Poland 155mm Artillery Shells Market Report: Trends, Growth and Forecast (2026-2032)

By Shell Type (High-Explosive (HE\HE-FRAG) Shell, Smoke Shell, Illumination Shell, Training/Practice Shell, Other Special-Purpose Shell), By Guidance (Unguided, Precision-Guided), By Range Class (Standard Range, Extended Range, Assisted Range (Base Bleed, Rocket-Assisted (RAP))), By Operational Use (Training Consumption, Routine Peacetime Stockpile Replenishment, Active Conflict Replenishment\Urgent Operational Demand, Strategic Reserve\Surge Inventory Build), By Artillery Platform Type (Towed Howitzers, Self-Propelled Howitzers, Truck-Mounted Howitzers) ... Read more

|

Major Players

|

Poland 155mm Artillery Shells Market Statistics and Insights, 2026

- Market Size Statistics

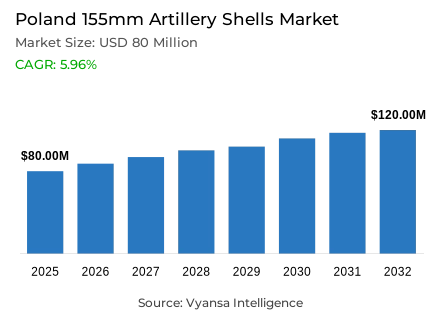

- 155mm artillery shells market size in Poland was estimated at USD 80 million in 2025.

- The market size is expected to grow to USD 120 million by 2032.

- Market to register a CAGR of around 5.96% during 2026-32.

- Shell Type Shares

- High-explosive (he/he-frag) shell grabbed market share of 70%.

- Competition

- 155mm artillery shells in Poland is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 75% of the market share.

- BAE Systems, Nexter (KNDS), Elbit Systems, PGZ (Polska Grupa Zbrojeniowa), Mesko etc., are few of the top companies.

- Guidance

- Unguided grabbed 85% of the market.

Poland 155mm Artillery Shells Market Outlook

The Poland 155mm Artillery Shells Market is estimated at USD 80 million in 2025 and is projected to reach USD 120 million by 2032, registering a CAGR of approximately 5.96% during 2026-32. This steady growth trajectory is underpinned by Poland's 2026 state budget allocating over PLN 200 billion to national defence - representing 4.81% of GDP - ensuring consistent procurement volumes and reinforcing demand signals across the supply chain for the foreseeable future.

A defining structural driver is the rapid acceleration of domestic manufacturing capability. Backed by a landmark PGZ–BAE Systems technology transfer partnership, Poland is on track to produce approximately 130,000 shells annually within two years. The government's allocation of PLN 1.3 billion for Dezamet facility expansion further signals a long-term ambition toward sovereign capability, potentially positioning Poland as a net exporter should surplus capacity emerge.

Within the product breakdown, High-Explosive (HE/HE-FRAG) rounds dominate - commanding approximately 70% of total share - owing to their role as the standard workhorse for indirect fire support across NATO artillery platforms, including the AHS Krab howitzer. The demand for 155mm artillery shells in this configuration is driven by high-volume procurement priorities and contingency stockpiling objectives. Unguided rounds account for around 85% of the guidance segmentation, reflecting Poland's "scale first" procurement philosophy that favours standardised, high-throughput configurations over precision-guided alternatives.

On the supply side, propellants and explosives remain the most persistent upstream bottleneck, despite EU-level interventions under ASAP channelling EUR 248 million into powder and EUR 124 million into explosives capacity. While pan-European funding mechanisms - including EUR 310 million under EDIRPA - create meaningful partnership and consortium opportunities for Polish producers, energetic material constraints continue to weigh on delivery timelines, representing a key risk to otherwise robust demand fundamentals shaping this sector's growth through 2032.

Poland 155mm Artillery Shells Market Growth DriverSurging Defence Expenditure Anchoring Sustained Ammunition Demand

Poland's 2026 state budget allocates over PLN 200 billion to national defence, representing 4.81% of GDP, underscoring an unambiguous commitment to large-scale army modernisation and broader security system reinforcement. This unprecedented level of fiscal commitment ensures that ammunition procurement and stock replenishment remain firmly embedded within strategic planning priorities, particularly for NATO-standard artillery systems where 155 mm rounds are considered central to operational readiness. End users across Poland's artillery forces benefit directly from this sustained funding environment, which provides consistent demand signals to both domestic producers and international integrators operating within the supply chain.

The multi-year nature of ongoing capability upgrades further solidifies demand by prioritising the steady availability of standard rounds for training cycles and contingency stockpiling-not merely platform acquisition. This structural "budget certainty" functions as a direct demand anchor, assuring producers and system integrators of predictable procurement volumes over the medium term. For end users operating Poland's howitzer fleets, the policy framework translates into a more reliable supply pipeline, reinforcing readiness levels and reducing procurement uncertainty at the operational level.

