UK Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

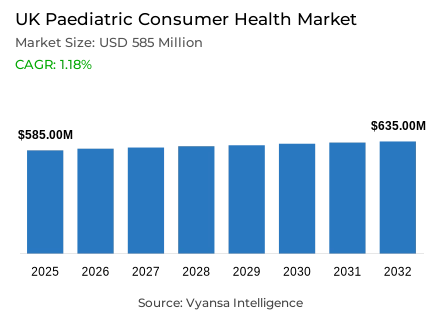

- Paediatric consumer health market size in UK was valued at USD 585 million in 2025 and is estimated at USD 604.95 Million in 2026.

- The market size is expected to grow to USD 635 million by 2032.

- Market to register a CAGR of around 1.18% during 2026-32.

- Product Type Shares

- Paediatric analgesics grabbed market share of 40%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in UK.

- Top 5 companies acquired around 50% of the market share.

- Haleon Plc, Thornton & Ross Ltd, Omega Pharma Ltd, McNeil Healthcare (UK) Ltd, Reckitt Benckiser Group Plc (RB) etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

UK Paediatric Consumer Health Market Outlook

The UK paediatric consumer health market was valued at USD 585 million in 2025 and is projected to grow from USD 604.95 million in 2026 to USD 635 million by 2032, reflecting a compound annual growth rate of 1.18% over the forecast period. but structurally intact, sustained by rising parental focus on proactive child wellness and a broadening range of specialised products entering the end user's consideration set.

Everyday-use categories anchored to common childhood health needs keep demand active and consistent. Parents are managing minor ailments at home with greater confidence, turning to accessible non-prescription options before escalating to clinical care. Pain relief and skin protection sit at the centre of this behavioural pattern, generating steady repeat volume across household budgets.

Category performance reflects both evolving family structures and broader demographic movement across the country. Paediatric Analgesics hold the leading product type position at 53% market share, driven by rising child participation in sports and organised physical activity. Nappy rash treatments record particularly strong commercial momentum, benefiting from widespread household accessibility and use extending beyond the infant care context.

Retail Offline captures 80% of total market sales. Physical pharmacies remain the preferred purchase channel — combining trust, familiarity, and direct pharmacist guidance in a way that digital platforms have not yet replicated at scale. Digital is gaining ground, as pharmacy operators invest in delivery infrastructure, competitive pricing, and targeted end user incentives, but the market remains firmly pharmacy-led.

UK Paediatric Consumer Health Market Growth DriverPreventive Nutrition Is Becoming a Consistent and Everyday Parental Priority

Among the most structurally reliable growth drivers in the UAE paediatric consumer health market, the deepening shift toward prevention-oriented home management stands out clearly. Parents are managing minor childhood ailments with non-prescription products at earlier intervention points and with greater confidence than in prior periods. Pain relief and skin protection anchor this shift most visibly, where brand familiarity, established safety credentials, and ease of access drive the purchase decision.

Demographic expansion reinforces this direction. The Federal Competitiveness and Statistics Centre reports that the UAE population reached 11.29 million in 2024, a 5.7% increase from 2023 a base that directly expands the addressable end user pool for child-focused health spending. Within this growing population, broader product availability and strengthening wellness awareness are reinforcing interest in paediatric offerings that families can maintain conveniently at home as part of routine preventive care.

UK Paediatric Consumer Health Market ChallengeWeakening Demographic Trends Are Limiting Natural Category Expansion

Accurate demand forecasting in UAE paediatric consumer health faces a challenge that is both persistent and structural: the addressable base of child end users shifts in ways that conventional demographic indicators do not reliably capture. Birth rates trend gradually upward. Category growth stays positive. Yet the expatriate-heavy population structure responds to employment cycles and international migration patterns in ways that alter the real size of the paediatric end user base materially and sometimes rapidly.

Corporate hiring cycles bring single professionals into the country at one phase and family households at another directly altering the underlying need for paediatric products without following a predictable pattern. Brands and distributors that rely too heavily on birth-rate direction alone risk commercially misleading their planning assumptions. This structural uncertainty ripples into product supply decisions, brand investment allocation, and channel strategy development across the category. shifts is the depth and consistency of the underlying demand base and in a market environment where demographic composition can reset faster than forecasting cycles allow, that distinction carries real commercial weight.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Paediatric Consumer Health Market TrendPharmacy-Led Care Is Becoming More Deeply Embedded in Family Health Management

Child-friendly supplement formats are gaining meaningful commercial traction. Paediatric dietary supplements attract increasing parental interest as options that are easier to administer and more readily accepted by children in daily routines. Oral sprays represent the clearest expression of this shift moving from predominantly online availability into mainstream pharmacy channels and drawing end user attention through simplified dosing mechanics and a more pleasant administration experience relative to conventional tablets or syrups.

