Mexico Paediatric Consumer Health Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Analgesics (Paediatric Acetaminophen, Paediatric Aspirin, Paediatric Combination Products Analgesics, Paediatric Dipyrone, Paediatric Ibuprofen, Paediatric Naproxen), Paediatric Cough, Cold and Allergy Remedies (Paediatric Allergy Remedies, Paediatric Cough/Cold Remedies), Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion and Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Paediatric Dermatologicals, Nappy (Diaper) Rash Treatments, Paediatric Vitamins and Dietary Supplements), By Dosage Form (Liquid Syrups, Chewable Tablets, Drops, Powders/Sachets, Gummies, Topical Creams & Ointments), By Age Group (Infants & Toddlers (0-3 Years), Children (4-12 Years), Adolescents (13-18 Years)), By Treatment Type (Acute Treatment, Chronic Condition Management, Genetic & Rare Disease Management), By Sales Channel (Retail Online (Online Pharmacies, E-commerce Platforms, Brand Websites), Retail Offline (Hospital Pharmacies, Retail Pharmacies / Drugstores, Supermarkets & Hypermarkets, Specialty Baby Stores)) ... Read more

|

Major Players

|

Mexico Paediatric Consumer Health Market Statistics and Insights, 2026

- Market Size Statistics

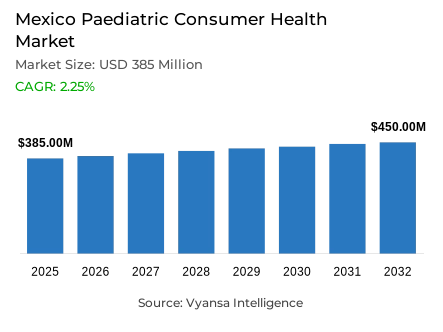

- Paediatric consumer health market size in Mexico was valued at USD 385 million in 2025 and is estimated at USD 395.43 million in 2026.

- The market size is expected to grow to USD 450 million by 2032.

- Market to register a CAGR of around 2.25% during 2026-32.

- Product Type Shares

- Paediatric vitamins and dietary supplements grabbed market share of 25%.

- Competition

- More than 20 companies are actively engaged in producing paediatric consumer health in Mexico.

- Top 5 companies acquired around 50% of the market share.

- Reckitt Benckiser México SA de CV, Laboratorios Andrómaco SA de CV, Genomma Lab Internacional SAB de CV, Bayer de México SA de CV, GlaxoSmithKline México SA de CV etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Mexico Paediatric Consumer Health Market Outlook

The Mexico paediatric consumer health market was valued at USD 385 million in 2025 and is projected to expand from USD 395.43 million in 2026 to USD 450 million by 2032, reflecting a compound annual growth rate of 2.25% over the forecast period. This growth trajectory is fundamentally underpinned by a strategic shift among end users toward proactive wellness management, as parents place increasing emphasis on developmental support and long‑term illness prevention as primary healthcare priorities for their children. Although the growth velocity has slowed moderately compared to the previous years, the increasing clinical burden of childhood obesity and chronic respiratory diseases guarantees a steady and uninterrupted demand of specialised therapeutic and nutritional interventions throughout the paediatric category.

Portfolio diversification within the market is increasingly oriented around specific and measurable health outcomes, with paediatric vitamins and dietary supplements accounting for 25% of total market share. End users in Mexico are progressively viewing these products as meaningful instruments for supporting cognitive development and academic performance, driving a pronounced preference for palatable and child‑friendly delivery formats including emulsions and gummy presentations. This expansion of the paediatric consumer health landscape is particularly evident in the growing consumption of iron and omega‑3 supplement formulations, which are widely regarded among end users for their capacity to support memory function and concentration levels during critical stages of childhood education and development.

