China Elevators & Escalators Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Elevator (By Type (Traction, Hydraulic, Machine Room Less), By Speed (Upto 1 m/s, 1.1 to 2 m/s, 2.1 to 3 m/s, 3.6 to 5 m/s, Above 5 m/s)), Escalator (By Type (Moving Walkway, Moving Stairs))), By Service (New Installation, After Sales Service, Modernization, Maintenance), By Application (Residential, Commercial, Industrial), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Elevators & Escalators Market Statistics and Insights, 2026

- Market Size Statistics

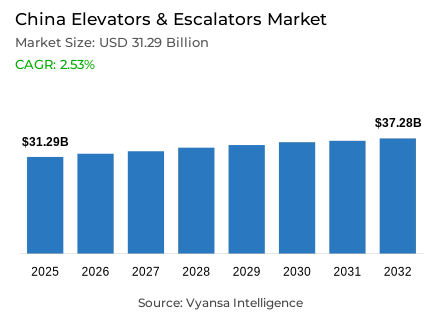

- Elevators & escalators market size in China was estimated at USD 31.29 billion in 2025.

- The market size is expected to grow to USD 37.28 billion by 2032.

- Market to register a CAGR of around 2.53% during 2026-32.

- Product Type Shares

- Elevator grabbed market share of 80%.

- Competition

- Elevators & escalators in China is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 40% of the market share.

- Mitsubishi Electric (Shanghai China) Co. Ltd., Canny Elevator Co. Ltd., Shanghai Johnson Elevator Co. Ltd. (SJEC Corporation), Shanghai Mitsubishi Elevator Co. Ltd., Otis Elevator Company etc., are few of the top companies.

- Service

- New installation grabbed 55% of the market.

China Elevators & Escalators Market Outlook

The China elevators & escalators market size was valued at USD 31.29 billion in 2025 and is projected to grow from USD 32.99 billion in 2026 to USD 37.28 billion by 2032, exhibiting a CAGR of 2.53% during the forecast period. Growth over 2026-2032 will be shaped by steady urban expansion, public infrastructure buildout, and rising lifecycle upgrades across the installed base.

Urbanization reached 67.89% by the end of 2025, with 10.30 million additional permanent urban residents added during the year, reinforcing long-term requirements for elevators & escalators across high-density residential, healthcare, and commercial assets. However, 2025 construction indicators remained weak, as newly started building floor space declined 20.4% year-on-year and real-estate development investment fell 17.2%, which continues to tighten near-term visibility for new-build order inflow.

Modernization is becoming a central growth engine as more than 1.10 million units have already been operating for over 15 years, making upgrades essential for safety and reliability. Policy support adds momentum: since August 2024, more than 160,000 old residential elevators have been included under the ultra-long special treasury-bond subsidy framework, supporting control-system replacement, component renewal, and digital monitoring. This increases the role of elevators & escalators modernization and long-term service contracts in 2026-2032 planning.

Segment fundamentals remain clear, with elevator systems holding 80% of total demand and New Installation accounting for 55% of overall activity. Public infrastructure provides a resilient channel, with 343 urban rail transit lines spanning 11,710.3 kilometers and 6,680 stations as of December 31, 2025, sustaining procurement as well as high-duty maintenance needs. Overall, elevators & escalators demand is expected to stay structurally supported through 2032.

China Elevators & Escalators Market Growth DriverSustained Urbanization Reinforcing High-Rise Mobility Demand

The growing urbanization trend in China remains a key driver of structural demand in the China elevators & escalators market. As per the National Bureau of Statistics (NBS), the urbanization rate in the country has been recorded at 67.89% as of the end of 2025, with 10.30 million new permanent urban dwellers added in a year. From a planning and development standpoint, this gradual shift in the country’s population translates into a consistent demand for vertical transport solutions in residential high-rises, mixed-use developments, hospitals, and commercial districts, where high foot traffic makes elevators and escalators a necessity rather than a luxury.

