Global Titanium Trichloride Market Report: Trends, Growth and Forecast (2026-2032)

By Grade (Catalyst Grade, Industrial Grade, Reagent Grade, Custom/High-Purity Grade), By Form (Solid, Aqueous/Acidic Solution, Solvent Complex, Catalyst Component), By Application (Polyolefin Production, Organic Synthesis, Inorganic Chemical Synthesis, Research & Development), By End-User (Polymer & Plastics Industry, Chemical & Petrochemical Industry, Pharmaceutical & Fine Chemicals, Academic & Research Institutions, Universities & Research Labs), By Sales Channel (Direct, Chemical Distributors, Lab Catalog/E-commerce), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Titanium Trichloride Market Statistics and Insights, 2026

- Market Size Statistics

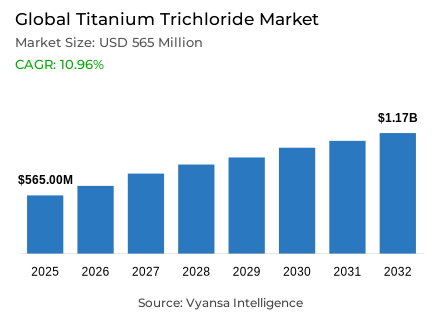

- Titanium trichloride market size in Global was estimated at USD 565 million in 2025.

- The market size is expected to grow to USD 1.17 billion by 2032.

- Market to register a CAGR of around 10.96% during 2026-32.

- Grade Shares

- Catalyst grade grabbed market share of 50%.

- Competition

- More than 20 companies are actively engaged in producing titanium trichloride.

- Top 5 companies acquired around 70% of the market share.

- TOHO Titanium Co. Ltd., Osaka Titanium Technologies Co. Ltd., Cangzhou Heli Chemical Co. Ltd., Tronox Holdings plc, The Chemours Company etc., are few of the top companies.

- End-User

- Polymer & plastics industry grabbed 55% of the market.

- Region

- Asia Pacific leads with a 45% share of the global market.

Global Titanium Trichloride Market Outlook

The Global titanium trichloride market is in a stage of fast growth due to the fact that it is an essential component in the manufacture of high volume plastics. The market is estimated to be USD 565 million in 2025 and is expected to exceed USD 1.17 billion in 2032. This strong growth is a CAGR of about 10.96 % over the 202632 period, driven by stable polyolefin plant run-rates and a world plastics production of over 436 metric tonnes in the last few years.

The polymer and plastics industry forms the backbone of the market, contributing 55 % of the total demand. Titanium trichloride is an important ingredient in Ziegler-Natta catalyst systems, which are required in the polymerization of olefins to polyethylene and polypropylene. With manufacturers focusing on stable supply of catalysts and quality production inputs to maintain the huge global trade, this end-user segment is the main contributor to market stability and growth.

Technical specifications are also a defining factor in market structure with catalyst-grade material having a market share of 50 per cent. This grade is particularly sought after by polymer manufacturers to maintain a close control over catalyst activity and trace impurities, which are crucial to the attainment of the desired material properties in high-performance plastics. Although laboratory and technical grades are helping to sustain the emerging R&D in grid storage and titanium-based flow batteries, the predictable, repeat demand of large-scale resin plants gives the catalyst-grade TiCl 3 the lead.

Asia-Pacific is the most dominant region with 45 per cent of the world market. The high density of polymer manufacturing centers and the huge supply of titanium mineral concentrates, especially in China, supports this leadership. Asia-Pacific has access to almost one-third of the world ilmenite production, and well-developed logistics systems to transport corrosive and water-reactive chemicals, which will keep the region the main center of titanium trichloride consumption and distribution by 2032.

Global Titanium Trichloride Market Growth Driver

Global Polyolefin Scale Sustains TiCl₃ Demand

The demand of titanium trichloride is still strongly associated with the production of polypropylene and polyethylene because it provides titanium to Ziegler-Natta catalyst systems used in the olefin polymerization to high-volume polyolefins. Titanium tetra-, or trichlorides with organo-, or aluminum co-catalysts are often used as industrial catalysts; as a result, steady run-rates of polyolefin plants create a steady demand of catalyst raw material.