The distribution framework across the market remains anchored in physical proximity and professional reliability, with retail offline accounting for 90% of total market share. The distribution environment is dominated by large pharmacy chain operators who exploit their large urban and rural retail networks, structured loyalty programmes and high-visibility promotional activity to maintain high end-user engagement levels. These retailers have managed to tailor their paediatric consumer health product lines to include a combination of both high-technology clinical skincare formulations and herbal remedy products, effectively meeting the needs of an end-user base that demands both scientific and natural ingredient disclosure in one trusted retail setting.

In the 2032 forecast horizon, the gradual adoption of precision health methods and digital health tools will transform the caregiving experience of a new generation of parents. The increasing use of artificial intelligence-based diagnostic platforms and wearable health monitoring devices by younger parent demographics is establishing new and valuable touchpoints of brand engagement in the paediatric consumer health category. With the industry still developing into more personalised treatment strategies and plant-based paediatric formulations with well-defined safety profiles, the industry is poised to maintain a consistent value growth by balancing the proven equity of trusted heritage brands with the new potential of data-driven and personalised childhood wellness management.

Mexico Paediatric Consumer Health Market Growth DriverPreventive Nutrition Assumes Greater Prominence Within Parental Health Priorities

Preventive nutrition is presumed to gain higher priority in parental health. Preventive care remains the main, structurally reinforced, force behind the Mexico paediatric consumer health market parents are increasingly focusing on nutrition, immunity support, and proactive health management as the cornerstones of childhood health. This trend is accelerating because parental interest in child health is no longer limited to the treatment of acute disease but to the long-term promotion of healthy growth and physical robustness. Vitamins, dietary supplements, and child‑focused wellness products benefit directly from this mindset, as end users commonly regard them as practical and accessible tools for reinforcing healthier daily routines from an early stage of childhood.

The importance of the overall child health burden in Mexico further supports this behavioural change. Available data indicate that 36.5% of school‑age children and 40.4% of adolescents in Mexico are living with overweight or obesity, thereby sustaining preventive nutrition as a prominent and ongoing priority on the family health agenda. School-based health-related programmes are also becoming larger in scale, with programmes aimed at enhancing food environments targeting over 34 million children and adolescents across the country this increases the institutional and societal focus on childhood nutritional health.

Mexico Paediatric Consumer Health Market ChallengeBroader Consumer Moderation Constrains the Pace of Category Growth

The challenges that the Mexico market is facing is the slowing rate of category demand growth, with the overall end user spending environment becoming softer and household buying behaviour more discriminating. Despite the fact that parents always give high priority to the expenditure on children health, the momentum of purchasing in the category is more restrained and value-conscious when the household budget is strained. This dynamic constrains the pace at which the paediatric consumer health market can grow, even in the situation when the availability of products is still increasing, and the level of awareness of supplements, respiratory remedies, and child-oriented over-the-counter product categories is still high.

This less aggressive macroeconomic environment is reflected in official data on private consumption. The National Institute of Statistics and Geography’s Timely Indicator of Private Consumption recorded annual declines of 1.3% in March 2025 and 1.1% in April 2025, with corresponding monthly declines of 0.2% and 0.1% respectively. Although this wider moderation does not eradicate underlying category demand, it does make growth slower and more price-sensitivity and perceived-value acutely sensitive across family health purchasing decisions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Paediatric Consumer Health Market TrendPharmacy Chain Strength and Retail Online Expansion Are Reshaping End User Purchasing Behaviour

The most evident and commercially relevant tendencies in the Mexico paediatric consumer health market is the increasing strategic value of channel strength, most notably by the twofold growth of pharmacy chain networks and retail online platforms. End users increasingly expect paediatric health products to be readily discoverable, easily comparable, and conveniently purchasable across both physical and digital touchpoints. This anticipation compels brands and retail operators to expand paediatric product lines with more child-friendly formats, increase product awareness in both channel settings, and make access more convenient to everyday respiratory, wellness, and personal care buying requirements.

