India Clinical Laboratory Services Market Report: Trends, Growth and Forecast (2026-2032)

By Test Type (Clinical Chemistry (Routine Chemistry Testing, Therapeutic Drug Monitoring Testing, Endocrinology Chemistry Testing, Specialized Chemistry Testing, Other Clinical Chemistry Testing), Hematology Testing, Medical Microbiology (Infectious Disease Testing, Transplant Diagnostic Testing, Other Microbiology Testing), Immunology & Serology Testing, Molecular Diagnostics, Genetic Testing, Pathology (Cytopathology, Histopathology), Blood Banking & Transfusion Services, Toxicology & Drug Abuse Testing, Other Specialty/Esoteric Tests), By Service Provider (Hospital-based Laboratories, Independent/Standalone Clinical Laboratories, Clinic/Physician Office Laboratories, Public Health Laboratories, Specialty Laboratories), By Application (Routine Diagnostic Testing, Chronic Disease Testing, Infectious Disease Testing, Oncology Testing, Preventive/Screening Testing, Specialized/Genetic Testing), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Clinical Laboratory Services Market Statistics and Insights, 2026

- Market Size Statistics

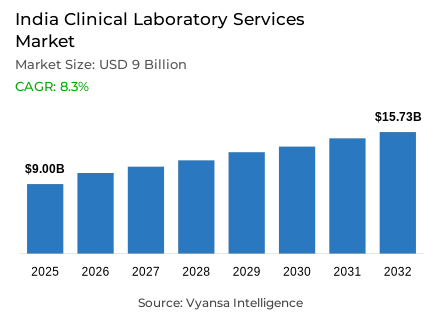

- Clinical laboratory services market size in India was valued at USD 9 billion in 2025 and is estimated at USD 9.75 billion in 2026.

- The market size is expected to grow to USD 15.73 billion by 2032.

- Market to register a CAGR of around 8.3% during 2026-32.

- Test Type Shares

- Clinical chemistry grabbed market share of 25%.

- Competition

- More than 10 companies are actively engaged in producing clinical laboratory services in India.

- Top 5 companies acquired around 15% of the market share.

- Neuberg Diagnostics, Apollo Diagnostics, Aarthi Scans & Labs, Dr Lal PathLabs, Metropolis Healthcare etc., are few of the top companies.

- Service Provider

- Independent/standalone clinical laboratories grabbed 45% of the market.

India Clinical Laboratory Services Market Outlook

The India clinical laboratory services market was valued at USD 9 billion in 2025, establishing a commercially dynamic and institutionally well-supported foundation within one of the world's most rapidly expanding healthcare diagnostics ecosystems. Projected to advance from USD 9.75 billion in 2026 to USD 15.73 billion by 2032, the sector registers a CAGR of 8.3% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the convergence of accelerating national disease screening programs, progressive public health infrastructure investment, and the deepening integration of diagnostic testing into routine preventive and chronic disease management care pathways across India's diverse and rapidly modernizing healthcare delivery landscape. Growth is anchored in genuine institutional and population health imperatives rather than discretionary healthcare spending cycles, giving this market a commercial resilience that sustains consistent laboratory service demand across diverse economic and geographic contexts.

The test type architecture defining this market's commercial structure is anchored in clinical chemistry testing. Clinical Chemistry commands approximately 25% of total test type market share, reflecting the consistent and broad clinical preference for routine biochemical testing whose high-volume applicability, repeat evaluation frequency, and broad relevance across metabolic monitoring, organ function assessment, and chronic disease management make it the reference test category across the country's most commercially significant laboratory service environments. The Ministry of Health and Family Welfare's documentation of 4.67 million USD hypertension screenings and USD 4.34 million diabetes screenings conducted under the NP-NCD programme by October 2025 confirms the institutional screening scale that sustains consistent clinical chemistry testing demand across hospital-based, independent, and primary care-linked laboratory service settings nationwide.

