India Data Center Maintenance & Support Services Market Report: Trends, Growth and Forecast (2026-2032)

By Service Type (Preventive & Predictive Maintenance Services, Corrective & Emergency Support Services, Remote & On-site Support Services, Lifecycle, Parts & Compliance Support Services, Managed Operations Services), By Supported Infrastructure (Power Infrastructure, Cooling Infrastructure, IT Infrastructure, Monitoring & Control Systems, Physical Security & Safety Systems), By Data Center Type (Enterprise Data Centers, Colocation Data Centers, Cloud/Hyperscale Data Centers, Edge/Modular Data Centers), By Tier Type (Tier I & Tier II, Tier III, Tier IV), By End User (IT & Telecommunications, BFSI, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Others), By Contract Type (Warranty & Post-Warranty Support, Comprehensive/Full-Service Contracts, Limited-Service Contracts, Time-and-Material/Ad Hoc Support, SLA-based Managed Support Contracts, Multi-Year Outsourced O&M Contracts), By Service Provider Type (OEM/Manufacturer Support Providers, Third-Party Maintenance Providers, Multi-Vendor Support Providers, System Integrators/IT Infrastructure Service Providers, Colocation Operator-led Support Providers, Specialized Critical Facility O&M Providers), By Data Center Size (Small Data Centers, Medium Data Centers, Large Data Centers, Hyperscale Facilities), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Data Center Maintenance & Support Services Market Statistics and Insights, 2026

- Market Size Statistics

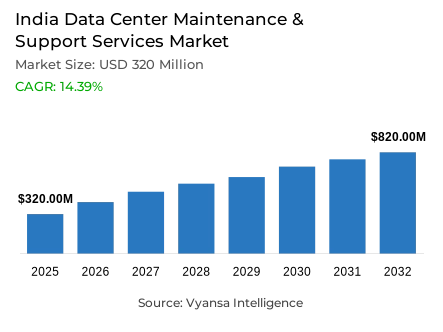

- Data center maintenance & support services market size in India was valued at USD 320 million in 2025 and is estimated at USD 366 million in 2026.

- The market size is expected to grow to USD 820 million by 2032.

- Market to register a CAGR of around 14.39% during 2026-32.

- Service Type Shares

- Managed operations services grabbed market share of 25%.

- Competition

- More than 10 companies are actively engaged in producing data center maintenance & support services in India.

- Top 5 companies acquired around 40% of the market share.

- Amazon Web Services (AWS), Google Cloud, Vertiv India, CtrlS Datacenters, STT GDC India etc., are few of the top companies.

- Supported Infrastructure

- Power infrastructure grabbed 35% of the market.

India Data Center Maintenance & Support Services Market Outlook

The India data center maintenance & support services market was valued at USD 320 million in 2025, establishing a commercially dynamic and structurally well supported foundation within one of Asia's most rapidly scaling digital infrastructure ecosystems. Projected to advance from USD 366 million in 2026 to USD 820 million by 2032, the sector registers a compound annual growth rate of 14.39% across the forecast horizon a near tripling of market value that reflects the structural transformation of data center operations from asset ownership models toward integrated, continuously managed service ecosystems. This expansion trajectory is not driven by cyclical technology spending but by the compounding interaction of four durable forces an explosively expanding national digital subscriber base, the accelerating deployment of hyperscale and AI led data center infrastructure, the rising complexity of power critical uptime management, and a policy framework designed to attract sustained cloud and digital infrastructure investment into India across a multi decade horizon.

The service architecture defining this market's commercial structure is anchored in managed operations functions, where managed operations services command approximately 25% of total market share the single largest service type concentration within the industry. This dominant position reflects a fundamental and accelerating shift in how data center operators approach facility management moving decisively away from reactive, event triggered maintenance interventions toward continuous oversight models that deliver stable day to day performance, proactive fault management, and consistent service level compliance across enterprise scale and colocation led operating environments. This preference transition signals a market whose commercial center of gravity is shifting from transactional service procurement toward long cycle, relationship anchored managed service partnerships that generate recurring revenue streams and deepen provider operator dependencies across the forecast horizon.

