France Sleep Aids Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Single Ingredient (Doxylamine Succinate, Diphenhydramine, Melatonin), Combination Ingredient (Diphenhydramine + Acetaminophen, Other Antihistamine-Based Combinations), Herbal & Traditional Sleep Aids (Valerian root, Passionflower, Chamomile, Kava, Multi-Herbal Sleep Blends)), By Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Sleep Walking, Others), By Age Group (Young to Mid Adults (25-44 Years), Middle-Aged Adults (45-64 Years), Geriatric Population (65+ Years)), By Sales Channel (Retail Online, Retail Offline), By End User (Homecare/Individual Consumers, Hospitals, Sleep Centers & Clinics), By Formulation (Tablets, Gummies, Capsules, Liquid, Sublingual) ... Read more

|

Major Players

|

France Sleep Aids Market Statistics and Insights, 2026

- Market Size Statistics

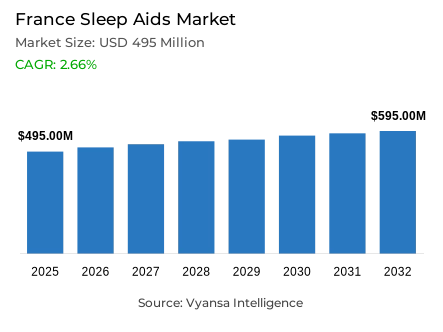

- Sleep aids market size in France was estimated at USD 495 million in 2025.

- The market size is expected to grow to USD 595 million by 2032.

- Market to register a CAGR of around 2.66% during 2026-32.

- Product Shares

- Single ingredient grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing sleep aids in France.

- Top 5 companies acquired around 25% of the market share.

- Pierre Fabre SA Laboratoires, Biocodex SAS, Coopération Pharmaceutique Française SAS (Cooper), Sanofi, Bayer Sante Familiale SAS etc., are few of the top companies.

- Sales channel

- Retail offline grabbed 70% of the market.

France Sleep Aids Market Outlook

The France sleepaids market is estimated at USD 495 million in 2025 and is projected to reach USD 595 million by 2032, reflecting a CAGR of about 2.66% during the forecast period. Growth is primarily supported by persistent stress and anxiety levels, influenced by economic uncertainty and geopolitical developments. French end users increasingly view restorative sleep as a fundamental pillar of overall wellbeing, strengthening demand for accessible and effective sleepsupport solutions that align with longterm health management goals.

A clear structural shift is underway from traditional synthetic sedatives toward natural and herbal formulations. Products containing melatonin, magnesium, and plant extracts are gaining traction due to perceptions of improved safety and reduced risk of dependency or morning drowsiness. Convenient delivery systems such as gummies are enhancing engagement, particularly among younger end users, by offering a more approachable and lifestyleoriented format compared with conventional tablets.

Competition remains intense, with strong advertising investment and continuous product innovation. Pharmacies, drugstores, and parapharmacies continue to dominate physical retail, but brands are differentiating through cleaner formulations and transparent ingredient communication. The inclusion of botanicals and wellnessaligned ingredients such as CBD supports positioning within the broader naturalhealth movement.

Looking ahead, the market may face pressure from supplychain disruptions, limited shelf space, and increasing end user fatigue due to category saturation. However, sustained interest in preventive health and personalized natural remedies is expected to underpin resilience. Brands that combine scientific validation with convenient, appealing formats will remain well positioned to capture ongoing end user focus on sleep health through 2032.

France Sleep Aids Market Growth DriverHigh Insomnia Prevalence Maintains Structural Demand

Sleep problems remain widespread in France, sustaining consistent interest in accessible sleepsupport solutions. According to Santé publique France, the average selfreported sleep duration in 2024 among adults aged 1879 was 7 hours and 32 minutes, while 21.5% of adults were classified as short sleepers six hours or less per night.

