India Ayurvedic Products Market Report: Trends, Growth and Forecast (2026-2032)

By Product Category (Healthcare Products (Classical Medicines, Proprietary/OTC Medicines, Nutraceuticals & Dietary Supplements), Personal Care Products (Skin Care, Hair Care, Oral Care, Others)), By Formulation Type (Herbal, Mineral Preparations, Herbomineral Preparations), By Form (Tablets & Capsules, Powders, Juices & Syrups, Oils & Ointments, Others), By Distribution Channel (Retail Offline (Pharmacies & Drug Stores, Ayurveda Stores, Supermarkets/Hypermarkets, Convenience Stores), Retail Online (E-commerce Marketplaces, Brand-owned Websites/D2C Platforms)), By Indication (GI Tract (Gastrointestinal), Infectious Diseases, Skin & Hair, Respiratory System, Nervous System, Cardiovascular System, Reproductive System, Others), By End User (Individuals / Households, Hospitals & Clinics, Wellness Centers & Ayurvedic Clinics, Others), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Ayurvedic Products Market Statistics and Insights, 2026

- Market Size Statistics

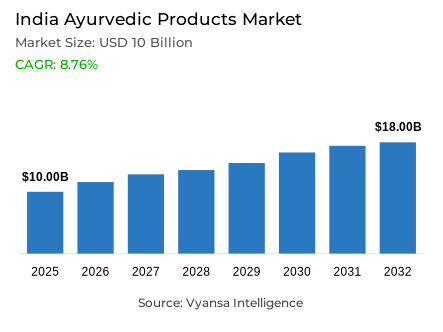

- Ayurvedic products market size in India was valued at USD 10 billion in 2025 and is estimated at USD 11.5 billion in 2026.

- The market size is expected to grow to USD 18 billion by 2032.

- Market to register a CAGR of around 8.76% during 2026-32.

- Product Category Shares

- Healthcare products grabbed market share of 60%.

- Competition

- More than 10 companies are actively engaged in producing ayurvedic products in India.

- Top 5 companies acquired around 55% of the market share.

- Vicco Laboratories, Amrutanjan Healthcare Ltd., Hamdard Laboratories (India), Dabur India Ltd., Patanjali Ayurved Ltd. etc., are few of the top companies.

- Formulation Type

- Herbal grabbed 70% of the market.

India Ayurvedic Products Market Outlook

India ayurvedic products market is estimated to be USD 10 billion in 2025 and it is projected to be around USD 11.5 billion in 2026 and USD 18 billion by 2032 with the CAGR of 8.76%. The growing confidence in ayurvedic medical products and growing disposable income of urban and semi-urban families, and the apparent trend toward preventive health care as opposed to reactive treatment are all adding to a demand base that is not spiking but growing steadily.

Herbal formulations make up around 70% of total market composition, and healthcare products account for close to 60% of category share. Taken together, those figures confirm that this is a market oriented around functional health outcomes, not lifestyle aesthetics. Manufacturers have responded by directing investment into phytochemical standardization and bioavailability research, pushing product quality upward and giving brands more defensible ground to compete on beyond price. Average realized value per product is edging up as a result, not in dramatic jumps, but consistently enough to improve margins across the category.

Urban end user, particularly in the post-pandemic period, are actively seeking healthcare alternatives outside the synthetic pharmaceutical mainstream, and ayurvedic products have captured a meaningful share of that redirected attention. What gives this more staying power than a typical wellness cycle is the institutional infrastructure operating behind it. Over approximately USD 1,880 USD Ayushman Arogya Mandirs are now operational, with more than 57.9 million wellness sessions delivered through them, normalizing Ayurvedic consumption across income groups and converting occasional users into repeat buyers over time. That loyalty depth is what supports premium pricing strategies at scale.

Regulatory developments have changed the competitive picture materially, and brands need to be clear-eyed about what that means going forward. The Ayush Quality Mark launched in December 2025 and India's collaboration with the WHO on a Traditional Medicine classification module are not cosmetic developments. Both signal a real push toward globally aligned quality standards that will increasingly define who can compete credibly across domestic and international markets. Brands with documentation and quality infrastructure already in place are reasonably well positioned for what follows, and on the export front, AYUSH revenues rising 6.11% to USD 688.89 million in 2024-25 confirms that international demand is real and extends the competitive playing field well beyond domestic boundaries through 2032.

India Ayurvedic Products Market Growth DriverGovernment-Catalyzed Preventive Healthcare Expansion

The long-term government investment in AYUSH-led healthcare is one of the main structural drivers, which entails institutional demand creation on a large scale within the Indian wellness ecosystem. The tactical use of state resources in the form of preventive health infrastructure triggers the growth of awareness, the availability of services, and the uptake of products by demographic groups that were previously not part of the official Ayurvedic consumption market. This policy pledge will turn Ayurveda into a non-discretionary wellness choice, essentially broadening the consumer universe that can be addressed.