The infrastructure architecture reinforces the primacy of power systems as the category's dominant service priority, with power infrastructure commanding approximately 35% of total supported infrastructure market share. This leadership reflects the irreducible operational reality of data center maintenance & support services power continuity is not a discretionary service parameter but the foundational prerequisite upon which all computational, cooling, and connectivity performance outcomes depend. In an environment where India successfully met a peak power demand of 242.49 GW during FY 2025-26 and where hyperscale projects of the scale of Google's planned 1 GW Visakhapatnam facility are entering the development pipeline the complexity and criticality of power infrastructure maintenance are escalating simultaneously, sustaining disproportionate service investment concentration within this infrastructure category.

The forward outlook through 2032 is defined by the convergence of a digital subscriber base that has crossed one billion total internet subscribers documented by TRAI at 1,002.85 million as of June 2025 with hyperscale infrastructure investment announcements of approximately USD 90 billion in AI linked data center development creating a facility expansion pipeline whose operational support requirements will structurally deepen service demand across every maintenance and support category. The proposed tax holiday for eligible foreign cloud service providers applicable from Tax Year 2026-27 through Tax Year 2046 47 and linked to procurement obligations from Indian data center operators further amplifies the long term commercial visibility for maintenance and lifecycle support partners positioned to scale alongside India's expanding cloud and digital infrastructure base through 2032.

India Data Center Maintenance & Support Services Market Growth Driver

Expanding Digital Subscriber Base Deepens Infrastructure Utilization and Service Demand

The rapid and institutionally documented expansion of India's national digital subscriber base represents the primary structural driver of data center maintenance and support services demand functioning as the foundational demand generation mechanism that continuously intensifies infrastructure utilization, elevates uptime criticality, and sustains the operational pressure that makes managed maintenance services commercially indispensable across India's expanding data center ecosystem. As more Indian consumers and enterprises deepen their digital engagement, the volume of workloads, data transactions, and connectivity demands flowing through India's data center infrastructure compounds consistently creating a structural demand escalation dynamic whose commercial implications for maintenance and support service intensity are direct, measurable, and durable across the forecast horizon.

The quantitative momentum of this connectivity driven demand dynamic is documented with precision by the Telecom Regulatory Authority of India. Total internet subscribers in India reached 1,002.85 million at the end of June 2025 with broadband subscribers standing at 979.71 million establishing a massive and continuously expanding digital consumer base whose sustained engagement generates persistent infrastructure utilization pressure across the data center facilities serving their connectivity, content, and cloud service requirements. Total wireless data usage reached 65,009 PB during the quarter ended June 2025, while average wireless data usage per subscriber per month rose to 24.01 GB in the same period confirming the relentless traffic volume intensification that elevates infrastructure maintenance complexity, accelerates equipment wear cycles, and sustains consistent demand for preventive maintenance, fault management, and technical support services through 2032.

India Data Center Maintenance & Support Services Market Challenge

Power Critical Uptime Complexity Elevates Service Delivery Demands

The escalating scale and operational complexity of power infrastructure management within India's data center environment represents the most consequential service delivery challenge confronting maintenance and support providers creating systematic technical capability, workforce competency, and infrastructure redundancy management demands that intensify as both national power grid utilization expands and individual facility power density escalates toward hyperscale configurations. In an environment where even brief power continuity disruptions translate directly into service level agreement breaches, enterprise workload interruptions, and reputational damage for both facility operators and their maintenance service partners, the pressure to maintain flawless electrical reliability, backup system readiness, and cooling continuity across increasingly large and complex power environments is structurally and continuously intensifying.

