Argentina Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (Queensland, New South Wales, Victoria, South Australia, Others) ... Read more

|

Major Players

|

Argentina Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

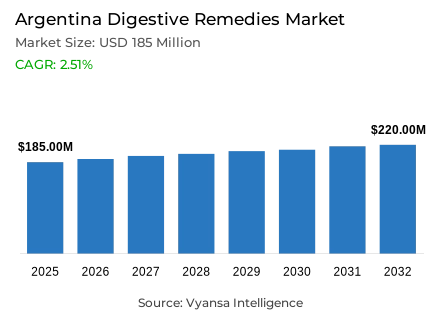

- Digestive remedies market size in Argentina was valued at USD 185 million in 2025 and is estimated at USD 195 million in 2026.

- The market size is expected to grow to USD 220 million by 2032.

- Market to register a CAGR of around 2.51% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing digestive remedies in Argentina.

- Top 5 companies acquired around 70% of the market share.

- Spedrog Caillon SAI y C, Mega Labs Argentina SAU, Instituto Sanitas Arg SACIPQyM, Laboratorio Elea SACIF y A, Opella Healthcare Argentina SAU etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Argentina Digestive Remedies Market Outlook

The Argentina digestive remedies market size was valued at USD 185 million in 2025 and is projected to grow from USD 195 million in 2026 to USD 220 million by 2032, exhibiting a CAGR of 2.51% during the forecast period. Growth is supported by regulatory actions that expand access to widely used digestive treatments. In March 2024, Argentina’s Ministry of Health issued Resolution 284/2024 instructing ANMAT to review sales conditions for several medicines. As a result, 22 molecules moved from prescription to over-the-counter status in May 2024, improving availability and convenience for consumers seeking treatment for common gastrointestinal discomforts.

Greater OTC availability is particularly important for commonly used treatments such as proton pump inhibitors, including omeprazole, esomeprazole, pantoprazole, and lansoprazole. Wider access allows consumers to purchase familiar digestive remedies more easily, supporting steady demand within the category. This dynamic also strengthens the position of indigestion and heartburn products, which hold around 60% share under product type, as consumers frequently rely on these treatments to manage recurring symptoms such as acidity and stomach discomfort.

At the same time, consumer preferences are evolving toward herbal and plant-based digestive remedies. Many consumers increasingly look for solutions that avoid artificial or chemical ingredients, encouraging the growth of natural digestive support products. This shift is also reflected in product development activity, such as the February 2024 launch of Hepatalgina 9 Herbs by Laboratorio Elea SACIF y A for temporary relief of symptoms including stomach pain, abdominal bloating, flatulence, and colic.

Distribution patterns also shape how digestive remedies reach consumers. Retail offline channels account for about 90% of sales because regulations prohibit the purchase of OTC medicines online or through other non-pharmacy channels. Pharmacies therefore remain the main point of purchase, supported by a network of 17,306 outlets nationwide, ensuring broad access to digestive treatments while maintaining strong product visibility across physical retail locations.

Argentina Digestive Remedies Market Growth DriverOTC Access Expands Everyday Use

A key driver for Argentina’s digestive remedies market is the wider consumer access created by the shift of several molecules from prescription to over-the-counter status. This regulatory change improves availability for commonly used digestive treatments, especially proton pump inhibitors such as omeprazole, esomeprazole, pantoprazole, and lansoprazole. This makes digestive remedies easier to purchase and supports stronger category demand, particularly for products already familiar to consumers.

This driver is backed by official regulation. Argentina’s Ministry of Health issued Resolution 284/2024 in March 2024, instructing ANMAT to review sales conditions, and 22 molecules moved from Rx to OTC status in May 2024. This directly supports faster consumer access to widely used digestive products.

Argentina Digestive Remedies Market ChallengeNatural Alternatives Intensify Competitive Pressure

A major challenge for the category is the growing consumer preference for natural digestive support, which limits the growth potential of conventional drug-based remedies. “Dietéticas” continue expanding and capturing sales from pharmacies by offering herbal digestive remedies. This creates stronger competition for traditional digestive products, especially among consumers who want remedies without artificial or chemical ingredients.