The service provider architecture reinforces the structural centrality of independent and standalone clinical laboratories as the category's dominant service delivery platform. Independent and Standalone Clinical Laboratories command approximately 45% of total service provider market share, reflecting the geographic accessibility, patient convenience, and recurring diagnostic testing service characteristics that make standalone laboratory networks the preferred testing service delivery model across India's diverse urban, semi-urban, and community healthcare markets. This provider concentration confirms that laboratory service buyers and clinical referrers consistently prioritize accessible, efficiently managed testing networks whose neighborhood presence, result delivery speed, and broad test menu availability create natural and durable utilization advantages across routine and preventive diagnostic care contexts throughout the national market.

The future outlook is defined by four converging structural forces whose combined commercial impact creates a clinical laboratory services market of sustained and well-grounded expansion momentum. The Ministry of Health and Family Welfare's documentation of 42.01 million people receiving hypertension treatment and 25.27 million receiving diabetes treatment by March 2025 confirms the structured chronic disease management demand that sustains consistent periodic testing utilization across the national patient population enrolled in organized care pathways. The Ayushman Bharat Digital Mission's creation of more than 9.6 USD million ABHA accounts by August 2025, alongside 1,59,020 ABDM-enabled health facilities and approximately 5.91 USD million linked health records, confirms the digital connectivity infrastructure that is progressively reshaping laboratory workflow efficiency and result delivery capability across India's national health ecosystem. The PM-ABHIM sanction of 744 Integrated Public Health Laboratories and 621 Critical Care Blocks by November 2025 creates structured public sector laboratory infrastructure investment that opens substantial new capacity development opportunity for equipment, workflow management, and specialized testing partnership across the national healthcare system over the forecast period.

India Clinical Laboratory Services Market Growth Driver

National Screening Program Scale Sustains High-Volume Diagnostic Testing Demand

The large-scale and institutionally documented expansion of India's national noncommunicable disease screening and treatment programs represents the primary structural driver of clinical laboratory services demand, functioning as a persistent testing volume generation mechanism that sustains consistent biochemical monitoring, confirmation testing, and treatment follow-up diagnostic activity across public and private laboratory service networks throughout the national healthcare delivery system. This screening program-driven demand dynamic creates a testing volume base that sustains laboratory service utilization independently of discretionary healthcare spending fluctuations, reflecting a genuine public health management necessity whose diagnostic support requirements are irreducible across the full patient management cycle of India's most prevalent chronic conditions.

The quantitative evidence validating this screening program-driven demand dynamic is documented with precision by the Ministry of Health and Family Welfare and the Press Information Bureau. A total of USD 4.7 million hypertension screenings and USD 4.34 million diabetes screenings were conducted under the NP-NCD programme by October 2025, confirming the national screening volume that sustains consistent clinical chemistry and metabolic testing demand across primary care, hospital-based, and independent laboratory service environments. The Press Information Bureau's documentation that 42.01 million people had received treatment for hypertension and 25.27 million for diabetes by March 2025 under the national initiative confirms the structured chronic disease management demand that generates consistent periodic monitoring testing requirements across a large and growing enrolled patient population. These screening and treatment coverage metrics validate a demand expansion dynamic of sufficient institutional scale and chronicity to sustain structural laboratory services market growth over the forecast period.

India Clinical Laboratory Services Market Challenge

Diagnostic Access Gaps at Primary Care Level Limit Service Reach and Efficiency

The structural gap between the geographic breadth of India's primary care network and the diagnostic test menu depth available at lower-tier facilities represents the most consequential operational challenge confronting the India clinical laboratory services market, creating systematic patient referral, sample transportation, and result delivery inefficiencies that moderate service convenience, increase care pathway complexity, and limit the translation of primary care patient volumes into efficiently served laboratory testing demand across the national healthcare system. In a healthcare delivery environment where first-contact primary care facilities generate the largest volumes of initial patient encounters, the limited diagnostic capability at these facilities creates consistent referral pressure that adds cost, time, and inconvenience to the diagnostic care journey for patients and providers alike.

