Global Photoresists & Advanced Lithography Materials Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Positive Photoresists, Negative Photoresists, Dry Film Photoresists), By Application (Semiconductor Manufacturing, Printed Circuit Boards, Microelectronics), By Region (North America, Latin America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Photoresists & Advanced Lithography Materials Market Statistics and Insights, 2026

- Market Size Statistics

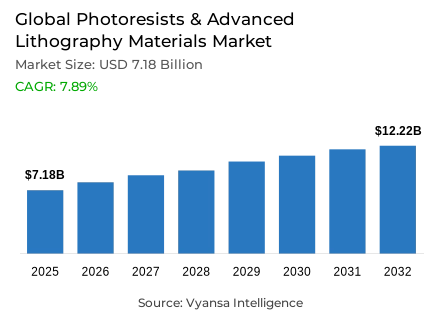

- Global photoresists & advanced lithography materials market is estimated at USD 7.18 billion in 2025.

- The market size is expected to grow to USD 12.22 billion by 2032.

- Market to register a CAGR of around 7.89% during 2026-32.

- Type Shares

- Positive photoresists grabbed market share of 50%.

- Competition

- Global photoresists & advanced lithography materials market is currently being catered to by more than 15 companies.

- Top 5 companies acquired around 65% of the market share.

- Shin-Etsu Chemical; Allresist; Merck KGaA; DuPont de Nemours; FUJIFILM Holdings etc., are few of the top companies.

- Application

- Semiconductor manufacturing grabbed 60% of the market.

- Region

- Asia Pacific leads with a 70% share of the global market.

Global Photoresists & Advanced Lithography Materials Market Outlook

The photoresists and advanced lithography materials market is projected to grow to USD 12.22 billion in 2032, with a CAGR of about 7.89% between 2026 and 2032, with a global market of USD 7.18 billion in 2025. This strong growth trend is closely linked to the continued expansion of semiconductor manufacturing capacity across the globe, driven by the growing needs of artificial-intelligence workloads and high-performance computing. The world semiconductor revenues were USD 728 billion in 2025 and are expected to reach USD 800 billion in 2026, thus motivating manufacturers to invest heavily in new and increased fabrication plants.

In 2025, the semiconductor firms invested close to USD 185 billion in capital investments, which increased the manufacturing capacity across the world by about 7%. The consumption of photoresist is directly proportional to the introduction of every new fabrication line, as lithography is reused in gate patterning, interconnect formation, contact layering, and advanced packaging. The level of demand is significantly higher at advanced nodes, where artificial-intelligence accelerators and data-centre processors require numerous critical lithography layers with nanometre-scale precision. As a result, the consumption of photoresist increases in direct proportion to capacity additions across all major semiconductor regions.

In terms of product segmentation, positive photoresists make up about 50% of the overall market demand. Their leading role is based on decades of process integration, consistent pattern transfer, and proven applicability to high-volume manufacturing, including advanced EUV lithography. The most dominant application segment is semiconductor manufacturing, which consumes almost 60% of the total consumption, since photoresists are essential in both front-end and back-end fabrication processes. The long life cycles of fabrication plants ensure that there is a constant, repeated demand.

The Asia Pacific region holds about 70% of the market share, which has been maintained by its concentration of high-technology semiconductor fabrication plants in Taiwan, South Korea, Japan, China, and emerging projects in India. Despite the growing momentum of new investments in North America and Europe, the established manufacturing base in the Asia Pacific region means that it will continue to be the key driver of demand of photoresists and advanced lithography materials until 2032.

Global Photoresists & Advanced Lithography Materials Market Growth Driver

Expanding AI Chip Production Accelerates Fabrication Capacity Investments

The global market of photoresists and advanced lithography materials is being driven by unparalleled growth of semiconductor fabrication capacity to serve artificial intelligence workloads. According to World Semiconductor Trade Statistics data, the global semiconductor market at around USD 772 billion in 2025 and is projected to be close to USD 1 trillion in 2026, with AI accelerators contributing almost 20% of all semiconductor sales in 2024 and increasing further in 2025. To meet this demand, semiconductor manufacturers invested about USD 185 billion in capital spending in 2025, increasing global manufacturing capacity by about 7%, and the United States semiconductor supply chain alone has received over USD 630 billion in private investment since 2020 under government incentive programs.