The quantitative aspects of this driver highlight its importance in the market with accuracy. The 2025-26 Union Budget has allocated approximately USD 475 million to the Ministry of Ayush, and the National AYUSH Mission alone is allocated approximately USD 152 million. The operational delivery infrastructure has increased to 1,78,154 Ayushman Arogya Mandirs, where 57.9 million wellness sessions have been administered by August 2025. These indicators confirm the level of institutional engagement and the extent of ground-level demand mobilization, establishing sustainable demand tailwinds of ayurvedic products by 2032.

India Ayurvedic Products Market ChallengeRegulatory Tightening and Credibility Imperatives

The compliance climate is becoming stricter and the pressure of adjustment is not distributed evenly. Brands that have good documentation, clinical support, and well-organized claims management are in a better position to withstand greater regulatory attention, whereas smaller players that have built their claims architecture on thinner evidence and looser promotional language will find it more difficult to withstand exposure, reputational and legal, to anyone who has not taken the time to get their claims architecture in order. Beyond operational compliance, the issue goes further into the way product benefits are conveyed and whether the evidence behind those conveyances is of an increasing standard of expectation by both regulators and end user.

The enforcement infrastructure being built out gives a clear sense of how serious this shift is. Launched on 30 May 2025, the Ayush Suraksha portal gives regulators and end user a direct channel for flagging misleading advertisements and adverse drug reaction reports, while the pharmacovigilance network operates through 1 national centre, 5 intermediary centres, and 97 peripheral centres. Public notices on ASU&H drugs are being disseminated through 100 leading newspapers in Hindi, English, and regional languages, which means compliance failures now carry broad public visibility. Brands that treat this period as an opportunity to build genuine evidence infrastructure will come out of it with a measurable trust advantage over those treating compliance as a minimum threshold to clear.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ayurvedic Products Market TrendStandardisation and Global Quality Alignment

Ayurveda's integration into internationally recognized healthcare classification frameworks is no longer a future ambition. It is actively underway, and the commercial implications are significant for any brand thinking seriously about international market access. For a long time, the absence of shared quality language that a foreign buyer or regulator could recognize and verify against kept many export pathways effectively closed, and the shift toward standardized, evidence-supported positioning is what changes that access equation in a practical way.

On 24 May 2025, India and the WHO began collaborative development of a Traditional Medicine module under the International Classification of Health Interventions, placing Ayurvedic interventions inside a globally standardized terminology structure. The Ayush Quality Mark, launched on 19 December 2025 at the Second WHO Global Summit on Traditional Medicine, creates an internationally aligned quality assurance framework for AYUSH products and services. Taken together, these developments raise the baseline for credible market participation and draw a progressively clearer line between brands with genuine standardization capability and those still operating as undocumented commodity players, a distinction that will carry real commercial weight through 2032.

India Ayurvedic Products Market OpportunityExport-Led Expansion and International Market Penetration

International demand for traditional and natural healthcare is generating real commercial pull for Indian Ayurvedic brands, particularly among end user in markets where skepticism toward synthetic healthcare interventions is growing. The economics favor brands that can combine a credible heritage narrative with clinical documentation and internationally recognized quality credentials. Pursuing export revenue also offers something beyond income diversification, since a visible international presence tends to reinforce premium positioning in the domestic market as well.

AYUSH and herbal product exports grew 6.11% to USD 688.89 million in 2024-25, up from USD 649.2 million in the prior year. The institutional architecture supporting that growth has expanded considerably, encompassing 25 country-to-country MoUs, 15 MoUs for AYUSH Academic Chairs, and 43 Ayush Information Cells operating across 39 foreign nations. That diplomatic and trade network reduces market-entry friction and gives compliant exporters structured visibility in target markets. Brands that align product development and documentation practices with international standards are positioned to capture a disproportionate share of this opportunity through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Ayurvedic Products Market Segmentation Analysis

By Product Category

- Healthcare Products

- Classical Medicines

- Proprietary/OTC Medicines

- Nutraceuticals & Dietary Supplements

- Personal Care Products

- Skin Care

- Hair Care

- Oral Care

- Others

The segment with highest market share under Product Category is Healthcare products account for approximately 60% of the total market, the dominant category and by a considerable margin. That share concentration reflects where consumer purchase intent is most durably anchored: functional outcomes, therapeutic relief, and preventive care. Healthcare products generate the highest transaction volumes, the strongest repeat purchase rates, and attract the most consistent channel investment across the competitive landscape, dynamics that collectively reinforce the category's lead over other product segments in a way that is unlikely to shift substantially in the near term.

As regulatory expectations around clinical validation become more explicit, the healthcare products category is likely to attract even greater R&D investment from both incumbents and new entrants. Formulation pipelines are gravitating toward health-centric outcomes because that is where price premiums are most defensible and where regulatory credibility delivers the most direct commercial payoff. The concentration of competitive energy within this segment is expected to deepen its market share leadership through 2032.

