Herbal & Traditional Sleep Aids

- Valerian root

- Passionflower

- Chamomile

- Kava

- Multi-Herbal Sleep Blends

The product-type category is dominated by single-ingredient products, which have 52% of the market share. The leadership of this segment is based on the popularity of proven active ingredients like doxylamine succinate, which is present in such brands as Dozile, and the increasing popularity of melatonin. Consumers like these specific solutions because they have been shown to be effective in offering short-term relief of insomnia and in the management of circadian rhythms. The perceived risk is minimized by the clarity of single-ingredient formulations, and the decision-making process is simplified by consumers who want a simple pharmacological intervention.

Although combination herbal preparations and multifunctional supplements are gaining momentum due to their wellness positioning and accessibility benefits, the single-ingredient category is still the most popular when it comes to direct pharmacological intervention that demands measurable results. Specific functionality and clear labelling will attract Australias who are increasingly becoming educated on their sleep needs and the efficacy of ingredients. This category is projected to stay on top until 2032, with further introduction of over-the-counter melatonin products to treat certain conditions, including jet lag relief, which will support the clinical plausibility that is the foundation of single-ingredient dominance.

By Sales Channel

- Retail Online

- Retail Offline

The retail offline channels are the most dominant in sales-channel classification, with 70% of the market. This large proportion indicates the historical role of pharmacies as the initial source of sleep-health consultation and product choice. A large number of effective sleep aids under Schedule 3 must be pharmacist-intervened at the time of purchase, and thus physical retail locations are structurally essential within the existing regulatory framework. Professional consultation in-store is appreciated by consumers, particularly when dealing with more complicated problems like chronic insomnia, drug interactions, or new ingredient safety concerns.

Although offline prevails, online retailing is growing at a very high rate especially in the sale of herbal supplements and lifestyle products that do not need pharmacist clearance at the checkout. Large retailers like Coles and online-specific websites make products such as kava shots and sleep teas more accessible to everyday use, which attracts consumers who want to find wellness solutions that are easy to use and do not require consultation. Nevertheless, the professional control of high-potency aids will keep brick-and-mortar pharmacies as the backbone of Australia sleep-aid distribution during the forecast period, especially with pharmacist-mediated access to scheduled substances being maintained by regulatory authorities.

List of Companies Covered in Australia Sleep Aids Market

The companies listed below are highly influential in the Australia sleep aids market, with a significant market share and a strong impact on industry developments.

- Paladin Labs Inc

- Aspen Pharmacare Australia Pty Ltd

- Havenhall Pty Ltd

- Key Pharmaceuticals Pty Ltd

- Brauer Natural Medicine Pty Ltd

- HW Woods Ltd

- Opella Consumer Healthcare ANZ

- Blackmores Ltd

Competitive Landscape

Australia’s sleep aids market is led by Key Pharmaceuticals (Dozile), leveraging pharmacist-only S3 positioning with doxylamine, while HW Woods (Restavit) and melatonin-based brands such as Brauer, Nature’s Own, and Blackmores compete through herbal and lower-dose alternatives. However, the most significant competitive pressure comes from adjacent vitamins and dietary supplements players including Swisse and Blackmores, whose mood/relaxation formulations (eg magnesium, ashwagandha, kava) benefit from broader retail access and fewer purchase barriers. This regulatory asymmetry constrains OTC sleep aids growth and shifts demand toward multifunctional, lifestyle-positioned solutions. Opportunities lie in targeted propositions such as jet lag (eg Voquily melatonin), menopause-related sleep disruption, and science-backed novel ingredients. Brands that combine clinical credibility with easier access and cross-functional benefits are best positioned to capture incremental share.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Australia Sleep Aids Market Policies, Regulations, and Standards

- Australia Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Australia Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Australia Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Key Pharmaceuticals Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Brauer Natural Medicine Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HW Woods Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Opella Consumer Healthcare ANZ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Blackmores Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Paladin Labs Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Havenhall Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Key Pharmaceuticals Pty Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.