This capacity build-out scale directly proportions the consumption of photoresist, with each wafer needing several lithography layers to pattern gates, define interconnects, form contacts, and package it. Highly specialised photoresist formulations that can achieve nanometre-scale precision are used in advanced node manufacturing of AI accelerators, data-centre processors and high-bandwidth memory. With the increase in fabrication capacity around the world, the demand of photoresist increases in the same proportion in all regions of semiconductor manufacturing.

Global Photoresists & Advanced Lithography Materials Market Challenge

Structural Raw Material Dependencies Constrain Rapid Supply Scaling

Although the market of photoresists and advanced lithography materials is highly demanded, the supply of materials is constrained globally, which does not allow accelerating production. OECD semiconductor supply-chain evaluations show that more than half of the critical chemical supply chains do not have enough domestic capacity to satisfy the projected 2030 demand, with ultra-high-purity hydrogen fluoride and other important inputs being highly concentrated in Asia. The construction of advanced-node fabrication plants costs USD 10-20 billion per site, has long construction times, and needs access to highly specialised talent, which introduces structural rigidity in the materials ecosystem.

Vulnerability is further aggravated by geographic concentration of precursor materials. OECD materials analysis points out that over 70% of the world supply of tungsten, germanium and cobalt is dominated by individual nations, which puts the production of photoresist at risk of geopolitical and trade interference. These limitations are reflected in longer qualification cycles and lead times, especially with extreme ultraviolet photoresists, where the manufacturing is still concentrated in the hands of a few certified suppliers around the globe.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Photoresists & Advanced Lithography Materials Market Trend

Metal Oxide Photoresists Redefine Advanced Lithography Performance

The technological development in the international market of photoresists and high-technology lithography materials focuses on metal-oxide photoresists that allow advanced-node scaling. A study by the United States National Institutes of Health in 2024 has shown that photoresists based on tin-oxide, hafnium-oxide and zirconium-oxide absorb extreme ultraviolet radiation two to three times better than traditional polymer resists. This enhanced absorption increases photon utilisation, minimises stochastic defects, and increases etch resistance, directly overcoming pattern-fidelity issues at sub-3nm nodes.

To complement material innovation, high-numerical-aperture EUV lithography systems are transforming process requirements. According to SPIE technical documentation, 0.55-NA EUV systems have 1.7 times smaller features and enhance local critical-dimension uniformity by approximately 40% over 0.33-NA systems. Such systems require thinner coatings, greater sensitivity, and lower line-edge roughness, and thus the transition to metal-oxide and multi-trigger resist platforms is hastened as the traditional chemically amplified resists approach fundamental performance limits.

Global Photoresists & Advanced Lithography Materials Market Opportunity

Advanced Packaging Expands Photoresist Demand Beyond Front End Processes

Advanced packaging architectures are one of the major growth opportunities in the global market of photoresists and advanced lithography materials. Governments are starting to see packaging as strategic infrastructure; under the United States CHIPS and Science Act, USD 52.7 billion is being spent on semiconductor manufacturing and research, and as much as USD 1.6 billion of that is specifically on packaging-technology development. These projects indicate the increased significance of backend integration of artificial-intelligence accelerators and high-performance computing devices.

Specialised photoresists are needed in advanced packaging processes to patterning of thick-film, redistribution layers of fine-line, through-silicon vias, and hybrid bonding. The HBM4 standard of JEDEC, announced in April 2025, highlights the necessity of ultra-high-density interconnects with sub-10 m pitches, which in turn puts pressure on high-resolution, high-alignment-precision photoresists. With the increasing global adoption of chiplet integration and hybrid-bonding, backend lithography is becoming a structurally significant source of incremental photoresist usage.

