Australia Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)), By Region (Queensland, New South Wales, Victoria, South Australia, Others) ... Read more

|

Major Players

|

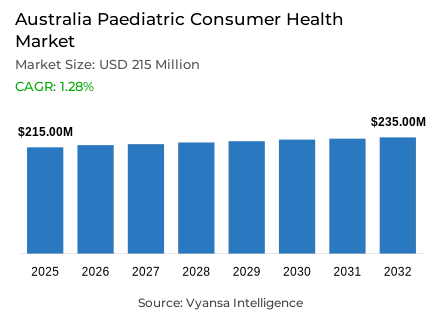

Australia Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

- Paediatric consumer health market size in Australia was valued at USD 215 million in 2025 and is estimated at USD 220.61 million in 2026.

- The market size is expected to grow to USD 235 million by 2032.

- Market to register a CAGR of around 1.28% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 45%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in Australia.

- Top 5 companies acquired around 60% of the market share.

- Johnson & Johnson Pacific Pty Ltd, By-health Co Ltd, JBX Pty Ltd, Pharmacare Laboratories Pty Ltd, Bayer Australia Pty Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Australia Paediatric Consumer Health Market Outlook

Australia paediatric consumers health market is estimated to be worth USD 215 million in 2025 and is expected to increase by USD 220.61 million in 2026 to USD 235 million in 2032 with a CAGR of 1.28% during the forecast period. This gradual rise is due to the growing awareness of preventative care by parents and caregivers who take the initiative to take care of their children. The increased attention to immunity, digestion, and allergy control remains a driving force behind the steady demand in the market.

Paediatric vitamins and dietary supplements had 45% market share within the market. Parents are moving off generic multivitamins to specific formulations, so that daily paediatric requirements like cognitive development and stress relief are being proactively addressed. Also, the prevalence of childhood allergies has increased the dynamism of allergy remedies, whereas the demand of nappy-rash treatments has decreased as a result of a decreasing national birth rate, forcing brands to reposition these creams to more general family skin issues.

In the analysis of the distribution channels, offline retail dominated 80 per cent of the market. Although the physical stores are still the most popular channel of purchase, online platforms and e-commerce are growing at a very high rate due to their convenience and low prices. However, the internet has also increased safety issues especially with unregulated imported melatonin gummies that have caused unintentional overdoses. To this, medical authorities are advising parents to consult professional advice before administering these sleep supplements to avoid unsafe practices.

In the future, the ongoing wellness trend and the high focus on specific nutritional support will continue to be the driving forces of growth. The major producers are likely to keep launching new chewable and gummy products to fill certain dietary gaps and gut health concerns. The companies that work in the paediatric end users health sector can adjust to the changes in the demographics and focus on the clear and high-quality ingredients, which will help them to address the needs of the modern families.

Australia Paediatric Consumer Health Market Growth DriverAllergy Burden Sustains Category Demand

The growing pressure of allergies remains to support demand among paediatric end users in Australia. Allergic disorders are also very relevant in the early childhood stage, thus keeping parents on their guard against products that alleviate the symptoms of allergy, skin irritation, and other related wellness issues. This increases the demand of paediatric allergy remedies, dermatologicals, and supportive health products that can be included in the normal child care.

The demand is comprehensive and repetitive as opposed to single-time treatments. Allergic disease is present in over five million Australians, and food allergy is found in up to one in ten infants. As a result, the management of allergies will always be closely connected with the daily health needs of children, which will continue to generate the interest towards effective paediatric health solutions.

Australia Paediatric Consumer Health Market ChallengeDeclining Births Restrain Infant-Centric Demand

The decline in birth rate poses a definite challenge to paediatric end users, especially in those categories that are closely related to infants and newborns. Goods like nappy-rash ointments have a slower demand creation since their clientele directly relies on the quantity of infants joining the population. Therefore, demographic shrinkage is a major structural limitation of baby-oriented categories.

This is reflected in national birth statistics: the Australian Bureau of Statistics recorded 286,998 births in 2023, a 4.6 per cent decrease on the previous year, and a total fertility rate of 1.50 births per woman. The number of births registered is lower, which means that the growth of infant-led categories is also restricted, forcing brands to work harder to ensure relevance and volume growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Paediatric Consumer Health Market TrendSafety Oversight Reshapes Product Preferences

The notable trends in paediatric end users is the growing significance of product safety, age appropriateness, and regulatory conformity. Parents are also becoming more wary of what they give to children, particularly in the categories of sleep support and allergy treatment. This increases the importance of certified products, better usage instructions and increased confidence in controlled brands.

