Global Cloud ITSM Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solutions, ITSM Platform Solutions, IT Visibility & Control Solutions, Intelligent Automation Solutions, Services, Consulting & Deployment Services, Integration & Migration Services, Support & Managed Services), By Deployment (Public Cloud, Private Cloud, Hybrid Cloud), By Enterprise Size (Large Enterprises, SMEs), By End User (BFSI, IT & Telecom, Healthcare, Retail & E-commerce, Manufacturing, Government & Public Sector, Others), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Cloud ITSM Market Statistics and Insights, 2026

- Market Size Statistics

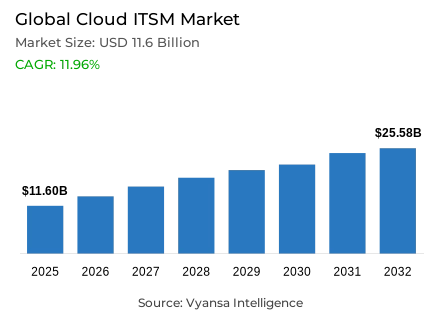

- Cloud itsm market size in Global was valued at USD 11.6 billion in 2025 and is estimated at USD 13 Billion in 2026.

- The market size is expected to grow to USD 25.58 billion by 2032.

- Market to register a CAGR of around 11.96% during 2026-32.

- Component Shares

- Solutions grabbed market share of 75%.

- Competition

- More than 30 companies are actively engaged in producing cloud itsm.

- Top 5 companies acquired around 25% of the market share.

- Zoho Corporation (ManageEngine), Freshworks, OpenText, ServiceNow, Atlassian etc., are few of the top companies.

- Deployment

- Public cloud grabbed 50% of the market.

- Region

- North America leads with a 40% share of the global market.

Global Cloud ITSM Market Outlook

The Global Cloud ITSM Market was valued at USD 11.6 billion in 2025, establishing a commercially resilient and structurally well-supported foundation within the world's rapidly evolving enterprise technology ecosystem. Projected to advance from USD 13 billion in 2026 to USD 25.58 billion by 2032, the sector registers a compound annual growth rate of 11.96% across the forecast horizon. This near-doubling of market value reflects the systematic migration of IT service operations from legacy, on-premise support structures toward integrated cloud platforms. Organizations worldwide are prioritizing service delivery improvement, workflow automation, and operational visibility as core digital transformation objectives. Growth is anchored in genuine modernization necessity rather than technology cycle enthusiasm, giving this market strong commercial resilience across diverse industry verticals and geographic contexts.

The component architecture defining this market's commercial structure is anchored firmly in integrated platform offerings. Solutions command approximately 75% of total component market share, reflecting the consistent organizational preference for unified service management platforms. These platforms consolidate incident handling, request management, asset visibility, and workflow automation within a single deployment framework. Eurostat's documentation that 52.7% of EU enterprises used paid cloud computing services in 2025, up by 7.4 percentage points from 2023, validates the cloud adoption momentum that is expanding the organizational base requiring structured service management. ITU's confirmation that 6 billion people, representing 74% of the global population, are using the internet in 2025 further confirms the digital engagement scale that sustains consistent cloud ITSM adoption pressure across enterprise environments worldwide.

The deployment architecture reinforces the structural primacy of public cloud as the category's dominant infrastructure preference. Public Cloud commands approximately 50% of total deployment model market share, reflecting the organizational preference for faster implementation timelines, lower infrastructure ownership burden, and more flexible scaling across distributed service teams. This concentration confirms that global enterprises have moved past the exploratory phase of cloud adoption and are now making long-cycle platform investment decisions based on operational performance, integration capability, and total service economics. The Cyber Solidarity Act entering into force on 4 February 2025 simultaneously signals a regulatory maturation that is elevating governance expectations for cloud service management deployments across major markets.

The forward outlook through 2032 is defined by four structural forces operating in sustained convergence. The rise of AI integration across enterprise operations, confirmed by Eurostat's documentation of 20.0% of EU enterprises with at least 10 employees using AI technologies in 2025, is progressively redefining platform capability expectations within cloud ITSM procurement evaluations. ENISA's Threat Landscape 2025 analysis of 4,875 cybersecurity incidents between July 2024 and June 2025 sustains the security governance scrutiny that shapes cloud platform adoption decisions across security-sensitive buyer segments. The World Bank's documentation that less than 20% of low and middle-income countries possess modern data infrastructure confirms a globally significant untapped adoption opportunity. North America's 40% global market share leadership establishes the commercial center of gravity around which competitive strategy and product development investments are organized iver the forecast period.