By Formulation Type

- Herbal

- Mineral Preparations

- Herbomineral Preparations

The segment with highest market share under Formulation Type is Herbal formulations account for roughly 70% of total market, placing more than two-thirds of the entire industry within a single formulation type. That degree of concentration reflects decades of consumer preference for plant-based, phytochemically derived solutions, supported by manufacturing infrastructure and raw material supply chains built specifically around herbal product development over a long period. The foundation underpinning this dominance is resistant to disruption from shifts in consumer trend or competitive entry, largely because it has been built up over time rather than assembled quickly around a market trend.

Cultural legitimacy, growing clinical documentation, and rising global demand for nature-derived wellness products collectively sustain the segment's commercial position. A well-established raw material ecosystem enables scalable production across price points, keeping the segment accessible at the mass end while still supporting premium positioning at the top. As international quality benchmarks tighten, herbal manufacturers with serious quality assurance capabilities will be better placed to compete across both domestic and export markets, and the ongoing expansion of bilateral trade agreements and export infrastructure adds further upside to the segment's long-term commercial potential through 2032.

List of Companies Covered in India Ayurvedic Products Market

The companies listed below are highly influential in the India ayurvedic products market, with a significant market share and a strong impact on industry developments.

- Vicco Laboratories

- Amrutanjan Healthcare Ltd.

- Hamdard Laboratories (India)

- Dabur India Ltd.

- Patanjali Ayurved Ltd.

- Himalaya Wellness Company

- Emami Ltd. (Zandu)

- Baidyanath Group (Shree Baidyanath Ayurved Bhawan)

- Sandu Pharmaceuticals Ltd.

- The Arya Vaidya Pharmacy (Coimbatore) Ltd.

Market News & Updates

- Dabur India Ltd., 2025:

Dabur launched Siens by Dabur in June 2025 as a premium digital-first nutraceutical range spanning Beauty and Skin Health, Daily Wellness, and Gut Health. This is relevant to the India ayurvedic products market because nutraceuticals and dietary supplements are one of your key product categories, and the launch shows Dabur extending Ayurveda-linked wellness into a more modern direct-to-consumer supplement format.

- Hamdard Laboratories (India), 2025:

Hamdard’s official India website listed Ashokarishta under its “Newly Launched” range in 2025, alongside other fresh additions to its portfolio. This is a meaningful market update because it reflects continued product expansion in classical and women’s-health-focused Ayurvedic formulations, which are central to India’s healthcare and wellness-oriented Ayurveda market. The company’s official product-directory listing shows the relevant pages were updated in May 2025.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Ayurvedic Products Market Policies, Regulations, and Standards

- India Ayurvedic Products Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Ayurvedic Products Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Category

- Healthcare Products- Market Insights and Forecast 2022-2032, USD Million

- Classical Medicines- Market Insights and Forecast 2022-2032, USD Million

- Proprietary/OTC Medicines- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals & Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Personal Care Products- Market Insights and Forecast 2022-2032, USD Million

- Skin Care- Market Insights and Forecast 2022-2032, USD Million

- Hair Care- Market Insights and Forecast 2022-2032, USD Million

- Oral Care- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Healthcare Products- Market Insights and Forecast 2022-2032, USD Million

- By Formulation Type

- Herbal- Market Insights and Forecast 2022-2032, USD Million

- Mineral Preparations- Market Insights and Forecast 2022-2032, USD Million

- Herbomineral Preparations- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Tablets & Capsules- Market Insights and Forecast 2022-2032, USD Million

- Powders- Market Insights and Forecast 2022-2032, USD Million

- Juices & Syrups- Market Insights and Forecast 2022-2032, USD Million

- Oils & Ointments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies & Drug Stores- Market Insights and Forecast 2022-2032, USD Million

- Ayurveda Stores- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- Brand-owned Websites/D2C Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Indication

- GI Tract (Gastrointestinal)- Market Insights and Forecast 2022-2032, USD Million

- Infectious Diseases- Market Insights and Forecast 2022-2032, USD Million

- Skin & Hair- Market Insights and Forecast 2022-2032, USD Million

- Respiratory System- Market Insights and Forecast 2022-2032, USD Million

- Nervous System- Market Insights and Forecast 2022-2032, USD Million

- Cardiovascular System- Market Insights and Forecast 2022-2032, USD Million

- Reproductive System- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Individuals / Households- Market Insights and Forecast 2022-2032, USD Million

- Hospitals & Clinics- Market Insights and Forecast 2022-2032, USD Million

- Wellness Centers & Ayurvedic Clinics- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Category

- Market Size & Growth Outlook

- India Healthcare Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Formulation Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Indication- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Personal Care Products Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Formulation Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Indication- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Dabur India Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Patanjali Ayurved Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Himalaya Wellness Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Emami Ltd. (Zandu)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Baidyanath Group (Shree Baidyanath Ayurved Bhawan)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vicco Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amrutanjan Healthcare Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hamdard Laboratories (India)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sandu Pharmaceuticals Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Arya Vaidya Pharmacy (Coimbatore) Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dabur India Ltd.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Category |

|

| By Formulation Type |

|

| By Form |

|

| By Distribution Channel |

|

| By Indication |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.