This connection is essential since the plastics throughput is high. UNCTAD estimates that in 2023, the world produced 436 million metric tons of plastic, and plastic trade was more than US1.1 trillion, or about 5 per cent of global merchandise trade. On this scale, manufacturers are concerned with a stable and consistent supply of catalysts, thus maintaining a consistent purchase of titanium trichloride as a standard supply.

Global Titanium Trichloride Market Challenge

Hazardous Handling Raises Logistics Costs

The logistics of titanium trichloride are under constant compliance requirements because transport authorities categorize TiCl3 mixtures as corrosive (hazard class 8). According to the CAMEO datasheet of NOAA, TiCl3 crystals react with moist air and water, producing heat and hydrogen chloride fumes, and classifies the substance as water-reactive and air-reactive. These properties require more stringent packaging, dry/inert handling, and the use of trained operators in the supply chain.

The necessity of the so-called hazmat discipline is supported by incident data. According to the National Transportation Statistics Table 2-6 of the U.S. Bureau of Transportation Statistics, there were 24,289 hazardous-materials transportation incidents in 2023 and 27,413 incidents in 2024. Although these numbers represent all the hazardous materials, they highlight the high level of scrutiny of the reporting and risk-management duties that shippers of corrosive and water-sensitive chemicals must constantly face.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Titanium Trichloride Market Trend

Grid Storage R&D Expands Titanium Applications

The use of energy storage is increasing and broadening the ancillary need of Ti(III) salts. The IEA reported that in 2023, the world added 42 GW of battery storage, nearly twice the amount added in the prior year. As utilities and developers expand storage infrastructure, they also consider chemistries appropriate to long-duration operation and grid support, beyond mainstream lithium-ion systems.

This atmosphere maintains flow-battery research and development, such as titanium-based redox couples. Recent literature discusses titanium flow-battery systems constructed based on Ti redox chemistry (such as TiO 2 +/Ti 3 +), in which the stability of the electrolyte and kinetics are the main constraints. Titanium trichloride, which directly provides Ti(III) in acidic chloride environments, thus remains useful as a laboratory and pilot precursor in new storage chemistries, although volumes may be small relative to catalyst applications.

Global Titanium Trichloride Market Opportunity

Strong Titanium Feedstock Base Secures Supply

The upstream titanium feedstock scale presents a concrete chance to enhance the dependability of the titanium trichloride supply. The production chains of TiCl3 are based on the mineral concentrates of titanium and chloride processing; therefore, high, consistent output of the concentrate makes the long-term contracts of raw materials and purification economics more viable, especially in the case of catalyst-grade specifications where contamination is a major concern.

The current concentration of that scale is shown in government mineral statistics. According to the U.S. Geological Survey, in 2024, China is the largest producer and consumer of titanium mineral concentrates, producing about one-third of the world ilmenite. To TiCl 3 suppliers, this concentration enables integrated feedstock solutions and more predictable raw-material throughput, which lessens procurement interruptions to customers who rely on stable catalyst performance and dependable deliveries.

Global Titanium Trichloride Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

Asia‑Pacific holds the leading position, with a 45% share of global demand (regional split provided for this study). The region’s strength comes from its dense concentration of polymer manufacturing and broader chemical processing capacity, so suppliers of titanium trichloride benefit from shorter customer lead times, frequent replenishment cycles, and established supplier qualification ecosystems around catalysts and specialty reagents.

Upstream raw‑material availability also supports this leadership. The U.S. Geological Survey notes that China remains the leading producer and consumer of titanium mineral concentrates in 2024, accounting for approximately one‑third of global ilmenite production. With both downstream polymer/value‑added manufacturing and a major upstream titanium feedstock base nearby, Asia‑Pacific continues to anchor procurement, storage, and distribution networks for titanium trichloride across multiple industries.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Titanium Trichloride Market Segmentation Analysis

By Grade

- Catalyst Grade

- Industrial Grade

- Reagent Grade

- Custom/High-Purity Grade

The segment has the highest share around the Grade segment, where Catalyst Grade grabs a 50% market share. This dominance aligns with how TiCl3 is consumed: catalyst‑grade material is selected when polymer producers need tight control over catalyst activity, stereospecificity, and trace impurities in Ziegler-Natta catalyst systems used for olefin polymerization.

