India Butane Market Report: Trends, Growth and Forecast (2026-2032)

By Type (n-Butane, Isobutane), By Source (Natural Gas, Refining), By Application (LPG Blending, Petrochemical Feedstock (Ethylene / Butadiene production), Refineries, Refrigerants, Aerosol Propellants, Gasoline Blending), By End-Use Industry (Residential & Commercial Fuel, Automotive / Transportation, Petrochemical Industry, Food & Beverage Processing, Personal Care & Cosmetics, Industrial Manufacturing), By Packaging / Storage Format (Cylinders & Bottled Gas, Bulk Tanks, Cartridge / Canisters (Portable Butane), Aerosol Cans), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Butane Market Statistics and Insights, 2026

- Market Size Statistics

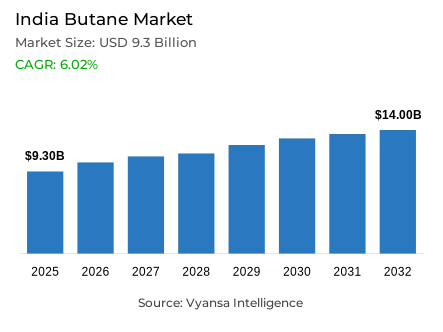

- Butane market size in India was valued at USD 9.3 billion in 2025 and is estimated at USD 10.1 Billion in 2026.

- The market size is expected to grow to USD 14 billion by 2032.

- Market to register a CAGR of around 6.02% during 2026-32.

- Type Shares

- N-butane grabbed market share of 60%.

- Competition

- More than 10 companies are actively engaged in producing butane in India.

- Top 5 companies acquired around 70% of the market share.

- Shell India / Shell plc, SUPERGAS (SHV Energy), Aegis Logistics Ltd., Indian Oil Corporation Ltd., Bharat Petroleum Corporation Ltd. etc., are few of the top companies.

- Application

- Lpg blending grabbed 45% of the market.

India Butane Market Outlook

The India Butane Market was valued at USD 9.3 billion in 2025 and is projected to grow from USD 10.1 billion in 2026 to USD 14 billion by 2032, reflecting a CAGR of 6.02% during the forecast period. The growth of the market is also closely associated with the development of the domestic LPG ecosystem in India, where butane is still a significant blending factor in domestic cooking fuel. The Petroleum Planning and Analysis Cell (PPAC) indicated that as of 1 April 2025, 329.7 million active domestic LPG end user were served by the public sector oil marketing companies (OMCs), which indicates the high and steady consumption base that underpins the demand of butane.

The LPG network is still growing thus enhancing the fundamentals of demand in blending inputs like butane. According to PPAC, PSU OMCs have added 43.6 lakh new domestic LPG end user in FY 2024-25, and the Pradhan Mantri Ujjwala Yojana (PMUY) programme has reached approximately 103.3 million beneficiaries as of 1 April 2025. This growing clean-cooking system grounds butane demand in domestic energy consumption in India.

Within the product landscape, n‑Butane accounts for 60% of the market, reflecting its suitability for large‑scale fuel blending and mainstream downstream applications. Its wide commercial acceptance makes it the most common type of butane in the LPG value chain in India.

From an application perspective, LPG Blending holds 45% of the market, underscoring its central role in butane consumption. The leadership of the segment indicates the tight coordination between the supply of butane and the domestic LPG distribution system of the country. With the growth in infrastructure capacity and the growth in petrochemical investments, the India butane market will continue to grow steadily but slowly diversify into other industrial uses.

India Butane Market Growth Driver

Expanding Household LPG Reach Supports Base Demand

The growth of the domestic LPG ecosystem in India remains a key driver of butane demand. Butane and propane are both widely used as blending inputs in LPG supply chains, thus making the size of the domestic LPG consumer base a critical factor in determining market stability. As more and more households are getting access to LPG connections, the demand of blending components like butane increases accordingly.