Additionally, around one third of adults report symptoms of insomnia, including difficulty falling asleep or frequent nighttime awakenings. This persistent sleep deficit supports structural demand for overthecounter supplements positioned around relaxation and faster sleep onset. As stress and anxiety remain embedded in daily routines, sleep continues to shift from a lifestyle topic to a preventative health priority, reinforcing steady category demand.

France Sleep Aids Market ChallengeSupply Disruptions Create Shelf-Level Availability Gaps

Periodic supply shortages remain a material constraint in the French sleepaid market. According to Agence nationale de sécurité du médicament (ANSM), there were 3,825 notifications of stock ruptures and supply risks in 2024, with nearly half requiring at least one corrective management measure to safeguard access.

For brands, these interruptions limit the ability to convert highintent shoppers seeking immediate relief, particularly in pharmacies where shelf space is limited. Retailers become cautious about maintaining wide assortments when replenishment is uncertain, which weakens promotional impact and reduces visibility. In a category where urgency drives purchasing decisions, supply instability directly constrains volume potential and end user trust.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Sleep Aids Market TrendGummies and Natural Positioning Rise with Safety Scrutiny

The market is shifting toward more approachable formats and softer positioning. Gummies and herbalstyle sleep aids are gaining visibility as alternatives to conventional tablets, reflecting growing concern over dependency and morning drowsiness. Natural claims and less clinical branding resonate strongly with end users seeking reassurance.

At the same time, safety oversight is becoming more prominent. In 2024, Agence nationale de sécurité sanitaire de l’alimentation (Anses) recorded 478 nutrivigilance declarations, of which 5.6% were classified as severe among analysable cases. Anses also issued an opinion regarding a serious case linked to Novanuit Triple Action, reinforcing scrutiny around ingredient combinations such as melatonin and plant extracts. This environment encourages brands to combine appealing formats like gummies with clearer dosage guidance and responsible communication.

France Sleep Aids Market OpportunityDigital Commerce Expands Multi-Format Reach

Online purchasing behavior is now mainstream in France, creating strong scalability opportunities for sleepaid brands. According to Institut national de la statistique et des études économiques (Insee), 72.9% of individuals aged 15+ made an online purchase within the past twelve months in 2025, while 63.6% purchased online within the past three months.

Digital channels allow broader assortment across formats such as gummies, oils, tablets, and herbal blends, while also supporting ingredient education and responsibleuse messaging. end users benefit from discreet purchasing and the ability to compare magnesium, melatonin, or plantbased formulations. As pharmacy Retail online and marketplace listings expand, online retail will remain a central lever for category penetration and premium multiformat innovation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Sleep Aids Market Segmentation Analysis

By Product

- Single Ingredient

- Combination Ingredient

- Herbal & Traditional Sleep Aids

The France sleepaids market is led by the singleingredient segment, which accounts for about 45% of total market value. This dominance reflects the strong end user preference for familiar, clearly positioned solutions, particularly melatoninbased products that are perceived as fastacting and dependable for managing sleep latency.

Singleingredient formulations serve as the primary entry point for many end users beginning their sleephealth journey. Their simplicity, transparent dosing, and straightforward communication strengthen trust and repeat purchase. While multiingredient blends are gradually expanding to address broader sleep concerns such as relaxation and nighttime awakenings, singleingredient products remain the structural backbone of the market due to their clarity, accessibility, and established brand positioning.

By Sales Channel

- Retail Online

- Retail Offline

The France sleepaids market is dominated by the retail offline segment, which holds approximately 70% of total sales. This leadership is rooted in France longstanding reliance on pharmacies, drugstores, and parapharmacies as trusted sources of health and wellness guidance.

Physical retail outlets offer more than product availability; they provide pharmacist consultation and professional reassurance, which are highly valued in a category linked to health and sleep quality. Although Retail online is expanding and improving accessibility, instore purchasing remains preferred due to personalized advice and immediate availability. The extensive pharmacy network continues to drive strong brand visibility, end user trust, and conversion, reinforcing retail offline as the core sales pillar.