Technical or laboratory grades still move in meaningful volumes, but they are usually pulled by smaller, batch‑type applications such as R&D, pilot trials, or reagent use in fine‑chemical synthesis—use cases that tolerate broader specification ranges and fluctuate with project cycles. In contrast, polymer plants value predictable catalyst behavior, so buyers qualify fewer suppliers and lock specifications for longer periods, reinforcing repeat demand for catalyst‑grade TiCl3.

By End-User

- Polymer & Plastics Industry

- Chemical & Petrochemical Industry

- Pharmaceutical & Fine Chemicals

- Academic & Research Institutions

- Universities & Research Labs

The segment has the highest share around the End‑User segment, where the Polymer & Plastics Industry grabs 55% of the market. This is consistent with the chemical’s core role in olefin polymerization: titanium halides (including TiCl3) sit in the toolkit of Ziegler-Natta catalysts that enable large‑scale production of polyethylene and polypropylene.

The scale of the plastics value chain makes this end‑use hard to displace. UNCTAD reports global plastic production at 436 million metric tons in 2023 and plastic trade above US$1.1 trillion (around 5% of global merchandise trade). High, continuous resin output pushes producers to prioritize stable catalyst inputs and reliable deliveries, keeping polymer and plastics applications as the anchor demand pool for titanium trichloride.

Market Players in Global Titanium Trichloride Market

These market players maintain a significant presence in the Global titanium trichloride market sector and contribute to its ongoing evolution.

- TOHO Titanium Co. Ltd.

- Osaka Titanium Technologies Co. Ltd.

- Cangzhou Heli Chemical Co. Ltd.

- Tronox Holdings plc

- The Chemours Company

- KRONOS Worldwide Inc.

- Venator Materials PLC

- Ishihara Sangyo Kaisha Ltd. (ISK)

- Xiantao Zhongxing Electronic Materials Co. Ltd.

- Lomon Billions Group

- Henan Longxing Titanium Co. Ltd.

- Ansteel Group (Pangang Group Vanadium & Titanium)

- CITIC Titanium Industry Co. Ltd.

- The Kerala Minerals & Metals Ltd. (KMML)

- Merck KGaA

Competitive Landscape

The global titanium trichloride market is set for steady expansion through 2026–32, supported by stable polyolefin production and consistent catalyst demand. Growth remains closely tied to its core role in Ziegler–Natta catalyst systems, which anchor consumption in large-scale polyethylene and polypropylene manufacturing. As a result, the Polymer & Plastics industry continues to dominate end use, while Catalyst Grade remains the leading segment due to strict quality and performance requirements in polymer production. Asia-Pacific leads global demand, driven by its strong concentration of polymer manufacturing capacity and access to titanium feedstock. However, the corrosive and water-reactive nature of titanium trichloride increases compliance, packaging, and logistics costs, making operational discipline critical across the supply chain. Although emerging uses such as titanium-based flow battery research provide incremental opportunities, mainstream catalyst applications will remain the primary growth engine over the forecast period

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Global Titanium Trichoride Market Policies, Regulations, and Standards

4. Global Titanium Trichoride Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Global Titanium Trichoride Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Grade

5.2.1.1. Catalyst Grade- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Industrial Grade- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Reagent Grade- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Custom/High-Purity Grade- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Form

5.2.2.1. Solid- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Aqueous/Acidic Solution- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Solvent Complex- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Catalyst Component- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Application

5.2.3.1. Polyolefin Production- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Organic Synthesis- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Inorganic Chemical Synthesis- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Research & Development- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By End-User

5.2.4.1. Polymer & Plastics Industry- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Chemical & Petrochemical Industry- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Pharmaceutical & Fine Chemicals- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Academic & Research Institutions- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Universities & Research Labs- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Direct- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Chemical Distributors- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lab Catalog/E-commerce- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. North America