The quantitative scale of this power management challenge is documented with institutional authority by the Ministry of Power and the Press Information Bureau. India successfully met a peak power demand of 242.49 GW during FY 2025 26 confirming the national grid utilization scale within which data center power infrastructure operates and whose volatility maintenance teams must actively manage through robust backup and redundancy systems. The challenge reaches its most acute expression in hyperscale development Google's planned Visakhapatnam project India's first 1 GW hyperscale data center and AI hub will require dedicated and purpose built power and cooling infrastructure whose maintenance complexity substantially exceeds anything currently operational within India's data center market. For service providers, navigating this power complexity escalation demands simultaneous investment in technical workforce specialization, redundancy management methodology, and real time monitoring capability through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Data Center Maintenance & Support Services Market Trend

AI Led Hyperscale Development Redefines Service Model Requirements

The accelerating development of AI linked hyperscale data center infrastructure across India represents the defining structural trend reshaping the maintenance and support services market fundamentally elevating the technical complexity, service intensity, and operational specialization requirements of facility support contracts while simultaneously expanding the total addressable service opportunity to a scale that has no precedent in India's prior data center development history. This trend moves the competitive conversation in the maintenance and support services market beyond routine preventive maintenance and reactive fault response into the domain of continuous high density infrastructure oversight, AI workload optimized cooling management, and sub minute incident response performance dimensions that are redefining service provider capability requirements and contract value thresholds across the industry's most commercially significant emerging segment.

The investment scale and operational specificity of this hyperscale AI development trend are documented with authority by the Press Information Bureau. Investments of approximately USD 70 billion are currently underway in India, with data center announcements particularly AI data centers reaching approximately USD 90 billion and confirming the structural commitment of global technology operators to India as a primary AI infrastructure deployment geography. Google's Visakhapatnam facility India's first 1 GW hyperscale data center and the country's first Google AI hub will require essential manpower, infrastructure, power, and cooling facilities at a scale and technical complexity that defines a new service delivery standard for India's maintenance and support ecosystem. As AI linked workloads expand and hyperscale facility density deepens, maintenance and support service models will be progressively redefined by the operational demands of these flagship infrastructure deployments through 2032.

India Data Center Maintenance & Support Services Market Opportunity

Policy Backed Investment Framework Creates Durable Long Term Service Demand Visibility

The comprehensive and long horizon policy framework being deployed by the Indian government to attract foreign cloud and digital infrastructure investment into the country creates a structurally significant and commercially durable opportunity for data center maintenance and support service providers delivering a policy guaranteed demand expansion dynamic whose multi decade time horizon substantially exceeds the investment visibility available in most infrastructure services market contexts. This policy opportunity is distinguished from conventional market demand by its structural predictability the regulatory linkage between foreign operator tax incentives and Indian data center service procurement creates a contractually embedded demand commitment that sustains maintenance service engagement across the full lifecycle of the qualifying infrastructure investment independent of cyclical technology spending fluctuations.

The commercial specificity and long term scale of this policy opportunity are documented with precision by the Press Information Bureau. The proposed tax holiday for eligible foreign cloud service providers applies from Tax Year 2026 27 through Tax Year 2046 47 a 20 year incentive horizon that creates exceptional long cycle investment visibility for Indian data center operators and their maintenance service ecosystem partners. The eligibility framework's requirement that qualifying foreign companies procure data center services from Indian operators creates a structural procurement obligation that directly sustains domestic maintenance and support service demand across the incentive period. The proposed 15% safe harbour margin on cost for related entity arrangements further improves service contract economics and commercial predictability for compliant Indian service providers positioned within qualifying operator supply chains. Maintenance and support providers that align their service delivery capability, compliance infrastructure, and long term capacity investment with this policy framework will capture disproportionate value from India's most structurally guaranteed digital infrastructure growth opportunity through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Data Center Maintenance & Support Services Market Segmentation Analysis

By Service Type

- Preventive & Predictive Maintenance Services

- Corrective & Emergency Support Services

- Remote & On-site Support Services

- Lifecycle, Parts & Compliance Support Services

- Managed Operations Services

The segment with highest market share under the service type is managed operations services, accounting for approximately 25% of the total market. This commanding position reflects the deep structural alignment between continuous managed service models and the operational requirements of data center operators whose uptime commitments, infrastructure complexity, and performance level obligations make reactive, event driven maintenance approaches commercially and operationally inadequate across both enterprise owned and colocation facility environments. With one quarter of total market value concentrated within a single service type, managed operations services define the commercial priorities, contract structure dynamics, and long term service relationship frameworks of the India data center maintenance and support services industry establishing the operational continuity standards, service level agreement expectations, and outsourcing investment thresholds against which all alternative service delivery models are evaluated.

