Vietnam Diagnostic Labs Market Report: Trends, Growth and Forecast (2026-2032)

By Lab Type (Single/Independent Laboratories, Hospital-based Laboratories, Physician Office Laboratories, Others), By Testing Services (Physiological Function Testing, General & Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing, Others), By Disease (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Odontology, Others), By Revenue Source (Healthcare Plan, Out-of-Pocket, Public System), By Test Type (Pathology, Radiology), By End User (Referrals, Walk-ins, Corporate Clients) ... Read more

|

Major Players

|

Vietnam Diagnostic Labs Market Statistics and Insights, 2026

- Market Size Statistics

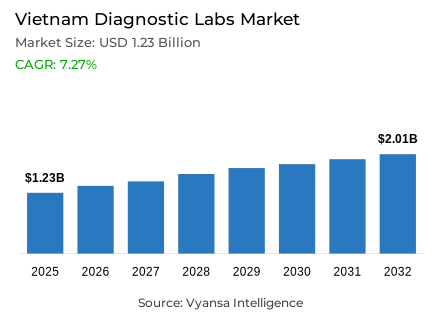

- Diagnostic labs market size in Vietnam was estimated at USD 1.23 billion in 2025.

- The market size is expected to grow to USD 2.01 billion by 2032.

- Market to register a CAGR of around 7.27% during 2026-32.

- Lab Type Shares

- Hospital-based laboratories grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing diagnostic labs in Vietnam.

- Top 5 companies acquired around 60% of the market share.

- Hi-Lab Medical Testing Center, Medilab Vietnam, CHEK Genomics Vietnam, Diag Laboratories, Pathlab Vietnam etc., are few of the top companies.

- Testing Services

- General & clinical testing grabbed 45% of the market.

Vietnam Diagnostic Labs Market Outlook

Vietnam's diagnostic labs market estimated at USD 1.23 billion in 2025 and is projected to reach USD 2.01 billion by 2032, growing at a CAGR of approximately 7.27% during 2026-2032. This expansion is fundamentally driven by near-universal health insurance coverage, which reached 94.2% of the population in 2024-over 95 million participants-and is expected to climb to 96.46% by end-May 2025. As more people access insured healthcare services through 3,016 contracted facilities and over 10,000 communal health stations, routine diagnostic testing remains central to clinical decisions across primary care, hospitals, and chronic disease management, creating consistent demand for laboratory examinations nationwide.

Hospital-based laboratories control 55% of the market, as the main testing facility of both insured outpatient and inpatient services. These facilities enjoy the advantage of 24/7 operations, on-site phlebotomy, emergency processes, and direct access to clinicians, which makes them have quick turnaround times. In the testing services, General and Clinical Testing has 45% of the market share. This leadership is fueled by the high-frequency routine diagnostics of hematology, clinical chemistry, and urinalysis, which produce sustained volumes in all care settings and across the seasons.

The market is facing issues on standardisation of quality. A national survey of 240 laboratories showed that there were differences in performance, although 90% of samples met transport standards. The remaining problems are equipment malfunction, poor calibration, third-party reagents, and unfinished validation. This means that laboratories have to invest continuously in calibration procedures, documentation, and employee training to maintain a consistent test outcome among various instruments and methodologies.

Digital transformation presents both opportunities and challenges. While 99.5% of healthcare facilities submit electronic insurance claims and all public hospitals operate information systems, only 6% have deployed electronic medical records. New reimbursement policies effective from 2025-2026—including remote consultation coverage and 100% payment rates for near-poor cardholders—favor hybrid care models combining teleconsultations with laboratory diagnostics, strengthening the business case for home sample collection, courier logistics, and networked reference laboratories operating within established insurance pathways.

Vietnam Diagnostic Labs Market Growth DriverExpanding Insurance Infrastructure Accelerates Testing Accessibility

The almost universal coverage of health insurance in Vietnam makes it easier to access diagnostic laboratory services and protect finances in case of illness. Vietnam Social Security (VSS) reports that in 2024, the coverage was 94.2% of the population, including over 95 million members. This number is expected to reach 96.46% by the end of May 2025. With more patients receiving insured services, routine diagnostic tests remain a pillar of clinical decision-making in primary care centers, hospitals, and chronic-care follow-ups, thus maintaining a consistent demand of laboratory tests.