Alongside format evolution, product perception is shifting. Parents show a growing preference for formulations positioned as gentler, safer, and more naturally derived particularly for products applied directly to children or used frequently. In the nappy rash treatment segment, this orientation creates competitive pressure on established conventional brands to modernise their positioning or risk losing ground to naturally-framed alternatives. Together, format innovation and natural product preference are directing the broader category toward convenience-oriented and reassurance-driven purchasing choices.

UK Paediatric Consumer Health Market OpportunityFlu Prevention Programming Is Opening a New Strategic Lane for Paediatric Brands

State-backed child wellness initiatives, social media influence on parenting behaviour, and expanding technology-enabled health management practices are converging to create well-defined commercial space. The Ministry of Health and Prevention reports that the Masar project expanded from 15 schools serving 12,600 students in its first year to 83 schools and 137,828 students in 2024, with more than 2,000 teachers trained during 2024 to support student health across participating institutions. Institutional reach of that scale gives paediatric wellness themes a platform that commercial marketing alone cannot replicate.

Brands have a credible and addressable opportunity within this environment. Specialised supplements, child health monitoring tools, and targeted wellness solutions for younger end users each find natural entry points as families grow more comfortable with prevention-led care and digital health monitoring. Social media figures are already active in this space promoting clean-label products, natural remedy alternatives, and technology-supported health habits to parenting audiences at scale. Products that combine everyday convenience, meaningful health support, and genuine relevance to children's daily lives are positioned to build sustained awareness and demand across this channel.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with highest market share under Product Type is Paediatric Analgesics, accounting for 53% of the total market. This clear leadership reflects the fundamental and recurring role pain relief plays in everyday child healthcare management. Parents need safe, trusted, accessible options for addressing minor discomfort at home without requiring clinical consultation and analgesics meet that need consistently. Rising child participation in sports and organised physical activity increases the frequency of relevant purchase occasions, expanding demand beyond fever management into aches and short-term pain relief.

Household familiarity reinforces this position. Repeat purchasing behaviour among parents already confident in handling minor childhood ailments keeps analgesics central to the home health management toolkit. As the first-response purchase before professional care escalation, the segment maintains its primary role as the category's volume and value driver throughout the forecast period.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

The segment with highest market share under Sales Channel is Retail Offline, accounting for 80% of the total market. Physical pharmacies hold this position for reasons that extend beyond habit a strict regulatory environment governing child health product promotion, combined with the genuine reassurance that familiar brands in a professional setting provide, make offline the preferred and trusted purchase point. Pharmacist guidance functions as a meaningful and often decisive factor in the final purchase decision for paediatric products.

Offline pharmacy's advantage is structural. Immediate product access combined with real-time professional advice at the point of need creates a form of convenience that digital channels have not yet fully replicated in this category. Parents purchasing health products for children are less willing to experiment with unfamiliar products or sellers a preference that reinforces offline dominance regardless of digital channel improvements. Retail online channels are expanding their commercial presence through improved delivery infrastructure, competitive pricing, and end user incentive programmes, but offline pharmacies retain a stronger foundation of trust, accessibility, and professional interaction that keeps the segment firmly dominant across the UAE paediatric consumer health market.

List of Companies Covered in UK Paediatric Consumer Health Market

The companies listed below are highly influential in the UK paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Haleon Plc

- Thornton & Ross Ltd

- Omega Pharma Ltd

- McNeil Healthcare (UK) Ltd

- Reckitt Benckiser Group Plc (RB)

- Teva UK Ltd

- Seven Seas Ltd

- Vitabiotics Ltd

- Ernest Jackson Ltd

- Boots UK Ltd

Competitive Landscape

The UK paediatric consumer health market in 2025 is led by McNeil Healthcare (UK) Ltd, which maintains its top position through the trusted Calpol brand, widely recommended by pharmacists and strongly associated with childhood pain relief and post-vaccination care. Medipharma is emerging as the most dynamic competitor, driven by strong growth of Optibac in paediatric probiotics, reflecting rising interest in children’s gut health and natural preventative care. Competition is increasingly concentrated in paediatric vitamins and dietary supplements, the main engine of category growth, supported by premiumisation and innovation. Brands are also using IP licensing to strengthen appeal, with examples including Natures Aid’s Bluey range and Haliborange’s Disney-themed vitamins. Pharmacies remain the most trusted channel, while digital health platforms and e-commerce are expanding market reach.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- United Kingdom Paediatric Consumer Health Market Policies, Regulations, and Standards

- United Kingdom Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- United Kingdom Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- United Kingdom Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United Kingdom Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United Kingdom Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United Kingdom Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United Kingdom Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- United Kingdom Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- McNeil Healthcare (UK) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser Group Plc (RB)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teva UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Seven Seas Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vitabiotics Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thornton & Ross Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Omega Pharma Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ernest Jackson Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boots UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- McNeil Healthcare (UK) Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.