5.2.6.2. South America

5.2.6.3. Europe

5.2.6.4. Middle East & Africa

5.2.6.5. Asia Pacific

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. North America Titanium Trichoride Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Grade- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Form- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End-User- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Country

6.2.6.1. U.S.

6.2.6.2. Canada

6.2.6.3. Mexico

6.2.6.4. Rest of North America

6.3. U.S. Titanium Trichoride Market Statistics, 2022-2032F

6.3.1.Market Size & Growth Outlook

6.3.1.1. By Revenues in USD Million

6.3.2.Market Segmentation & Growth Outlook

6.3.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

6.3.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

6.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

6.3.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

6.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.4. Canada Titanium Trichoride Market Statistics, 2022-2032F

6.4.1.Market Size & Growth Outlook

6.4.1.1. By Revenues in USD Million

6.4.2.Market Segmentation & Growth Outlook

6.4.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

6.4.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

6.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

6.4.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

6.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.5. Mexico Titanium Trichoride Market Statistics, 2022-2032F

6.5.1.Market Size & Growth Outlook

6.5.1.1. By Revenues in USD Million

6.5.2.Market Segmentation & Growth Outlook

6.5.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

6.5.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

6.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

6.5.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

6.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. South America Titanium Trichoride Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Grade- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Form- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End-User- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Country

7.2.6.1. Brazil

7.2.6.2. Chile

7.2.6.3. Rest of South America

7.3. Brazil Titanium Trichoride Market Statistics, 2022-2032F

7.3.1.Market Size & Growth Outlook

7.3.1.1. By Revenues in USD Million

7.3.2.Market Segmentation & Growth Outlook

7.3.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

7.3.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

7.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

7.3.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

7.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.4. Chile Titanium Trichoride Market Statistics, 2022-2032F

7.4.1.Market Size & Growth Outlook

7.4.1.1. By Revenues in USD Million

7.4.2.Market Segmentation & Growth Outlook

7.4.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

7.4.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

7.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

7.4.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

7.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Europe Titanium Trichoride Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Grade- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Form- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By End-User- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Country

8.2.6.1. Germany

8.2.6.2. France

8.2.6.3. UK

8.2.6.4. Italy

8.2.6.5. Rest of Europe

8.3. Germany Titanium Trichoride Market Statistics, 2022-2032F

8.3.1.Market Size & Growth Outlook

8.3.1.1. By Revenues in USD Million

8.3.2.Market Segmentation & Growth Outlook

8.3.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

8.3.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

8.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.3.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

8.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.4. France Titanium Trichoride Market Statistics, 2022-2032F

8.4.1.Market Size & Growth Outlook

8.4.1.1. By Revenues in USD Million

8.4.2.Market Segmentation & Growth Outlook

8.4.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

8.4.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

8.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.4.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

8.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.5. UK Titanium Trichoride Market Statistics, 2022-2032F

8.5.1.Market Size & Growth Outlook

8.5.1.1. By Revenues in USD Million

8.5.2.Market Segmentation & Growth Outlook

8.5.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

8.5.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

8.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.5.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

8.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.6. Italy Titanium Trichoride Market Statistics, 2022-2032F

8.6.1.Market Size & Growth Outlook

8.6.1.1. By Revenues in USD Million

8.6.2.Market Segmentation & Growth Outlook

8.6.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

8.6.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

8.6.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.6.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

8.6.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Middle East & Africa Titanium Trichoride Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Grade- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Form- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By End-User- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By Country

9.2.6.1. Turkey

9.2.6.2. GCC Countries

9.2.6.3. Africa

9.2.6.4. Rest of Middle East & Africa

9.3. Turkey Titanium Trichoride Market Statistics, 2022-2032F

9.3.1.Market Size & Growth Outlook

9.3.1.1. By Revenues in USD Million

9.3.2.Market Segmentation & Growth Outlook

9.3.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

9.3.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

9.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9.3.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

9.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.4. GCC Countries Titanium Trichoride Market Statistics, 2022-2032F

9.4.1.Market Size & Growth Outlook

9.4.1.1. By Revenues in USD Million

9.4.2.Market Segmentation & Growth Outlook

9.4.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

9.4.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

9.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9.4.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