The structural leadership of managed operations services is further reinforced by the growing operational burden that scaling data center infrastructure places on in house facility management teams a burden that is intensifying as AI linked hyperscale deployments introduce denser compute environments, more complex cooling architectures, and faster incident response expectations that exceed the capacity of conventional internal operations models. As total wireless data usage reaches 65,009 PB during the quarter ended June 2025 and average data consumption per subscriber rises to 24.01 GB per month confirming the relentless traffic volume growth that sustains infrastructure utilization pressure the operational case for continuous managed oversight strengthens commensurately. The segment's structural centrality to service purchasing behavior, outsourcing strategy, and long term commercial market development is expected to deepen through 2032.

By Supported Infrastructure

- Power Infrastructure

- Cooling Infrastructure

- IT Infrastructure

- Monitoring & Control Systems

- Physical Security & Safety Systems

The segment with highest market share under the supported infrastructure is power infrastructure, accounting for approximately 35% of the total market. This dominant position reflects the foundational operational reality of data center management where uninterrupted electrical performance, backup system readiness, and the stable functioning of power distribution and conditioning systems represent the non negotiable prerequisites upon which all computational, connectivity, and cooling performance outcomes depend. With more than one third of total market value concentrated within a single infrastructure category, power infrastructure defines the service investment priorities, risk management frameworks, and technical capability requirements of the India data center maintenance and support services market establishing the reliability standards, redundancy management disciplines, and electrical continuity protocols that all service providers must demonstrate credibly to compete for high value facility support contracts.

The structural leadership of power infrastructure is being actively intensified by the hyperscale development wave that is transforming India's data center landscape from mid density enterprise facilities into gigawatt scale AI infrastructure complexes whose power management complexity vastly exceeds the operational support requirements of conventional data center environments. India's documented peak power demand achievement of 242.49 GW during FY 2025 26 combined with Google's planned 1 GW hyperscale data center and AI hub in Visakhapatnam requiring dedicated power and cooling infrastructure confirms that the scale and complexity of power related maintenance obligations are expanding at a pace that is structurally elevating service investment within this category. Power infrastructure's position as the market's dominant service investment priority and primary risk management focus is expected to deepen and consolidate through 2032.

List of Companies Covered in India Data Center Maintenance & Support Services Market

The companies listed below are highly influential in the India data center maintenance & support services market, with a significant market share and a strong impact on industry developments.

- Amazon Web Services (AWS)

- Google Cloud

- Vertiv India

- CtrlS Datacenters

- STT GDC India

- NTT Global Data Centers India

- Yotta Data Services

- Sify Technologies

- AdaniConneX

- Schneider Electric India

Market News & Updates

- Vertiv India, 2026:

In January 2026, Vertiv launched Vertiv™ Next Predict, an AI-powered managed service that the company says transforms data center maintenance by continuously analyzing equipment behavior, using anomaly detection and predictive algorithms to identify risks early across power, cooling, and IT systems; Vertiv’s India services portfolio also highlights remote monitoring, diagnostics, alarm management, and remote system restoration for data center operators. For the Data Center Maintenance & Support Services market in India, this is one of the most relevant verified service updates because it signals a shift from periodic and reactive maintenance toward condition-based, analytics-driven support, which can improve uptime, reduce unplanned outages, and accelerate adoption of predictive maintenance contracts among Indian colocation, enterprise, and AI data center operators.