The challenge also becomes more visible because these alternative outlets are building momentum within a highly regulated market. Pharmacies remain the leading channel and account for 17,306 points of sale nationwide, yet health and personal care stores are the most dynamic channel due to the expansion of dietéticas. This means conventional digestive remedies now compete not only with other medicines, but also with a broader natural-products ecosystem.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Argentina Digestive Remedies Market TrendHerbal Positioning Gains Stronger Consumer Appeal

A clear trend in Argentina is the stronger pull of herbal and plant-based digestive solutions. Local consumers increasingly prefer natural products that do not contain artificial or chemical additives, which is keeping demand for herbal digestive remedies robust. This is shifting the category toward formulations that feel gentler, more familiar, and better aligned with wider wellness preferences.

Brand activity reflects this movement. In February 2024, Laboratorio Elea SACIF y A introduced Hepatalgina 9 Herbs, positioned for temporary relief of gastrointestinal symptoms such as stomach pain, abdominal bloating, flatulence, and colic. This launch shows how companies are using multi-herb and natural-style concepts to match changing consumer expectations in digestive care.

Argentina Digestive Remedies Market OpportunityProton Pump Inhibitors Open a Bigger Growth Window

A strong opportunity in Argentina lies in proton pump inhibitors, as wider OTC availability and broad consumer familiarity increase their commercial potential. Proton pump inhibitors are the most dynamic subcategory over the forecast period, supported by Laboratorio Elea’s omeprazole development and the growing recognition of these products as effective solutions for major digestive ailments. Their presence in both affordable brands and generics also improves reach.

This opportunity is reinforced by official policy action. Resolution 284/2024 begins the review process that enables broader non-prescription access, and the omeprazole, esomeprazole, pantoprazole, and lansoprazole move from prescription only to OTC status in April–May 2024. That expands visibility, accessibility, and price competition for a high-use product group.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Argentina Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share around product type under digestive remedies, where indigestion & heartburn remedies hold 60% share. This leading position fits well and shows strong momentum in proton pump inhibitors and highlights the positive effect of the OTC shift for commonly used molecules such as omeprazole, esomeprazole, pantoprazole, and lansoprazole. These products are widely recognised and used for frequent digestive discomfort, which helps the segment maintain its dominance.

Their position is also supported by accessibility and familiarity. As more commonly used digestive molecules become easier to buy, consumers can address recurring symptoms more quickly through well-known remedy types. This strengthens the role of indigestion and heartburn remedies as the core product group within digestive care.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share around the sales channel, where retail offline holds 90% of the market. This dominance is consistent, which explains that government regulations prohibit the purchase of OTC remedies online or through other offline channels outside pharmacies. As a result, physical pharmacy networks remain central to digestive remedy sales across Argentina.

The scale of this channel is substantial. Pharmacies account for 17,306 points of sale nationwide, with 80% of sales concentrated in just 20% of these outlets. This shows how strongly retail offline continues to anchor product availability, visibility, and purchase behaviour, even as dietéticas capture some demand for herbal alternatives.

List of Companies Covered in Argentina Digestive Remedies Market

The companies listed below are highly influential in the Argentina digestive remedies market, with a significant market share and a strong impact on industry developments.

- Spedrog Caillon SAI y C

- Mega Labs Argentina SAU

- Instituto Sanitas Arg SACIPQyM

- Laboratorio Elea SACIF y A

- Opella Healthcare Argentina SAU

- GlaxoSmithKline Argentina SA

- Laboratorios Bago SA

- Bayer Argentina SA

- Federacion Argentina de Cooperativas Farmaceuticas

- Monserrat y Eclair SA

Competitive Landscape

The competitive landscape of digestive remedies in Argentina is led by established pharmaceutical companies with strong brand portfolios and active marketing strategies. Laboratorio Elea SACIF y A leads the market with a value share of 27.9%, largely supported by its strong position in proton pump inhibitors through the Aziatop brand and the development of omeprazole-based products widely used to treat digestive ailments. Opella Healthcare Argentina SAU follows with a value share of 16.9%, with its Buscapina portfolio performing strongly in treatments for IBS and supported by multi-platform marketing campaigns promoting Buscapina Duo. Competition in the category has also intensified following regulatory changes that shifted several digestive remedy molecules from prescription-only to over-the-counter status, increasing accessibility and driving demand. At the same time, companies continue to face growing competition from herbal digestive remedies offered through expanding health and personal care stores known as dietéticas.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Australia Digestive Remedies Market Policies, Regulations, and Standards

- Australia Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Australia Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Queensland

- New South Wales

- Victoria

- South Australia

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Australia Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Johnson & Johnson Pacific Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Care Pharmaceuticals Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Norgine Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser (Australia) Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Procter & Gamble Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestle Australia Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Opella Consumer Healthcare ANZ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson Pacific Pty Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.