The digital infrastructure in Mexico is currently very strong to support this channel evolution. The National Institute of Statistics and Geography reports 100.2 million internet end users in 2024, equivalent to 83.1% of the population aged 6 years and above. Data further indicate that 35.8% of internet end users made retail online purchases, with the proportion of the population buying products or services online increasing by 2.4 percentage points relative to 2023. This dynamic of retail online expansion continues despite the fact that the operators of pharmacy chains still play a very significant role in the family health purchasing decisions in both urban and non-urban regions.

Mexico Paediatric Consumer Health Market OpportunityImproving Household Financial Capacity Creates Meaningful Space for Premium Paediatric Products

There is a clear business opportunity in the creation and positioning of more value-added paediatric health products that integrate preventive nutritional advantages, quality-based product attributes, and brand equity. With the growing financial ability of households among the working population, parents are showing a greater readiness to spend on products that can provide proven convenience, proven safety standards, and more holistic support of the health and developmental outcomes of children. This provides growing business space to high-end supplement formulations, specialised respiratory solutions, and products that are framed around cognitive development and academic performance support.

There is substantive support of this opportunity through labour market data. The Mexico Social Security Institute reported a record 22,837,768 formal employment positions in Mexico as of November 2025, while the average base salary reached 624.9 pesos per day, representing a year‑on‑year increase of 7.0%. Having a larger formally employed population base and a significantly better wage level, an increasing percentage of families have more financial ability to channel expenditure into higher-quality paediatric consumer health products, beyond the purely necessary or low-cost purchases to more high-quality and differentiated products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Paediatric Consumer Health Market Segmentation Analysis

By Product Type

- Paediatric Analgesics

- Paediatric Acetaminophen

- Paediatric Aspirin

- Paediatric Combination Products Analgesics

- Paediatric Dipyrone

- Paediatric Ibuprofen

- Paediatric Naproxen

- Paediatric Cough, Cold and Allergy Remedies

- Paediatric Allergy Remedies

- Paediatric Cough/Cold Remedies

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion and Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Paediatric Dermatologicals

- Nappy (Diaper) Rash Treatments

- Paediatric Vitamins and Dietary Supplements

The segment with highest market share under product type is, paediatric vitamins and dietary supplements, accounting for 25% of total market share. This leadership role is indicative of the expanding and institutionally reinforced role of preventive care in the child health agenda in Mexico, with parents increasingly demanding practical and convenient means of sustaining childhood immunity, physical development, and overall health as part of the daily health practices. These products are generally viewed as a simple and effective way of supplementing nutritional intake in cases where caregivers do not feel that the normal dietary provision is adequate.

The segment also enjoys a wide relevance and applicability to various age groups of childhood and a wide spectrum of health and developmental issues. End users utilise these products not only for general wellness maintenance but also for more targeted applications including immunity reinforcement, cognitive development support, and healthy physical maturation. The fact that these formulations are available in child-friendly delivery systems, most prominently gummy and emulsion formulations, also contributes to product acceptance among children and repeat purchasing behaviour among parents, which in turn maintains the leading position of the segment in the overall product type mix.

By Sales Channel

- Retail Online

- Online Pharmacies

- E-commerce Platforms

- Brand Websites

- Retail Offline

- Hospital Pharmacies

- Retail Pharmacies / Drugstores

- Supermarkets & Hypermarkets

- Specialty Baby Stores

Within the sales channel segmentation, retail offline accounts for 90% of total market share, maintaining an overwhelming position of dominance within the paediatric consumer health distribution landscape in Mexico. This channel retains its primary status because end users continue to rely heavily on physical pharmacy outlets and established retail stores for the purchase of paediatric health products. The instant access to products when needed, confidence in known and familiar shopping conditions, and the practicality of direct product comparisons on-shelf are all very pertinent buying factors, especially when children need instant access to cough, cold, allergy, or personal care solutions.