The Petroleum Planning and Analysis Cell (PPAC) estimates that there are 329.7 million active domestic LPG end user of the public sector oil marketing companies as of 1 April 2025. The consumption base is expanding with the addition of new end user and clean-cooking programs. According to PPAC, PSU OMCs have 4.36 million new domestic LPG end user in FY 2024-25 and the Pradhan Mantri Ujjwala Yojana (PMUY) coverage stood at approximately 103.3 million beneficiaries as of 1 April 2025. This consistent growth of the LPG consumer base helps to sustain the demand of LPG blending inputs hence providing a stable consumption base of the India butane market.

India Butane Market Challenge

High Affordability Sensitivity Keeps Pricing Policy-Linked

The butane market faces a structural challenge in the form of pricing sensitivity in the household LPG sector in India. The affordability of LPG is still closely linked to the government policy support, which affects the pricing dynamics throughout the whole value chain, including the upstream blending inputs like butane.

The magnitude of this support is supported by government policy measures. A specific subsidy of 300 per 14.2 kg LPG cylinder on up to nine refills in FY 2025-26 has been approved by the Union Cabinet with a total fiscal outlay of 120 billion. This shows that a large percentage of LPG use is still underpinned by policy processes and not necessarily by market-based pricing. The consumer base supported is also large. The PMUY programme has an estimated 103.3 million beneficiaries as of 1 July 2025 (PPAC). Due to the strong association between butane and domestic LPG supply chains, the demand and pricing dynamics of the product are still affected by the affordability factor and the government subsidy framework.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Butane Market Trend

Stronger LPG Infrastructure and Throughput Build Momentum

The market trends that are defining the India butane market is the reinforcement of LPG supply infrastructure and the increasing throughput volumes in the national distribution system. The supply chain of blending components like butane also grows in operation as the demand of LPG grows.

According to PPAC, PSU OMCs sold nearly 7.7 MMT of LPG during Q1 FY 2025–26, representing an 8.8% growth compared with Q1 FY 2024–25, while packed domestic LPG consumption increased by 8.0% during the same period. The capacity of infrastructure also keeps growing. By 1 July 2025, PSU OMCs had 213 LPG bottling plants with a rated bottling capacity of about 23.05 MMTPA, and total gross LPG tankage of 1423.0 TMT. These enhancements reinforce storage, handling, and distribution functions along the LPG value chain, which facilitates a more effective flow of blending inputs like butane across India.

India Butane Market Opportunity

Petrochemical Integration Opens Higher-Value Use Cases

The growth of the petrochemical industry in India is a new opportunity of butane other than in the LPG blending. Light hydrocarbon streams like C4 components can be processed by petrochemical complexes, thus providing more demand channels to butane in chemical manufacturing.

The major advancement that has led to this opportunity is the memorandum of understanding between IndianOil and Government of Odisha in April 2025 to construct a 6.11 billion petrochemical complex at Paradip. IndianOil also suggests that this project will be accompanied by further investments in pipelines and distribution infrastructure. During the manufacture of chemicals like propylene, petrochemical processing plants usually separate butane and heavier hydrocarbons in the cracked LPG streams. With the development of new petrochemical assets, the industry is achieving wider capability to transform C4 streams into more valuable products, allowing the India butane market to diversify gradually beyond traditional LPG blending uses.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Butane Market Segmentation Analysis

By Type

- n-Butane

- Isobutane

The segment with the highest share under Product Type is n‑Butane, accounting for approximately 60% of the market. This leadership is indicative of the extensive application of n-butane in fuel blending and mainstream downstream industrial applications.

n-butane is the type of product of choice since it can be easily incorporated into large-volume fuel supply chains, especially in LPG blending systems to supply domestic cooking fuel in India. Its high share is also indicative of the industry practice where suppliers and buyers are dependent on a stream of products that can be easily used in the current infrastructure and processing systems. The prevalence of n-Butane thus points to the fact that the market is still focused on the high-volume, practical consumption as opposed to specialised or niche applications.

By Application

- LPG Blending

- Petrochemical Feedstock (Ethylene / Butadiene production)

- Refineries

- Refrigerants

- Aerosol Propellants

- Gasoline Blending

Under Application, LPG Blending accounts for roughly 45% of the market. This segment is the biggest source of butane consumption since LPG blending is the fundamental application in the Indian domestic fuel supply system.