Global Photoresists & Advanced Lithography Materials Market Regional Analysis

By Region

- North America

- Latin America

- Europe

- Middle East & Africa

- Asia Pacific

Asia Pacific commands roughly 70% of the Global photoresists & advanced lithography materials market, reflecting its concentration of advanced semiconductor fabrication capacity. The region includes Taiwan’s leading foundry ecosystem, South Korea’s memory manufacturing leadership, Japan’s specialty materials and device production, China’s large scale mature node base, and India’s emerging government supported semiconductor initiatives. This concentration drives proportional demand for advanced photoresists required for sub 5 nm logic and high volume memory manufacturing.

India is becoming an increasingly relevant contributor as government backed semiconductor projects expand domestic capacity. The national Semiconductor Mission has approved multiple large scale investments across several states, supporting logic fabs and assembly test manufacturing facilities. Combined with capacity expansion in North America under the CHIPS Act and parallel European programs, Asia Pacific’s entrenched fabrication leadership ensures it will remain the primary consumption hub for advanced lithography materials through the forecast horizon.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Photoresists & Advanced Lithography Materials Market Segmentation Analysis

By Type

- Positive Photoresists

- Negative Photoresists

- Dry Film Photoresists

Within the Global photoresists & advanced lithography materials market, positive photoresists account for approximately 50% of total demand, reflecting decades of established process integration. Positive tone resists dissolve in exposed regions, enabling direct and highly predictable pattern transfer across optical and EUV lithography platforms. Their proven compatibility with high volume manufacturing makes them the preferred choice for logic, memory, and foundry applications at both mature and advanced nodes.

This entrenched position is reinforced by extensive historical data, qualification records, and fab certification processes that reduce risk during technology transitions. In EUV lithography, positive tone formulations deliver superior photon sensitivity and comparatively lower stochastic defect rates than negative alternatives at 13.5 nm wavelengths. While metal oxide platforms are gaining traction, semiconductor manufacturers continue to favor incremental innovation within positive tone chemistries, sustaining their leadership across global fabrication capacity.

By Application

- Semiconductor Manufacturing

- Printed Circuit Boards

- Microelectronics

Semiconductor manufacturing represents around 60% of total consumption in the Global photoresists & advanced lithography materials market, underscoring lithography’s central role in integrated circuit production. Photoresists are used repeatedly across front end and back end processes, including gate definition, interconnect patterning, contact formation, and advanced packaging. This segment spans leading edge logic production, DRAM and 3D NAND memory, analog and mixed signal devices, and specialty semiconductors such as power and RF components.

Demand intensity increases sharply at advanced nodes, where each wafer requires multiple EUV critical layers, significantly raising photoresist usage per unit. Long fab lifecycles of 15-20 years create durable baseline demand aligned with installed capacity. Sustained global requirements for AI accelerators, data center processors, advanced memory architectures, and specialty devices ensure that semiconductor manufacturing remains the dominant and most stable end user segment through the 2026-2032 period.

Market Players in Global Photoresists & Advanced Lithography Materials Market

The companies listed below are highly influential in the Global photoresists & advanced lithography materials market, with a significant market share and a strong impact on industry developments.

- Shin-Etsu Chemical

- Allresist

- Merck KGaA

- DuPont de Nemours

- FUJIFILM Holdings

- JSR Corporation

- Sumitomo Chemical

- Tokyo Ohka Kogyo (TOK)

- Avantor Performance Materials

- micro resist technology (GmbH)

- Brewer Science

- SACHEM, Inc.

- Kayaku Advanced Materials

- Weifang Startech Microelectronic Materials

Market News & Updates

- DuPont de Nemours, 2025:

DuPont launched DuPont™ UV™ 26GNF photoresist, representing the first commercial photoresist to successfully substitute traditional fluorine-containing photoacid generators with a non-fluorine alternative designed to replace per- and polyfluoroalkyl substances (PFAS) in semiconductor manufacturing. This innovation addresses decades-long industry efforts to develop feasible non-PFAS photoresists for deep ultraviolet (DUV) lithography at 248-nanometer wavelengths. The company received recognition from the American Chemical Society, with 13 current and former scientists associated with the innovative photoresist program honored as 2025 Heroes of Chemistry for their contributions to sustainable semiconductor manufacturing solutions.