The offline distribution of retail also enjoys the advantage of the large geographic coverage of the pharmacy chain networks in the urban centres and non-urban communities spread across Mexico. These stores go far beyond the traditional pharmaceutical product lines, and are increasingly carrying vitamins, child-friendly over-the-counter medicines, personal care products, and wider wellness products in one and trusted retail store. The established end-user trust, convenience in purchasing, and the high visibility of the product range allow physical retail to maintain its status as the main purchase channel of paediatric consumer health products, despite the growing commercial presence and end-user access of retail online channels throughout the market.

List of Companies Covered in Mexico Paediatric Consumer Health Market

The companies listed below are highly influential in the Mexico paediatric consumer health market, with a significant market share and a strong impact on industry developments.

- Reckitt Benckiser México SA de CV

- Laboratorios Andrómaco SA de CV

- Genomma Lab Internacional SAB de CV

- Bayer de México SA de CV

- GlaxoSmithKline México SA de CV

- Sanofi-Aventis de México SA de CV

- Pisa Laboratorios SA

- Abbott Laboratorios de México SA de CV

- Compañía Internacional de Comercio SAPI de CV

- Boehringer Ingelheim Promeco SA de CV

Competitive Landscape

Mexico paediatric consumer health market in 2025 reflects a competitive landscape shaped by established multinational brands, specialised infant-care companies, and expanding pharmacy retail networks. Bayer AG maintains the leading position, supported by its diversified paediatric OTC portfolio addressing respiratory conditions and allergy symptoms, with innovations such as Paediatric Cough Relief Sachet designed to improve dosing convenience and child-friendly administration. Meanwhile, premium infant-care specialist Laboratoires Expanscience is strengthening its presence through the Mustela portfolio, including products such as Mustela Stelatopia and Mustela Diaper Cream. Scientific research backing and natural ingredient positioning have reinforced consumer trust in the brand. Together, strong multinational portfolios and clinically positioned infant-care brands are intensifying competition across Mexico’s paediatric consumer health market.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Mexico Paediatric Consumer Health Market Policies, Regulations, and Standards

- Mexico Paediatric Consumer Health Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Mexico Paediatric Consumer Health Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Aspirin- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Combination Products Analgesics- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dipyrone- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Ibuprofen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Naproxen- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough, Cold and Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Allergy Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Cough/Cold Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion and Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Dermatologicals- Market Insights and Forecast 2022-2032, USD Million

- Nappy (Diaper) Rash Treatments- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Vitamins and Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Analgesics- Market Insights and Forecast 2022-2032, USD Million

- By Dosage Form

- Liquid Syrups- Market Insights and Forecast 2022-2032, USD Million

- Chewable Tablets- Market Insights and Forecast 2022-2032, USD Million

- Drops- Market Insights and Forecast 2022-2032, USD Million

- Powders/Sachets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Topical Creams & Ointments- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Infants & Toddlers (0-3 Years)- Market Insights and Forecast 2022-2032, USD Million

- Children (4-12 Years)- Market Insights and Forecast 2022-2032, USD Million

- Adolescents (13-18 Years)- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type

- Acute Treatment- Market Insights and Forecast 2022-2032, USD Million

- Chronic Condition Management- Market Insights and Forecast 2022-2032, USD Million

- Genetic & Rare Disease Management- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Online Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Brand Websites- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospital Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- Retail Pharmacies / Drugstores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets & Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Specialty Baby Stores

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Mexico Paediatric Analgesics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Paediatric Cough, Cold and Allergy Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Paediatric Dermatologicals Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Nappy (Diaper) Rash Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Paediatric Vitamins and Dietary Supplements Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Dosage Form- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Treatment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Bayer de México SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline México SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi-Aventis de México SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pisa Laboratorios SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratorios de México SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser México SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorios Andrómaco SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Genomma Lab Internacional SAB de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Compañía Internacional de Comercio SAPI de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boehringer Ingelheim Promeco SA de CV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer de México SA de CV

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Dosage Form |

|

| By Age Group |

|

| By Treatment Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.