The management of this segment indicates the direct connection between the supply of butane and the large LPG distribution network in the country to households and commercial users. Since the use of LPG is a regular activity in cooking and heating, the demand of blending inputs is stable and predictable. This repetitive energy consumption keeps LPG blending as the main demand centre in the butane market. Therefore, the application structure is still pegged on the core energy consumption as opposed to minor specialty applications, which supports the idea of LPG blending as the core segment in the India butane market.

List of Companies Covered in India Butane Market

The companies listed below are highly influential in the India butane market, with a significant market share and a strong impact on industry developments.

- Shell India / Shell plc

- SUPERGAS (SHV Energy)

- Aegis Logistics Ltd.

- Indian Oil Corporation Ltd.

- Bharat Petroleum Corporation Ltd.

- Hindustan Petroleum Corporation Ltd.

- Reliance Petroleum Ltd.

- TotalEnergies SE

- Jyothi Gas Pvt. Ltd.

- Eastern Gases Ltd.

Market News & Updates

- Bharat Petroleum Corporation Ltd., 2026:

BPCL launched Bharatgas Lite in January 2026, a next-generation LPG cylinder made from advanced composite material for Indian households. This is highly relevant to the India butane market because butane is a core component of LPG blending, and lighter composite-cylinder innovation can improve handling, safety perception, and household adoption in packaged fuel distribution.

- SUPERGAS (SHV Energy), 2026:

SUPERGAS inaugurated a new Coimbatore filling plant in 2025 with over 51,000 MT annual capacity, automated carousel cylinder handling, and future-ready expansion design. This is an important market development because it expands LPG filling infrastructure in India, strengthens regional distribution efficiency, and supports rising packaged-gas demand across commercial and industrial applications where butane-blended LPG remains important.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Butane Market Policies, Regulations, and Standards

- India Butane Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Butane Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- n-Butane- Market Insights and Forecast 2022-2032, USD Million

- Isobutane- Market Insights and Forecast 2022-2032, USD Million

- By Source

- Natural Gas- Market Insights and Forecast 2022-2032, USD Million

- Refining- Market Insights and Forecast 2022-2032, USD Million

- By Application

- LPG Blending- Market Insights and Forecast 2022-2032, USD Million

- Petrochemical Feedstock (Ethylene / Butadiene production)- Market Insights and Forecast 2022-2032, USD Million

- Refineries- Market Insights and Forecast 2022-2032, USD Million

- Refrigerants- Market Insights and Forecast 2022-2032, USD Million

- Aerosol Propellants- Market Insights and Forecast 2022-2032, USD Million

- Gasoline Blending- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry

- Residential & Commercial Fuel- Market Insights and Forecast 2022-2032, USD Million

- Automotive / Transportation- Market Insights and Forecast 2022-2032, USD Million

- Petrochemical Industry- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage Processing- Market Insights and Forecast 2022-2032, USD Million

- Personal Care & Cosmetics- Market Insights and Forecast 2022-2032, USD Million

- Industrial Manufacturing - Market Insights and Forecast 2022-2032, USD Million

- By Packaging / Storage Format

- Cylinders & Bottled Gas- Market Insights and Forecast 2022-2032, USD Million

- Bulk Tanks- Market Insights and Forecast 2022-2032, USD Million

- Cartridge / Canisters (Portable Butane)- Market Insights and Forecast 2022-2032, USD Million

- Aerosol Cans- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- India n-Butane Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Packaging / Storage Format- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Isobutane Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Source- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Packaging / Storage Format- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Indian Oil Corporation Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bharat Petroleum Corporation Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hindustan Petroleum Corporation Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reliance Petroleum Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TotalEnergies SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shell India / Shell plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SUPERGAS (SHV Energy)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aegis Logistics Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jyothi Gas Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eastern Gases Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Indian Oil Corporation Ltd.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Source |

|

| By Application |

|

| By End-Use Industry |

|

| By Packaging / Storage Format |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.