Global Cloud ITSM Market Growth Driver

Rising Enterprise Cloud Adoption Expands the Structural Cloud ITSM Demand Base

The rapid and institutionally documented expansion of paid cloud computing service adoption across global enterprises represents the primary structural driver of cloud ITSM demand. This adoption wave functions as a persistent organizational complexity mechanism that continuously expands the scale and sophistication of IT service management requirements across enterprise environments worldwide. As organizations transition core business processes into cloud environments, the operational requirements for centralized incident management, structured workflow coordination, change governance, and service visibility scale in direct proportion to the breadth and complexity of each organization's cloud workload portfolio. This cloud adoption-driven demand dynamic creates a self-reinforcing growth mechanism whose commercial implications for cloud ITSM platform investment are direct, measurable, and structurally compounding across the forecast horizon.

The quantitative momentum of this cloud adoption-driven demand dynamic is documented with precision by Eurostat and ITU. A total of 52.7% of EU enterprises used paid cloud computing services in 2025, up by 7.4 percentage points from 2023, confirming that enterprise cloud adoption is advancing at a pace that consistently expands the organizational base requiring structured cloud service management capabilities. ITU's confirmation of 6 billion internet users in 2025, representing 74% of the world's population, establishes the global digital engagement scale that sustains consistent cloud ITSM adoption pressure across diverse industry verticals and geographic markets. These overlapping cloud adoption metrics confirm a demand expansion dynamic of sufficient global scale and continuity to sustain structural cloud ITSM market growth over the forecast period.

Global Cloud ITSM Market Challenge

Cybersecurity Threats and Compliance Obligations Constrain Adoption Confidence

The rapidly escalating cybersecurity threat environment and progressively more demanding compliance obligations surrounding cloud-based service management deployments represent the most consequential structural challenge confronting the global cloud ITSM market. These pressures create systematic security governance, incident response, and regulatory compliance burdens that moderate adoption velocity and introduce procurement complexity into cloud ITSM deployment decisions across security-sensitive enterprise and public-sector buyer segments. In a market where cloud ITSM platforms sit at the intersection of user access management, workflow records, and business-critical support processes, the security implications of inadequate configuration governance and weak identity controls are directly material to organizational risk profiles across every major buyer segment.

The structural depth and institutional specificity of this cybersecurity challenge are quantified with precision by ENISA and the European Commission. ENISA's Threat Landscape 2025 analyses 4,875 cybersecurity incidents recorded between 1 July 2024 and 30 June 2025, confirming that threat activity remains significant and persistent across connected enterprise environments where cloud ITSM platforms are increasingly deployed. The Cyber Solidarity Act entered into force on 4 February 2025 to improve preparedness, detection, and response to cybersecurity incidents across the EU, confirming that regulatory compliance obligations for cloud service management users are expanding in scope and enforcement specificity simultaneously. For cloud ITSM providers, navigating this threat and compliance environment demands sustained investment in security-by-design platform architecture, configuration governance tooling, and compliance documentation capability over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Cloud ITSM Market Trend

AI Integration Reshapes Cloud ITSM Platform Capability Expectations

The accelerating integration of artificial intelligence into enterprise service operations represents the defining structural trend reshaping the global cloud ITSM market. This AI adoption wave is fundamentally elevating organizational expectations for automation depth, predictive incident management, intelligent ticket routing, and proactive workflow optimization within cloud service management platform evaluations. The trend is moving the competitive differentiation axis beyond traditional service desk functionality and workflow control into the domain of intelligent automation, real-time anomaly detection, and AI-enhanced service experience design. These dimensions are progressively redefining what organizations consider baseline platform capability versus advanced feature differentiation in cloud ITSM procurement decisions across enterprise markets worldwide.

The institutional scale and organizational specificity of this AI integration trend are documented with precision by Eurostat. A total of 20.0% of EU enterprises with at least 10 employees used AI technologies in 2025, up from 13.5% in 2024, confirming that enterprise AI adoption is advancing at a pace that is progressively embedding intelligent automation expectations within cloud ITSM platform evaluations across a growing share of the European enterprise buyer population. The concentration of AI adoption among large enterprises is particularly commercially significant: 55.03% of large EU enterprises used AI technologies in 2025, confirming that the most complex and highest-value cloud ITSM buyer segments are already operationalizing AI across their digital service environments. As AI-augmented service capabilities transition from premium add-ons into expected platform features, providers with deep automation integration will capture disproportionate enterprise platform investment over the forecast period.