- Sify Technologies, 2026:

In February 2026, Sify Digital Services and HCLSoftware announced an India-focused partnership to launch a fully managed Sovereign AI offering for Indian enterprises, with Sify providing the sovereign infrastructure, platform services, foundation models, and specialized blueprints as part of an outcome-oriented managed-service model designed to keep data within India and meet local compliance needs. For the Data Center Maintenance & Support Services market in India, this is a significant verified development because it pushes support demand beyond basic uptime into higher-value managed operations, compliance-led infrastructure management, and lifecycle service delivery for AI workloads, which should raise customer expectations for integrated monitoring, managed hosting, and ongoing operational support from Indian data center service providers.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Data Center Maintenance & Support Services Market Policies, Regulations, and Standards

- India Data Center Maintenance & Support Services Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Data Center Maintenance & Support Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Type

- Preventive & Predictive Maintenance Services- Market Insights and Forecast 2022-2032, USD Million

- Corrective & Emergency Support Services- Market Insights and Forecast 2022-2032, USD Million

- Remote & On-site Support Services- Market Insights and Forecast 2022-2032, USD Million

- Lifecycle, Parts & Compliance Support Services- Market Insights and Forecast 2022-2032, USD Million

- Managed Operations Services- Market Insights and Forecast 2022-2032, USD Million

- By Supported Infrastructure

- Power Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- Cooling Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- IT Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- Monitoring & Control Systems- Market Insights and Forecast 2022-2032, USD Million

- Physical Security & Safety Systems- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type

- Enterprise Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Colocation Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Cloud/Hyperscale Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Edge/Modular Data Centers- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type

- Tier I & Tier II- Market Insights and Forecast 2022-2032, USD Million

- Tier III- Market Insights and Forecast 2022-2032, USD Million

- Tier IV- Market Insights and Forecast 2022-2032, USD Million

- By End User

- IT & Telecommunications- Market Insights and Forecast 2022-2032, USD Million

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- Government & Defense- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Energy & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type

- Warranty & Post-Warranty Support- Market Insights and Forecast 2022-2032, USD Million

- Comprehensive/Full-Service Contracts- Market Insights and Forecast 2022-2032, USD Million

- Limited-Service Contracts- Market Insights and Forecast 2022-2032, USD Million

- Time-and-Material/Ad Hoc Support- Market Insights and Forecast 2022-2032, USD Million

- SLA-based Managed Support Contracts- Market Insights and Forecast 2022-2032, USD Million

- Multi-Year Outsourced O&M Contracts- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type

- OEM/Manufacturer Support Providers- Market Insights and Forecast 2022-2032, USD Million

- Third-Party Maintenance Providers- Market Insights and Forecast 2022-2032, USD Million

- Multi-Vendor Support Providers- Market Insights and Forecast 2022-2032, USD Million

- System Integrators/IT Infrastructure Service Providers- Market Insights and Forecast 2022-2032, USD Million

- Colocation Operator-led Support Providers- Market Insights and Forecast 2022-2032, USD Million

- Specialized Critical Facility O&M Providers- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size

- Small Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Medium Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Large Data Centers- Market Insights and Forecast 2022-2032, USD Million

- Hyperscale Facilities- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Service Type

- Market Size & Growth Outlook

- India Preventive & Predictive Maintenance Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Supported Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Corrective & Emergency Support Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Supported Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Remote & On-site Support Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Supported Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Lifecycle, Parts & Compliance Support Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Supported Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Managed Operations Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Supported Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Type- Market Insights and Forecast 2022-2032, USD Million

- By Tier Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Contract Type- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider Type- Market Insights and Forecast 2022-2032, USD Million

- By Data Center Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- CtrlS Datacenters

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STT GDC India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NTT Global Data Centers India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yotta Data Services

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sify Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AdaniConneX

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vertiv India

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amazon Web Services (AWS)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google Cloud

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CtrlS Datacenters

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Service Type |

|

| By Supported Infrastructure |

|

| By Data Center Type |

|

| By Tier Type |

|

| By End User |

|

| By Contract Type |

|

| By Service Provider Type |

|

| By Data Center Size |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.