9.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.5. Africa Titanium Trichoride Market Statistics, 2022-2032F

9.5.1.Market Size & Growth Outlook

9.5.1.1. By Revenues in USD Million

9.5.2.Market Segmentation & Growth Outlook

9.5.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

9.5.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

9.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9.5.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

9.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Asia Pacific Titanium Trichoride Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.2.6. By Country

10.2.6.1. China

10.2.6.2. Japan

10.2.6.3. South Korea

10.2.6.4. Southeast Asia

10.2.6.5. India

10.2.6.6. Rest of Asia Pacific

10.3. China Titanium Trichoride Market Statistics, 2022-2032F

10.3.1. Market Size & Growth Outlook

10.3.1.1. By Revenues in USD Million

10.3.2. Market Segmentation & Growth Outlook

10.3.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.3.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.3.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.4. Japan Titanium Trichoride Market Statistics, 2022-2032F

10.4.1. Market Size & Growth Outlook

10.4.1.1. By Revenues in USD Million

10.4.2. Market Segmentation & Growth Outlook

10.4.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.4.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.4.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.5. South Korea Titanium Trichoride Market Statistics, 2022-2032F

10.5.1. Market Size & Growth Outlook

10.5.1.1. By Revenues in USD Million

10.5.2. Market Segmentation & Growth Outlook

10.5.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.5.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.5.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.6. Southeast Asia Titanium Trichoride Market Statistics, 2022-2032F

10.6.1. Market Size & Growth Outlook

10.6.1.1. By Revenues in USD Million

10.6.2. Market Segmentation & Growth Outlook

10.6.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.6.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.6.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.6.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.6.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10.7. India Titanium Trichoride Market Statistics, 2022-2032F

10.7.1. Market Size & Growth Outlook

10.7.1.1. By Revenues in USD Million

10.7.2. Market Segmentation & Growth Outlook

10.7.2.1. By Grade- Market Insights and Forecast 2022-2032, USD Million

10.7.2.2. By Form- Market Insights and Forecast 2022-2032, USD Million

10.7.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.7.2.4. By End-User- Market Insights and Forecast 2022-2032, USD Million

10.7.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Tronox Holdings plc

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. The Chemours Company

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. KRONOS Worldwide Inc.

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Venator Materials PLC

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Ishihara Sangyo Kaisha Ltd. (ISK)

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. TOHO Titanium Co. Ltd.

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Osaka Titanium Technologies Co. Ltd.

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Cangzhou Heli Chemical Co. Ltd.

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Xiantao Zhongxing Electronic Materials Co. Ltd.

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Lomon Billions Group

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

11.1.11. Henan Longxing Titanium Co. Ltd.

11.1.11.1.Business Description

11.1.11.2.Product Portfolio

11.1.11.3.Collaborations & Alliances

11.1.11.4.Recent Developments

11.1.11.5.Financial Details

11.1.11.6.Others

11.1.12. Ansteel Group (Pangang Group Vanadium & Titanium)

11.1.12.1.Business Description

11.1.12.2.Product Portfolio

11.1.12.3.Collaborations & Alliances

11.1.12.4.Recent Developments

11.1.12.5.Financial Details

11.1.12.6.Others

11.1.13. CITIC Titanium Industry Co. Ltd.

11.1.13.1.Business Description

11.1.13.2.Product Portfolio

11.1.13.3.Collaborations & Alliances

11.1.13.4.Recent Developments

11.1.13.5.Financial Details

11.1.13.6.Others

11.1.14. The Kerala Minerals & Metals Ltd. (KMML)

11.1.14.1.Business Description

11.1.14.2.Product Portfolio

11.1.14.3.Collaborations & Alliances

11.1.14.4.Recent Developments

11.1.14.5.Financial Details

11.1.14.6.Others

11.1.15. Merck KGaA

11.1.15.1.Business Description

11.1.15.2.Product Portfolio

11.1.15.3.Collaborations & Alliances

11.1.15.4.Recent Developments

11.1.15.5.Financial Details

11.1.15.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Grade |

|

| By Form |

|

| By Application |

|

| By End-User |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.