This extensive coverage creates a large reimbursement-based provider network that supports ongoing laboratory use. According to VSS, 3,016 health-care facilities are contracted to insured services, and over 10,000 communal health stations and regional polyclinics are offering health-insurance care. In the case of diagnostic laboratories, these broad access points maintain a broad denominator of sample inflow and enable the consistent utilization of instruments and reagents, thus establishing a strong base of market expansion in both urban and rural settings.

Vietnam Diagnostic Labs Market ChallengeQuality Standardization Challenges Across Fragmented Laboratory Networks

It is challenging to guarantee consistency of test results across the heterogeneous laboratory environment of Vietnam when instruments, reagents, and methodologies differ significantly across locations. A national clinical biochemistry external quality assessment (EQA) of 240 laboratories in five rounds between October 2024 and February 2025, and assessing 15 biochemical parameters, revealed performance differences across methods and testing cycles, thus revealing long-standing gaps in standardisation across the market.

Despite the fact that logistical provisions are usually up to the set standards, there are still analytical issues that undermine quality results. The above EQA study shows that over 90% of samples meet the necessary temperature and transport requirements before analysis; however, unacceptable results persist, which can be explained by equipment malfunction, insufficient calibration and maintenance, third-party reagents, and missing validation data in many open-system setups. To address these quality deficiencies, laboratories need to invest in calibration discipline on a continuous basis, implement extensive documentation systems, and promote ongoing staff competence development.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Vietnam Diagnostic Labs Market TrendDigitalization Momentum Drives Laboratory Information System Integration

The processing of electronic claims and hospital information-technology systems are increasingly affecting the ordering, billing, and reporting of diagnostic tests across the health-care network in Vietnam. An article in the Vietnam Investment Review (2024) citing World Bank health experts confirms that all public hospitals in Vietnam have installed and are operational with a hospital information system, and that 99.5% of health-care facilities are submitting electronic health-insurance claims to Vietnam Social Security, thus establishing standardised digital workflows to laboratory reimbursement.

However, the overall digitisation of the hospital environment is still uneven, which makes interoperability a vital business concern of diagnostic laboratories. According to the same source, 94 out of 1,500 hospitals (6%) have implemented electronic medical records as of 2024, thus creating integration issues. This information gap forces laboratories to invest in laboratory information system (LIS) / hospital information system (HIS) interfaces, middleware platforms, and barcode workflows to ensure a smooth flow of results between the current billing systems and to scale as EMR environments continue to expand throughout the health-care industry.

Vietnam Diagnostic Labs Market OpportunityReimbursement Policy Reforms Enable Decentralized Testing Models

The changing reimbursement models offer significant opportunities to diagnostic providers to go beyond the traditional facility-based service delivery models. According to Vietnam Social Security, the Law No. 51/2024/QH15, which will come into effect on 1 July 2025, will cover such services as remote medical consultations. Moreover, starting 1 January 2026, the Ministry of Health has assured that near-poor cardholders will receive an increase in payment rate to 100% of covered costs, rather than 95%, which will reduce financial barriers to vulnerable groups.

Favorable funding allocations strengthen this strategic change to more accessible diagnostic services. According to VSS, the health insurance fund spends 92% of its funds on medical checkups and treatments, the rest on preventive care and administration. Simultaneously, these policies prefer hybrid care models, i.e., teleconsultations with laboratory diagnostics, and strengthen the business case of home sample collection, courier logistics, and networked reference labs working within the established reimbursement pathways.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Vietnam Diagnostic Labs Market Segmentation Analysis

By Lab Type

- Single/Independent Laboratories

- Hospital-based Laboratories

- Physician Office Laboratories

- Others

Hospital-based laboratories command the leading position in the Lab Type segment with 55% market share, reflecting their strategic role as the primary testing venue for insured outpatient and inpatient care. Hospitals serve as the first contact point for end users seeking covered services, enabling routine tests such as complete blood counts, chemistry panels, and microbiology to be ordered at the point of treatment and processed in-house for rapid turnaround and seamless clinical coordination. They also benefit from integrated on-site phlebotomy and pre-procedure testing tied directly to hospital admissions.