Poland 155mm Artillery Shells Market ChallengePropellant and Explosives Scarcity Constraining Supply Chain Scalability

Although final assembly capacity has grown substantially throughout Europe, propellants and explosives have become the hardest to manage bottlenecks in the 155mm ammunition supply chain. These energetic materials have been explicitly listed by the European Commission as critical constraints, with EUR 248 million of powder capacity and EUR 124 million of explosives capacity being allocated under the Act in Support of Ammunition Production (ASAP), with increases of +10000 tonnes of powder and +4300 tonnes of explosives. However, the rate of capacity addition in these upstream segments remains below the rate of demand growth, which results in structural imbalances that burden delivery schedules across the wider production ecosystem.

To suppliers of Polish end users, this bottleneck is reflected in longer lead times and stricter qualification criteria on energetic input materials-problems that remain even when downstream metalworking and shell-filling capabilities are enhanced. The compliance cost of managing, transporting, and certifying these hazardous materials further complicates and increases the cost of operations at all levels of the 155mm supply chain. Controlling the dynamic material acquisition is thus a long-term and systemic issue of concern to the producers who want to fulfil delivery obligations to the armed forces of Poland in the prevailing demand environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland 155mm Artillery Shells Market TrendTechnology Transfer and Domestic Industrialisation Reshaping Production Landscape

One of the trends that are transforming the Poland 155 mm artillery shells market is the fast pace at which the domestic manufacturing capacity is being accelerated by organized technology transfer deals. With a historic agreement between Polska Grupa Zbrojeniowa (PGZ) and BAE Systems, Poland is set to achieve about 130,000 shells annually in two years, which is a massive increase in national production of 155mm ammunition. This drive towards industrialisation is supported by planned capital investment, whereby the Polish government has invested PLN 1.3 billion in the expansion and modernisation of the Dezamet production plant- a move that is a clear indication that the government has long term plans of becoming a sovereign manufacturer.

This trend has serious implications on the end users and the market structure at large. Through the creation of strong domestic production, Poland gradually becomes less reliant on foreign supply chains, improving the flexibility of procurement and operational stability. The Dezamet investment in specific positions places Poland not only as a net importer but as a potential net exporter of 155mm ammunition, in the event of excess capacity. The move towards native production, which has been accelerated by high-level technology alliances, is a structural re-alignment of the supply base that will outline the competitive and strategic lines of the market in the next decade.

Poland 155mm Artillery Shells Market OpportunityEU-Backed Collaborative Frameworks Unlocking Market Entry and Expansion Pathways

The coordinated industrial scale-up of the European Union is a concrete and organized complex of opportunities of Polish companies that are located in or near the 155 mm ammunition ecosystem. Within the framework of the ASAP mechanism, the European Commission has provided EUR 500 million in support of increasing EU-wide ammunition capacity to 2 million shells per year by end-2025, with 155 mm-specific capacity already reaching 1 million shells per year by January 2024. These capacity goals, supported by direct funding and solid schedules, create tangible procurement and collaboration prospects that Polish manufacturers and integrators are poised to seize with consortium membership, tooling modernization, and shared order platforms.

The opportunity landscape is further enhanced by the financial architecture underpinning this expansion. It has chosen 31 projects with a total EU and Norwegian funding of EUR 513 million, with an overall supply-chain investment of about EUR 1.4 billion. Simultaneously, EUR 310 million under the European Defence Industry Reinforcement through Common Procurement Act (EDIRPA) incentives aligned the procurement across the member states, allowing Polish end users to be part of bigger and cost-effective multi-country orders. Combined, these mechanisms can substantially reduce the entry barrier to Polish industrial involvement in pan-European 155mm production and procurement programmes.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland 155mm Artillery Shells Market Segmentation Analysis

By Shell Type

- High-Explosive (HE\HE-FRAG) Shell

- Smoke Shell

- Illumination Shell

- Training/Practice Shell

- Other Special-Purpose Shell

Within the Poland 155mm artillery shells market, the Shell Type segmentation is firmly led by High-Explosive (HE/HE-FRAG) Shell, which account for approximately 70% of total market share. This commanding position reflects the round's status as the standard workhorse of indirect fire support-deployed extensively for target suppression, neutralisation, and engagement of general target sets across diverse operational scenarios. The HE/HE-FRAG configuration offers an optimal balance of destructive effectiveness, logistical simplicity, and interoperability across NATO artillery platforms, making it the default procurement choice when end users prioritise volume, standardisation, and planning efficiency over mission-specific specialisation.

Other shell types-including smoke, illumination, training, and specialty variants-retain meaningful roles within the Polish artillery inventory but are typically procured in more targeted quantities driven by specific mission requirements rather than bulk stockpiling objectives. Poland's official communications reinforce the primacy of HE/HE-FRAG rounds by identifying 155 mm ammunition as the backbone of NATO artillery doctrine, with particular emphasis on systems such as the AHS Krab self-propelled howitzer. As Poland accelerates its artillery modernisation programme, the HE/HE-FRAG segment is expected to sustain its dominant share through continued demand for high-volume procurement and contingency stock maintenance.