List of Companies Covered in France Sleep Aids Market

The companies listed below are highly influential in the France sleep aids market, with a significant market share and a strong impact on industry developments.

- Pierre Fabre SA Laboratoires

- Biocodex SAS

- Coopération Pharmaceutique Française SAS (Cooper)

- Sanofi

- Bayer Sante Familiale SAS

- Jolly-Jattel SARL

- Laboratoires Arkopharma SA

- Vemedia Consumer Health France SAS

- Pileje SAS

- UPSA Laboratoires

Competitive Landscape

France sleep aids market is led by Sanofi’s Novanuit, which sustains category leadership through aggressive consumer marketing and melatonin-based, multi-action formulations, while Bayer’s Euphytose Nuit and Laboratoires Forté Pharma compete with extended-release and gummy variants. Laboratoires Arkopharma differentiates via Arkorelax, aligning with rising demand for herbal, non-habit-forming solutions, reflecting a broader shift from traditional sedatives such as Donormyl toward natural positioning. Gummies represent a key battleground, driving format premiumisation and brand visibility. Indirect competition is intensifying from vitamins and dietary supplements, notably magnesium and plant-based blends promoted via social media, as well as stabilising CBD offerings. Differentiation opportunities lie in low-dosage melatonin compliance, sea magnesium and CBD integration, clinically substantiated herbal blends, and compact, pharmacy-optimised packaging that mitigates shelf-space and over-promotion pressures.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- France Sleep Aids Market Policies, Regulations, and Standards

- France Sleep Aids Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- France Sleep Aids Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Doxylamine Succinate- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine- Market Insights and Forecast 2022-2032, USD Million

- Melatonin- Market Insights and Forecast 2022-2032, USD Million

- Combination Ingredient- Market Insights and Forecast 2022-2032, USD Million

- Diphenhydramine + Acetaminophen- Market Insights and Forecast 2022-2032, USD Million

- Other Antihistamine-Based Combinations- Market Insights and Forecast 2022-2032, USD Million

- Herbal & Traditional Sleep Aids- Market Insights and Forecast 2022-2032, USD Million

- Valerian root- Market Insights and Forecast 2022-2032, USD Million

- Passionflower- Market Insights and Forecast 2022-2032, USD Million

- Chamomile- Market Insights and Forecast 2022-2032, USD Million

- Kava- Market Insights and Forecast 2022-2032, USD Million

- Multi-Herbal Sleep Blends- Market Insights and Forecast 2022-2032, USD Million

- Single Ingredient- Market Insights and Forecast 2022-2032, USD Million

- By Sleep Disorder

- Insomnia- Market Insights and Forecast 2022-2032, USD Million

- Sleep Apnea- Market Insights and Forecast 2022-2032, USD Million

- Restless Legs Syndrome- Market Insights and Forecast 2022-2032, USD Million

- Narcolepsy- Market Insights and Forecast 2022-2032, USD Million

- Sleep Walking- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Young to Mid Adults (25-44 Years)- Market Insights and Forecast 2022-2032, USD Million

- Middle-Aged Adults (45-64 Years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric Population (65+ Years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Homecare/Individual Consumers- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Sleep Centers & Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Formulation

- Tablets- Market Insights and Forecast 2022-2032, USD Million

- Gummies- Market Insights and Forecast 2022-2032, USD Million

- Capsules- Market Insights and Forecast 2022-2032, USD Million

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Sublingual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- France Single Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Combination Ingredient Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Herbal & Traditional Sleep Aids Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sleep Disorder- Market Insights and Forecast 2022-2032, USD Million

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Formulation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Sanofi

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Sante Familiale SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jolly-Jattel SARL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoires Arkopharma SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vemedia Consumer Health France SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pierre Fabre SA Laboratoires

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Biocodex SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coopération Pharmaceutique Française SAS (Cooper)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pileje SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UPSA Laboratoires

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sleep Disorder |

|

| By Age Group |

|

| By Sales Channel |

|

| By End User |

|

| By Formulation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.