The structural depth and facility-tier specificity of this diagnostic access challenge are documented with precision by the Ministry of Health and Family Welfare. Free diagnostics at public facilities cover 14 tests at SHC-Ayushman Arogya Mandirs, 63 tests at PHC-AAMs, 97 tests at Community Health Centres, 111 tests at Sub-District Hospitals, and 134 tests at District Hospitals, confirming the progressive test menu limitation at lower-tier facilities that creates referral demand for more comprehensive diagnostic testing across the national primary care network. The Ministry's documentation of 1,82,944 Ayushman Arogya Mandirs operationalized by December 2025 confirms that the scale of the primary care network whose diagnostic capacity constraints generate referral demand is exceptionally large, creating both a service gap challenge and a market development opportunity for laboratory providers capable of efficiently serving the diagnostic overflow from India's most extensive public primary care infrastructure. Navigating this challenge demands investment in sample logistics, collection point expansion, and result delivery infrastructure that bridges the diagnostic capability gap between primary care facilities and comprehensive laboratory service networks over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Clinical Laboratory Services Market Trend

Digital Health Integration Reshapes Laboratory Service Connectivity and Workflow Efficiency

The accelerating adoption of the Ayushman Bharat Digital Mission infrastructure across India's healthcare delivery ecosystem represents the defining structural trend reshaping laboratory service workflows, result delivery standards, and competitive differentiation parameters within the national clinical laboratory services market. This digital integration trend is progressively transforming laboratory service delivery from a fragmented, paper-based testing model into a connected, data-enabled service ecosystem where ABHA-linked patient identification, ABDM-enabled result sharing, and interoperable health record integration collectively create faster, more coordinated, and more clinically valuable diagnostic service experiences across the diverse patient and provider populations served by India's national laboratory service network.

The institutional momentum and implementation scale of this digital integration trend are documented with authority by the Press Information Bureau. More than USD 9.6 million ABHA accounts had been created by August 2025, alongside more than 0.0050 USD million registered health facilities and0.0082 USD million registered healthcare professionals under ABDM, confirming that the digital health identity and provider registration infrastructure necessary for connected laboratory service workflows has achieved meaningful national scale. A total of 1,59,020 health facilities were using ABDM-enabled software and approximately USD 5.9 million health records had been linked with ABHA by February 2025, confirming that digital health record integration is advancing from pilot implementation into mainstream operational adoption across India's healthcare delivery network. As ABDM connectivity deepens across laboratory facilities, clinician systems, and patient health records, laboratory providers with established ABDM-compatible infrastructure and interoperable result delivery capability will capture disproportionate referral volume and physician loyalty over the forecast period.

India Clinical Laboratory Services Market Opportunity

Public Health Infrastructure Expansion Creates Structured Laboratory Capacity Development Openings

The systematic expansion of organized public health laboratory infrastructure under the PM-ABHIM program and the Ayushman Arogya Mandir network creates the India clinical laboratory services market's most structurally significant and institutionally certain growth opportunity, delivering a government-guaranteed infrastructure investment program whose facility development scope, geographic breadth, and long-horizon implementation commitment generate laboratory equipment partnership, workflow management, and specialized testing service opportunities of exceptional commercial scale and revenue visibility across the national public health system. This public infrastructure opportunity is distinguished from conventional private sector market growth by its institutional investment certainty, its systematic geographic reach across previously underserved districts and states, and the structured demand expansion it creates across the full spectrum of laboratory service categories from basic biochemistry through specialist and referral testing.

The quantitative scale and implementation specificity of this public infrastructure opportunity are documented with precision by the Ministry of Health and Family Welfare. A total of 744 Integrated Public Health Laboratories and 621 Critical Care Blocks had been approved and sanctioned under PM-ABHIM by November 2025, confirming the institutional investment commitment behind India's public laboratory infrastructure expansion program whose implementation will progressively expand laboratory service capacity, geographic reach, and diagnostic capability across previously underserved regions of the national healthcare system. The operationalization of 1,82,944 Ayushman Arogya Mandirs by December 2025, with diagnostic support covering 14 tests at SHC-AAMs and 63 tests at PHC-AAMs, establishes a primary care laboratory service integration platform whose systematic expansion of test menu breadth and sample referral volumes creates consistent and growing demand for private laboratory partnership across sample processing, specialized testing, and quality management functions. Laboratory service providers that align equipment supply, quality system support, and specialized testing partnership capability with India's public health laboratory infrastructure development priorities will capture disproportionate value from this structurally significant and policy-guaranteed market development opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Clinical Laboratory Services Market Segmentation Analysis