This dominance reflects infrastructure concentration and operational advantages that limit sample migration to standalone facilities. Hospital laboratories operate around-the-clock, support emergency workflows, and maintain close proximity to clinicians, ensuring immediate result availability for critical decision-making. While independent and private laboratories remain important for convenience, corporate health screenings, and specialized testing, they typically depend on referral relationships and serve complementary rather than primary testing needs.

By Testing Services

- Physiological Function Testing

- General & Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

- Others

General & Clinical Testing holds the dominant position in the Testing Services segment with 45% market share, reflecting the high-frequency nature of routine diagnostic work across Vietnam's healthcare system. This category encompasses basic hematology, clinical chemistry, urinalysis, and common screening procedures, generating sustained volumes across all seasons and care settings, from outpatient consultations to chronic disease follow-ups and annual health examination packages offered to end users.

The standardized and repetitive nature of these tests drives laboratories to prioritize automation, rigorous quality control measures, and rapid turnaround times to manage daily volume peaks from clinics and hospital wards efficiently. Specialized services, including advanced pathology, molecular diagnostic panels, and genetic testing, add complexity and require stricter validation protocols, but they serve narrower patient cohorts and are scheduled more selectively compared to routine clinical work that forms the backbone of laboratory operations.

List of Companies Covered in Vietnam Diagnostic Labs Market

The companies listed below are highly influential in the Vietnam diagnostic labs market, with a significant market share and a strong impact on industry developments.

- Hi-Lab Medical Testing Center

- Medilab Vietnam

- CHEK Genomics Vietnam

- Diag Laboratories

- Pathlab Vietnam

- Quest Laboratories Vietnam

- Labcare Diagnostics Vietnam

- Life Medical Laboratory Vietnam

- Vinmec Laboratory System

- Hoan My Diagnostic Laboratories

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Vietnam Diagnostic Labs Market Policies, Regulations, and Standards

- Vietnam Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Vietnam Diagnostic Labs Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Lab Type

- Single/Independent Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Testing Services

- Physiological Function Testing- Market Insights and Forecast 2022-2032, USD Million

- General & Clinical Testing- Market Insights and Forecast 2022-2032, USD Million

- Esoteric Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Testing- Market Insights and Forecast 2022-2032, USD Million

- Non-invasive Prenatal Testing- Market Insights and Forecast 2022-2032, USD Million

- COVID-19 Testing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Disease

- Cardiology- Market Insights and Forecast 2022-2032, USD Million

- Oncology- Market Insights and Forecast 2022-2032, USD Million

- Neurology- Market Insights and Forecast 2022-2032, USD Million

- Orthopedics- Market Insights and Forecast 2022-2032, USD Million

- Gastroenterology- Market Insights and Forecast 2022-2032, USD Million

- Gynecology- Market Insights and Forecast 2022-2032, USD Million

- Odontology- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source

- Healthcare Plan- Market Insights and Forecast 2022-2032, USD Million

- Out-of-Pocket- Market Insights and Forecast 2022-2032, USD Million

- Public System- Market Insights and Forecast 2022-2032, USD Million

- By Test Type

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Radiology- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Referrals- Market Insights and Forecast 2022-2032, USD Million

- Walk-ins- Market Insights and Forecast 2022-2032, USD Million

- Corporate Clients- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Lab Type

- Market Size & Growth Outlook

- Vietnam Single/Independent Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Hospital-based Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Physician Office Laboratories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Testing Services- Market Insights and Forecast 2022-2032, USD Million

- By Disease- Market Insights and Forecast 2022-2032, USD Million

- By Revenue Source- Market Insights and Forecast 2022-2032, USD Million

- By Test Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Diag Laboratories

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pathlab Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quest Laboratories Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Labcare Diagnostics Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Life Medical Laboratory Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hi-Lab Medical Testing Center

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medilab Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CHEK Genomics Vietnam

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vinmec Laboratory System

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hoan My Diagnostic Laboratories

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Diag Laboratories

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Lab Type |

|

| By Testing Services |

|

| By Disease |

|

| By Revenue Source |

|

| By Test Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.