Recent regulatory action supports this change. In November 2024, the Therapeutic Goods Administration (TGA) stated that oral promethazine hydrochloride products were contraindicated in children under the age of six years and imposed new conditions on almost 50 other oral promethazine brands. In 2025, the TGA tested 18 imported melatonin products and found that 12 of them contained melatonin levels that were significantly different to labelled claims, with one product containing between 118.4 and 416.8% of the stated amount.

Australia Paediatric Consumer Health Market OpportunityMental Wellness Creates New Space for Innovation

The mental wellbeing is an opportunity that is promising among the paediatric end users because parents are increasingly demanding specific assistance in the emotional balance, sleep quality, and cognitive wellness of children. This expands the purpose of paediatric supplements beyond simple nutrition and creates the possibility of products that are placed around particular daily wellbeing requirements.

The opportunity is supported by increased institutional attention to child and adolescent mental health in Australia. A total of 6,500 parents or carers of children aged 4-17 years and 3,500 adolescents are now involved in national research, after the government had previously invested AUD 8.1 million in this field. With the growing focus on child mental wellbeing, brands with well-defined and trusted wellness solutions will have more space to innovate and differentiate.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with the largest market share in the product category is paediatric vitamins and dietary supplements which occupy 45⠻% of the market. Their dominance is the result of the increased role of preventive care in the health of children, as parents are more willing to choose products that help to maintain immunity, digestion, growth, and everyday wellbeing. This makes the segment more applicable to everyday use as opposed to occasional treatment requirements.

Its power is also motivated by wide applicability in various issues of child health. The products within this category are often placed around certain needs, including fussy eating, iron support, gut health, and sleep support, which increases the engagement and repeat purchases. Paediatric vitamins and dietary supplements have broader use occasions compared to narrower remedy-based categories, which assist the segment to maintain its leading market position.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment that has the largest market share in the sales channel is offline retail which occupies 80% of the market. This channel is still dominant because parents still like to shop in physical stores when buying health products of children, as they can easily recognize the brands they trust and make sure in their purchases. Pharmacies, supermarkets, and health retail stores continue to be at the center of category visibility and accessibility.

Its leadership is also backed by the strong shelf position of key brands in big box stores. Popular products can be found in the stores like Woolworths, Coles, and Chemist Warehouse, which makes offline shopping not only convenient but also familiar to the family buyers. Despite the growing importance of online platforms, physical retail still enjoys the advantage of instant access to products, greater trust, and a role in daily shopping.

List of Companies Covered in Australia Paediatric Consumer Health Market

The companies listed below are highly influential in the Australia paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Johnson & Johnson Pacific Pty Ltd

- By-health Co Ltd

- JBX Pty Ltd

- Pharmacare Laboratories Pty Ltd

- Bayer Australia Pty Ltd

- Nice Pak Products Pty Ltd

- Haleon Australia Pty Ltd

- Reckitt Benckiser (Australia) Pty Ltd

- Church & Dwight (Australia) Pty Ltd

- iNova Pharmaceuticals (Australia) Pty Ltd

Competitive Landscape

Australia paediatric consumer health market features a competitive landscape led by strong multinational and domestic players, particularly those active in paediatric vitamins, dermatological care and allergy remedies. Pharmacare Laboratories Pty Ltd holds the leading position, supported by its paediatric supplements portfolio including Nature’s Way Kids Smart Vita Gummies and Bioglan Health Kids. Bayer Australia Pty Ltd follows with brands such as Bepanthen, Amolin, Claratyne and Demazin. Nice Pak Products Pty Ltd ranks third through its widely recognised Sudocrem. Other notable competitors include Haleon with Panadol and Centrum, Reckitt Benckiser with Nurofen, and Johnson & Johnson with Zyrtec.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Australia Paediatric Consumer Health Market Policies, Regulations, and Standards

- Australia Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Australia Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Queensland

- New South Wales

- Victoria

- South Australia

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Australia Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Pharmacare Laboratories Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nice Pak Products Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser (Australia) Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson Pacific Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- By-health Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- JBX Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Church & Dwight (Australia) Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- iNova Pharmaceuticals (Australia) Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pharmacare Laboratories Pty Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.