Global Cloud ITSM Market Opportunity

Underserved Digital Economies Create a Globally Significant Untapped Adoption Frontier

The large and structurally underserved digital infrastructure base across low and middle-income economies represents the global cloud ITSM market's most commercially significant long-term growth opportunity. Rising demand for structured service management, cloud application support, and digital workflow governance is confronting a critical shortage of modern IT service management platforms across markets where cloud adoption is accelerating but institutional service management maturity remains in its early stages. This emerging market adoption frontier is distinguished from mature market replacement demand by its scale, geographic breadth, and the structural advantage that cloud-native ITSM platforms hold in deployment contexts where rapid implementation, lower infrastructure dependency, and accessible cost structures are primary procurement criteria.

The quantitative scale and accessibility of this emerging market opportunity are documented with precision by the World Bank. Less than 20% of low and middle-income countries currently possess modern data infrastructure, confirming a structural digital capability gap of global geographic breadth whose commercial closure will require structured service management platforms capable of supporting first-time cloud adoption journeys across organizationally diverse and resource-constrained deployment contexts. The World Bank further documents that low-income countries have zero cloud on-ramps, while cloud resources are progressively moving closer to the edge to improve performance and accessibility for previously underserved markets. Cloud ITSM providers that develop platform offerings specifically engineered for emerging market deployment contexts, combining accessible cost structures, simplified implementation requirements, and scalable service governance frameworks, will capture disproportionate value from this structurally significant and geographically expansive growth opportunity over the forecast period.

Global Cloud ITSM Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

The segment with highest market share under the Region is North America, accounting for approximately 40% of the total market. This dominant regional position reflects the convergence of the world's largest enterprise technology investment base, the highest concentration of cloud-native organizational environments, and the most sophisticated IT service management procurement ecosystems across any global region. North America's 40% global share confirms its structural centrality to the cloud ITSM industry's commercial performance, competitive dynamics, and product development direction. The region's combination of mature enterprise cloud adoption, active digital modernization programs, and a regulatory environment that supports cloud platform innovation creates a uniquely favorable commercial environment for cloud ITSM platform adoption across both private enterprise and public-sector buyer segments.

The structural dominance of North America is sustained by demand characteristics operating simultaneously across multiple commercial dimensions. Active platform replacement and upgrade cycles among established cloud ITSM users in mature markets are generating consistent renewal and expansion revenue. Rapid first-time adoption momentum among mid-market organizations transitioning from legacy service management tools is expanding the total buyer population. The US federal government's documented annual IT investment exceeding USD 100 billion, with approximately 80% directed toward operating and maintaining existing IT systems, creates institutional modernization pressure that sustains consistent cloud ITSM platform investment across the region's most organizationally complex buyer segments. North America's structural leadership as the global market's dominant demand anchor is expected to deepen.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Cloud ITSM Market Segmentation Analysis

By Component

- Solutions

- ITSM Platform Solutions

- IT Visibility & Control Solutions

- Intelligent Automation Solutions

- Services

- Consulting & Deployment Services

- Integration & Migration Services

- Support & Managed Services

The segment with highest market share under the Component is Solutions, accounting for approximately 75% of the total market. This commanding position reflects the deep organizational preference for integrated platform capabilities that consolidate service desk operations, incident handling, workflow automation, and IT asset visibility within a unified deployment structure. With three-quarters of total market value concentrated within a single component category, Solutions define the commercial priorities, product development investments, and competitive differentiation frameworks of the global cloud ITSM market. The preference for unified platforms is being actively reinforced by the rising cloud workload complexity documented across EU enterprises, where core business process migration into cloud environments creates proportionally expanding requirements for structured service governance and operational coordination.

The structural leadership of Solutions is being further sustained by the progressive integration of AI capabilities into enterprise service management workflows. Eurostat confirms that 55.03% of large EU enterprises used AI technologies in 2025, confirming that the most commercially significant buyer segments are already operationalizing AI across their digital environments. As AI-augmented service automation, intelligent ticket routing, and predictive incident management transition from premium platform features into expected baseline capabilities, solution providers with deep automation integration and workflow intelligence will attract disproportionate enterprise platform investment. The segment's structural dominance as the market's primary revenue contributor is expected to consolidate and deepen.