By Test Type

- Clinical Chemistry

- Routine Chemistry Testing

- Therapeutic Drug Monitoring Testing

- Endocrinology Chemistry Testing

- Specialized Chemistry Testing

- Other Clinical Chemistry Testing

- Hematology Testing

- Medical Microbiology

- Infectious Disease Testing

- Transplant Diagnostic Testing

- Other Microbiology Testing

- Immunology & Serology Testing

- Molecular Diagnostics

- Genetic Testing

- Pathology

- Cytopathology

- Histopathology

- Blood Banking & Transfusion Services

- Toxicology & Drug Abuse Testing

- Other Specialty/Esoteric Tests

The segment with highest market share under the Test Type is Clinical Chemistry, accounting for approximately 25% of the total market. This leading position reflects the deep structural alignment between clinical chemistry testing capabilities and the specific diagnostic workflow requirements of India's most institutionally significant laboratory service environments, where the high-volume applicability, repeat testing frequency, and broad clinical relevance of biochemical analysis across metabolic assessment, organ function monitoring, chronic disease management, and routine health screening make clinical chemistry the reference test category across hospital-based, independent, and primary care-linked laboratory settings nationwide. With one-quarter of total market value concentrated within a single test type category, Clinical Chemistry defines the equipment investment priorities, reagent procurement frameworks, and operational capacity planning benchmarks of the India clinical laboratory services market.

The structural leadership of Clinical Chemistry is being actively sustained by the large-scale national screening and treatment programs that are systematically expanding the chronic disease patient population requiring consistent biochemical monitoring across India's public and private healthcare delivery networks. The Ministry of Health and Family Welfare's documentation of USD 4.67 million hypertension screenings and USD 4.34 million diabetes screenings under NP-NCD by October 2025 confirms the institutional testing volume that drives consistent clinical chemistry service demand across facilities at every tier of the national healthcare system. As more patients enter structured treatment pathways for hypertension, diabetes, and related metabolic conditions, the periodic monitoring requirements that clinical chemistry testing fulfills will compound consistently across the forecast period. The segment's structural commercial leadership is expected to consolidate over the forecast period.

By Service Provider

- Hospital-based Laboratories

- Independent/Standalone Clinical Laboratories

- Clinic/Physician Office Laboratories

- Public Health Laboratories

- Specialty Laboratories

The segment with highest market share under the Service Provider is Independent and Standalone Clinical Laboratories, accounting for approximately 45% of the total market. This dominant position reflects the foundational operational reality of Indian clinical diagnostics, where the geographic accessibility, patient convenience, physician referral responsiveness, and recurring diagnostic service availability of standalone laboratory networks generate the highest concentration of routine, preventive, and monitoring-linked testing demand across urban and semi-urban healthcare markets nationwide. With nearly half of total market value anchored in independent laboratory service delivery, this provider segment defines the turnaround time benchmarks, test menu breadth expectations, and patient access standards of the India clinical laboratory services market.

he structural leadership of Independent and Standalone Clinical Laboratories is being actively sustained by the progressive expansion of physician-referred and direct-access diagnostic testing demand across India's growing urban middle-class and healthcare-engaged populations, whose testing utilization patterns favor accessible, efficiently managed laboratory networks over more institutionally complex hospital-based alternatives for routine and preventive care diagnostics. As the Ayushman Bharat Digital Mission advances ABDM-enabled software adoption across health facilities and health record linkage expands, standalone laboratory networks with robust digital result delivery and physician connectivity infrastructure will deepen their competitive advantage over less-connected alternatives. The segment's structural commercial dominance as the market's primary service delivery platform is expected to strengthen over the forecast period.