- Sumitomo Chemical, 2025:

Sumitomo Chemical expanded its photoresist development and quality evaluation facilities at its Osaka Works to strengthen systems for developing and evaluating new photoresists for advanced semiconductor manufacturing processes. The expansion focuses on front-end and back-end processes, specifically targeting immersion argon fluoride (ArF) photoresists and i-line thick film photoresists. New semiconductor lithography devices were scheduled to commence operations sequentially beginning in fiscal year 2025 through the first half of fiscal year 2026, enabling the company to win additional orders from advanced semiconductor manufacturers globally.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Global Photoresists & Advanced Lithography Materials Market Policies, Regulations, and Standards

4. Global Photoresists & Advanced Lithography Materials Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Global Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Type

5.2.1.1. Positive Photoresists- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Negative Photoresists- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Dry Film Photoresists- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Semiconductor Manufacturing- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Printed Circuit Boards- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Microelectronics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Region

5.2.3.1. North America

5.2.3.2. Latin America

5.2.3.3. Europe

5.2.3.4. Middle East & Africa

5.2.3.5. Asia Pacific

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. North America Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Country

6.2.3.1. US

6.2.3.2. Canada

6.2.3.3. Mexico

6.2.3.4. Rest of North America

6.3. US Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

6.3.1.Market Size & Growth Outlook

6.3.1.1. By Revenues in USD Million

6.3.2.Market Segmentation & Growth Outlook

6.3.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

6.3.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

6.4. Canada Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

6.4.1.Market Size & Growth Outlook

6.4.1.1. By Revenues in USD Million

6.4.2.Market Segmentation & Growth Outlook

6.4.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

6.4.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

6.5. Mexico Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

6.5.1.Market Size & Growth Outlook

6.5.1.1. By Revenues in USD Million

6.5.2.Market Segmentation & Growth Outlook

6.5.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

6.5.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

7. Latin America Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Country

7.2.3.1. Brazil

7.2.3.2. Rest of Latin America

7.3. Brazil Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

7.3.1.Market Size & Growth Outlook

7.3.1.1. By Revenues in USD Million

7.3.2.Market Segmentation & Growth Outlook

7.3.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

7.3.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8. Europe Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Country

8.2.3.1. Germany

8.2.3.2. France

8.2.3.3. UK

8.2.3.4. Italy

8.2.3.5. Spain

8.2.3.6. Netherlands

8.2.3.7. Belgium

8.2.3.8. Poland

8.2.3.9. Russia

8.2.3.10. Turkey

8.2.3.11. Rest of Europe

8.3. Germany Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.3.1.Market Size & Growth Outlook

8.3.1.1. By Revenues in USD Million

8.3.2.Market Segmentation & Growth Outlook

8.3.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.3.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.4. France Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.4.1.Market Size & Growth Outlook

8.4.1.1. By Revenues in USD Million

8.4.2.Market Segmentation & Growth Outlook

8.4.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.4.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.5. UK Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.5.1.Market Size & Growth Outlook

8.5.1.1. By Revenues in USD Million

8.5.2.Market Segmentation & Growth Outlook

8.5.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.5.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.6. Italy Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.6.1.Market Size & Growth Outlook

8.6.1.1. By Revenues in USD Million

8.6.2.Market Segmentation & Growth Outlook

8.6.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.6.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.7. Spain Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.7.1.Market Size & Growth Outlook

8.7.1.1. By Revenues in USD Million

8.7.2.Market Segmentation & Growth Outlook

8.7.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.7.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.8. Netherlands Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.8.1.Market Size & Growth Outlook

8.8.1.1. By Revenues in USD Million

8.8.2.Market Segmentation & Growth Outlook

8.8.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.8.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.9. Belgium Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.9.1.Market Size & Growth Outlook

8.9.1.1. By Revenues in USD Million

8.9.2.Market Segmentation & Growth Outlook

8.9.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.9.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.10. Poland Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.10.1. Market Size & Growth Outlook