By Guidance

- Unguided

- Precision-Guided

The Guidance segmentation of the Poland 155mm artillery shells market is decisively led by unguided rounds, which account for approximately 85% of total market share. This substantial dominance is driven by the fundamental role unguided ammunition plays in sustaining high-volume training throughput and large-scale stockpile accumulation-both of which are priorities firmly embedded in Poland's current defence posture. Unguided rounds support continuous and high-tempo firing operations while ensuring standardisation across diverse artillery units, enabling end users to maintain consistent readiness without the logistical complexity associated with precision-guided munition inventories.

Guided rounds, while strategically valuable, are predominantly reserved for niche engagement scenarios involving high-value or time-sensitive targets where precision justifies the significantly higher per-unit cost. Poland's official policy direction strongly reinforces the "scale first" procurement philosophy: government communications emphasise rapidly increasing 155 mm production volumes through advanced technology and major facility investment, a framework that inherently favours high-throughput, standardised unguided configurations. As domestic production capacity scales at facilities such as Dezamet and procurement volumes grow in line with defence budget commitments, unguided rounds are expected to sustain their leading position across the market's guidance segmentation.

List of Companies Covered in Poland 155mm Artillery Shells Market

The companies listed below are highly influential in the Poland 155mm artillery shells market, with a significant market share and a strong impact on industry developments.

- BAE Systems

- Nexter (KNDS)

- Elbit Systems

- PGZ (Polska Grupa Zbrojeniowa)

- Mesko

- Nitro-Chem

- Rheinmetall

- Nammo

- General Dynamics Ordnance & Tactical Systems

Market News & Updates

- PGZ Group, 2025:

Dezamet (PGZ Group) announced that it selected BAE Systems as a strategic partner to support technology access/transfer and industrial scaling for NATO-standard 155mm artillery ammunition production in Poland—an “economy of war” move aimed at materially increasing domestic output and strengthening security of supply for Polish requirements (and potentially allied demand) by reducing dependence on external sources and accelerating local industrial modernization across the 155mm value chain.

- MESKO, 2025:

MESKO stated that on 29 October 2025 it launched the build-out of production infrastructure at its Kraśnik plant specifically to manufacture “key” 155mm artillery ammunition, positioning the site as a strategic capacity expansion within PGZ’s ammunition ecosystem; for the Poland 155mm shells market, this is a direct step-change toward higher sustained throughput, shorter delivery lead times, and improved resilience (multi-site national production) that supports long-horizon contracting and reduces single-point industrial risk.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Poland 155mm Artillery Shells Market Policies, Regulations, and Standards

- Poland 155mm Artillery Shells Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Poland 155mm Artillery Shells Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Shell Type

- High-Explosive (HE\HE-FRAG) Shell- Market Insights and Forecast 2022-2032, USD Million

- Smoke Shell- Market Insights and Forecast 2022-2032, USD Million

- Illumination Shell- Market Insights and Forecast 2022-2032, USD Million

- Training/Practice Shell- Market Insights and Forecast 2022-2032, USD Million

- Other Special-Purpose Shell- Market Insights and Forecast 2022-2032, USD Million

- By Guidance

- Unguided - Market Insights and Forecast 2022-2032, USD Million

- Precision-Guided - Market Insights and Forecast 2022-2032, USD Million

- By Range Class

- Standard Range - Market Insights and Forecast 2022-2032, USD Million

- Extended Range - Market Insights and Forecast 2022-2032, USD Million

- Assisted Range- Market Insights and Forecast 2022-2032, USD Million

- Base Bleed- Market Insights and Forecast 2022-2032, USD Million

- Rocket-Assisted (RAP)- Market Insights and Forecast 2022-2032, USD Million

- By Operational Use

- Training Consumption- Market Insights and Forecast 2022-2032, USD Million

- Routine Peacetime Stockpile Replenishment- Market Insights and Forecast 2022-2032, USD Million

- Active Conflict Replenishment\Urgent Operational Demand- Market Insights and Forecast 2022-2032, USD Million

- Strategic Reserve\Surge Inventory Build- Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type

- Towed Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Self-Propelled Howitzers- Market Insights and Forecast 2022-2032, USD Million

- Truck-Mounted Howitzers- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Shell Type

- Market Size & Growth Outlook

- Poland High-Explosive (HE\HE-FRAG) Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Smoke Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Illumination Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Poland Training/Practice Shells Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Guidance- Market Insights and Forecast 2022-2032, USD Million

- By Range Class - Market Insights and Forecast 2022-2032, USD Million

- By Operational Use - Market Insights and Forecast 2022-2032, USD Million

- By Artillery Platform Type - Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- PGZ (Polska Grupa Zbrojeniowa)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dezamet

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mesko

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nitro-Chem

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nammo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nexter (KNDS)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elbit Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Dynamics Ordnance & Tactical Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PGZ (Polska Grupa Zbrojeniowa)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Shell Type |

|

| By Guidance |

|

| By Range Class |

|

| By Operational Use |

|

| By Artillery Platform Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.