List of Companies Covered in India Clinical Laboratory Services Market

The companies listed below are highly influential in the India clinical laboratory services market, with a significant market share and a strong impact on industry developments.

- Neuberg Diagnostics

- Apollo Diagnostics

- Aarthi Scans & Labs

- Dr Lal PathLabs

- Metropolis Healthcare

- Agilus Diagnostics

- Thyrocare

- Vijaya Diagnostic Centre

- Medall Healthcare

- Healthians

Market News & Updates

- Agilus Diagnostics, 2025:

Fortis Healthcare launched the Fortis Institute of Genomic Medicine with support from Agilus Diagnostics’ nationwide footprint, positioning it as a precision-medicine platform spanning oncology, cardiology, and neurology and outlining plans for AI-powered genomic reporting. For the India clinical laboratory services market, this is one of the strongest service-launch developments because it expands access to advanced genomic interpretation and strengthens the integration of high-complexity molecular diagnostics into mainstream specialty care.

- Metropolis Healthcare, 2025:

Metropolis said it launched multiple innovation-led diagnostic upgrades, including AI-powered karyotyping, an HPV DNA self-sampling kit, expanded premium NGS panels, and a revamped app with AI-powered health insights and real-time sample tracking. For the India clinical laboratory services market, this is a meaningful product-and-service upgrade because it combines digital access, self-collection, and higher-complexity genomic testing in ways that can improve convenience and broaden the reach of organized diagnostic services

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Clinical Laboratory Services Market Policies, Regulations, and Standards

- India Clinical Laboratory Services Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Clinical Laboratory Services Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Test Type

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- Routine Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Therapeutic Drug Monitoring Testing- Market Insights and Forecast 2022-2032, USD Million

- Endocrinology Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Clinical Chemistry Testing- Market Insights and Forecast 2022-2032, USD Million

- Hematology Testing- Market Insights and Forecast 2022-2032, USD Million

- Medical Microbiology- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Transplant Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Microbiology Testing- Market Insights and Forecast 2022-2032, USD Million

- Immunology & Serology Testing- Market Insights and Forecast 2022-2032, USD Million

- Molecular Diagnostics- Market Insights and Forecast 2022-2032, USD Million

- Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- Pathology- Market Insights and Forecast 2022-2032, USD Million

- Cytopathology- Market Insights and Forecast 2022-2032, USD Million

- Histopathology- Market Insights and Forecast 2022-2032, USD Million

- Blood Banking & Transfusion Services- Market Insights and Forecast 2022-2032, USD Million

- Toxicology & Drug Abuse Testing- Market Insights and Forecast 2022-2032, USD Million

- Other Specialty/Esoteric Tests- Market Insights and Forecast 2022-2032, USD Million

- Clinical Chemistry- Market Insights and Forecast 2022-2032, USD Million

- By Service Provider

- Hospital-based Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Independent/Standalone Clinical Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Clinic/Physician Office Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Public Health Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Specialty Laboratories- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Routine Diagnostic Testing- Market Insights and Forecast 2022-2032, USD Million

- Chronic Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Infectious Disease Testing- Market Insights and Forecast 2022-2032, USD Million

- Oncology Testing- Market Insights and Forecast 2022-2032, USD Million

- Preventive/Screening Testing- Market Insights and Forecast 2022-2032, USD Million

- Specialized/Genetic Testing- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Test Type

- Market Size & Growth Outlook

- India Clinical Chemistry Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Hematology Testing Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Medical Microbiology Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Immunology & Serology Testing Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Molecular Diagnostics Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Genetic Testing Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Pathology Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Blood Banking & Transfusion Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Toxicology & Drug Abuse Testing Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Other Specialty/Esoteric Tests Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service Provider- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Dr Lal PathLabs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Metropolis Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agilus Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thyrocare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vijaya Diagnostic Centre

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Neuberg Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Apollo Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aarthi Scans & Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medall Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Healthians

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dr Lal PathLabs

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Test Type |

|

| By Service Provider |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.