8.10.1.1. By Revenues in USD Million

8.10.2. Market Segmentation & Growth Outlook

8.10.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.11. Russia Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.11.1. Market Size & Growth Outlook

8.11.1.1. By Revenues in USD Million

8.11.2. Market Segmentation & Growth Outlook

8.11.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.11.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

8.12. Turkey Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

8.12.1. Market Size & Growth Outlook

8.12.1.1. By Revenues in USD Million

8.12.2. Market Segmentation & Growth Outlook

8.12.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

8.12.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

9. Middle East & Africa Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Country

9.2.3.1. Saudi Arabia

9.2.3.2. UAE

9.2.3.3. Rest of Middle East & Africa

9.3. Saudi Arabia Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

9.3.1.Market Size & Growth Outlook

9.3.1.1. By Revenues in USD Million

9.3.2.Market Segmentation & Growth Outlook

9.3.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

9.3.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

9.4. UAE Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

9.4.1.Market Size & Growth Outlook

9.4.1.1. By Revenues in USD Million

9.4.2.Market Segmentation & Growth Outlook

9.4.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

9.4.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10. Asia Pacific Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Country

10.2.3.1. China

10.2.3.2. Japan

10.2.3.3. South Korea

10.2.3.4. India

10.2.3.5. Australia

10.2.3.6. Thailand

10.2.3.7. Rest of Asia Pacific

10.3. China Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.3.1. Market Size & Growth Outlook

10.3.1.1. By Revenues in USD Million

10.3.2. Market Segmentation & Growth Outlook

10.3.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.3.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.4. Japan Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.4.1. Market Size & Growth Outlook

10.4.1.1. By Revenues in USD Million

10.4.2. Market Segmentation & Growth Outlook

10.4.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.4.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.5. South Korea Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.5.1. Market Size & Growth Outlook

10.5.1.1. By Revenues in USD Million

10.5.2. Market Segmentation & Growth Outlook

10.5.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.5.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.6. India Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.6.1. Market Size & Growth Outlook

10.6.1.1. By Revenues in USD Million

10.6.2. Market Segmentation & Growth Outlook

10.6.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.6.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.7. Australia Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.7.1. Market Size & Growth Outlook

10.7.1.1. By Revenues in USD Million

10.7.2. Market Segmentation & Growth Outlook

10.7.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.7.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

10.8. Thailand Photoresists & Advanced Lithography Materials Market Statistics, 2022-2032F

10.8.1. Market Size & Growth Outlook

10.8.1.1. By Revenues in USD Million

10.8.2. Market Segmentation & Growth Outlook

10.8.2.1. By Type- Market Insights and Forecast 2022-2032, USD Million

10.8.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. DuPont de Nemours

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. FUJIFILM Holdings

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. JSR Corporation

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Sumitomo Chemical

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Tokyo Ohka Kogyo (TOK)

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Shin-Etsu Chemical

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Allresist

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Merck KGaA

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Avantor Performance Materials

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. micro resist technology (GmbH)

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

11.1.11. Brewer Science

11.1.11.1.Business Description

11.1.11.2.Product Portfolio

11.1.11.3.Collaborations & Alliances

11.1.11.4.Recent Developments

11.1.11.5.Financial Details

11.1.11.6.Others

11.1.12. SACHEM, Inc.

11.1.12.1.Business Description

11.1.12.2.Product Portfolio

11.1.12.3.Collaborations & Alliances

11.1.12.4.Recent Developments

11.1.12.5.Financial Details

11.1.12.6.Others

11.1.13. Kayaku Advanced Materials

11.1.13.1.Business Description

11.1.13.2.Product Portfolio

11.1.13.3.Collaborations & Alliances

11.1.13.4.Recent Developments

11.1.13.5.Financial Details

11.1.13.6.Others

11.1.14. Weifang Startech Microelectronic Materials

11.1.14.1.Business Description

11.1.14.2.Product Portfolio

11.1.14.3.Collaborations & Alliances

11.1.14.4.Recent Developments

11.1.14.5.Financial Details

11.1.14.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.