By Deployment

- Public Cloud

- Private Cloud

- Hybrid Cloud

The segment with highest market share under the Deployment is Public Cloud, accounting for approximately 50% of the total market. This leading position reflects the consistent organizational preference for deployment environments that deliver faster implementation timelines, reduced infrastructure management overhead, and flexible scaling across distributed service teams and geographically dispersed user populations. Public cloud's alignment with enterprise digital modernization priorities is being actively reinforced by rising global internet connectivity, with ITU confirming 6 billion internet users in 2025 whose digital service engagement creates proportionally expanding requirements for cloud-native service management platforms capable of supporting operationally complex and distributed organizational environments.

The structural leadership of Public Cloud is further reinforced by the progressive maturation of cloud governance frameworks across major markets. The European Commission's Cyber Solidarity Act, which entered into force on 4 February 2025, is progressively building enterprise confidence in cloud platform deployment by establishing clearer regulatory frameworks for incident response preparedness, detection obligations, and service continuity governance. As regulatory clarity around cloud security and compliance improves, the governance-related hesitancy that historically moderated public cloud ITSM adoption among more cautious buyer segments is progressively diminishing. This regulatory confidence dynamic is expanding the addressable public cloud ITSM market by converting previously undecided buyer segments into active platform adoption candidates through 2032

Market Players in Global Cloud ITSM Market

These market players maintain a significant presence in the Global cloud itsm market sector and contribute to its ongoing evolution.

- Zoho Corporation (ManageEngine)

- Freshworks

- OpenText

- ServiceNow

- Atlassian

- BMC Software

- Broadcom

- Ivanti

- SolarWinds

- Microsoft

- GoTo

- IBM

- TOPdesk

- EasyVista

- Matrix42

Market News & Updates

- ServiceNow, 2026:

ServiceNow launched Autonomous Workforce and introduced ServiceNow EmployeeWorks, combining Moveworks’ conversational AI and enterprise search with ServiceNow’s autonomous workflows; the company said this brings AI specialists into enterprise work, including a Level 1 Service Desk AI Specialist that can autonomously diagnose and resolve routine IT issues such as password resets, software access requests, and network troubleshooting. For the global Cloud ITSM market, this is one of the most important verified developments because it moves the category beyond assistive copilots toward governed, end-to-end service execution on a unified cloud platform, raising the competitive benchmark for self-service automation, service desk productivity, and AI-native workflow orchestration.

- Atlassian, 2025:

Atlassian launched Service Collection at Team ’25 Europe, bringing together Jira Service Management, Customer Service Management, and Assets into a single AI-powered service suite with Rovo agents; Atlassian also stated that Jira Service Management is already trusted by 60,000 customers worldwide, that 50 percent of the Fortune 500 use it, and that Rovo had orchestrated more than one million workflows in Jira Service Management over the prior six months. For the global Cloud ITSM market, this is a major strategic development because it expands Atlassian from a core ITSM platform into a broader AI-first service management ecosystem spanning internal and external support, intensifying competition around bundled automation, asset intelligence, and cross-functional cloud workflow delivery.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Cloud ITSM Market Policies, Regulations, and Standards

- Global Cloud ITSM Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solutions- Market Insights and Forecast 2022-2032, USD Million

- ITSM Platform Solutions- Market Insights and Forecast 2022-2032, USD Million

- IT Visibility & Control Solutions- Market Insights and Forecast 2022-2032, USD Million

- Intelligent Automation Solutions- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Consulting & Deployment Services- Market Insights and Forecast 2022-2032, USD Million

- Integration & Migration Services- Market Insights and Forecast 2022-2032, USD Million

- Support & Managed Services- Market Insights and Forecast 2022-2032, USD Million

- By Deployment

- Public Cloud- Market Insights and Forecast 2022-2032, USD Million

- Private Cloud- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Cloud- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- SMEs- Market Insights and Forecast 2022-2032, USD Million

- By End User

- BFSI- Market Insights and Forecast 2022-2032, USD Million

- IT & Telecom- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Retail & E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Government & Public Sector- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- North America Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Country

- US

- Canada

- Mexico

- Rest of North America

- US Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Rest of South America

- Brazil Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Germany Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Russia Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

- Saudi Arabia Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia Pacific Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Rest of Asia Pacific

- China Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Cloud ITSM Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component- Market Insights and Forecast 2022-2032, USD Million

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- ServiceNow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Atlassian

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BMC Software

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Broadcom

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ivanti

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zoho Corporation (ManageEngine)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Freshworks

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OpenText

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SolarWinds

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GoTo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IBM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TOPdesk

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EasyVista

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Matrix42

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ServiceNow

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Deployment |

|

| By Enterprise Size |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.