In real-world project implementation, elevators and escalators take center stage in the usability, accessibility, and footfall control. With the growth of urban assets and the renovation of old buildings, the owners of assets are more concerned with upgrading their systems to improve the comfort of the ride, its reliability, and energy efficiency. This two-fold impact, new high-rise supply and lifecycle upgrades, will provide a stable base demand in both primary installations and equipment enhancement projects in 2026.

China Elevators & Escalators Market ChallengeReal Estate Slowdown Pressuring New Installation Pipelines

The China elevators & escalators market is still very much linked to construction cycles, and 2025 figures reflect this. According to the National Bureau of Statistics, newly started building floor space contracted by 20.4% year-over-year, while total real estate development investment declined by 17.2%. Fewer projects are actually breaking ground, and this directly impacts order volume for new elevator and escalator equipment, clouding market visibility for manufacturers and installation companies dependent on new construction pipelines.

From a project delivery point of view, this situation ratchets up competitive bidding and pricing pressures. Buyers aggressively negotiate contract terms on price, payment, and delivery, while changing project schedules cause problems with labor and inventory management. Installation companies experience uneven labor utilization, while suppliers face increased accounts receivable and inventory risk. While many companies shift their focus to service and upgrade work to stabilize revenues, uncertainty in new construction development continues to impact capacity planning and profitability in 2026.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Elevators & Escalators Market TrendModernization Momentum Strengthening the Installed Base Economy

One of the most characteristic structural changes in the China elevators & escalators market is the increasing role of modernization and retrofitting. Government statistics show that the number of old elevators, those in use for more than 15 years, has already surpassed 1.10 million units, which is a clear indicator of the significant aging of the base that demands modernization and retrofitting for continued safety, compliance, and performance.

Government policy further fuels this trend. Since August 2024, more than 160,000 old residential elevators have been brought under the ultra-long special treasury-bond subsidy program, as reported in government updates until July 2025. This financial assistance helps in the successful implementation of retrofitting, further fueling the demand for modernization kits, intelligent diagnostic systems, and long-term service contracts, thus fueling the revenue shift towards lifecycle solutions in 2026.

China Elevators & Escalators Market OpportunityUrban Rail Infrastructure Offering Stable Long-Term Demand Visibility

The expansion of public infrastructure is also creating sustainable pockets of demand in the China elevators & escalators market. As of December 31, 2025, China has 343 urban rail transit lines, measuring 11,710.3 kilometers in total length and consisting of 6,680 stations, as reported by the Ministry of Transport. Every station needs multiple escalators and elevators to handle the large number of passengers, accessibility requirements, and emergency evacuation needs, thus creating a demand channel linked to government-assisted cycles of investment.

Apart from new installations, public transportation systems create long-term maintenance and upgrade demands because of high-duty usage and strict government regulation. Metro systems' equipment is subjected to heavy usage, requiring predictive maintenance, quick replacement of spare parts, and energy-saving upgrades to reduce peak-hour downtime. Urban rail transportation projects are, therefore, one of the most obvious medium-term market expansion opportunities for suppliers with a proven track record in public projects up to 2026-2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Elevators & Escalators Market Segmentation Analysis

By Product Type

- Elevator

- Escalator

The elevator segment accounts for the largest market share at 80% of the total market demand based on the product type segmentation. This is because of the massive vertical transport market in the country, which is further supported by government statistics showing that there are 11.5324 million registered elevators as of the end of 2024.

Escalators, although very significant in terms of strategy, are still largely concentrated in high-traffic infrastructure like metro stations, airports, and large-scale retailing facilities. By contrast, the day-to-day floor-to-floor mobility in high-rise residential and commercial buildings is largely dependent on elevator systems. This has ensured that the specification norms, spare parts inventory management, and service networks continue to be dominated by the elevator industry, thereby cementing their structural advantage in product development and revenue allocation over the lifecycle.

By Service

- New Installation

- After Sales Service

- Modernization

- Maintenance

Service segmentation-wise, New Installation contributes 55% to the total market demand in the China elevators & escalators market. Notwithstanding the fluctuations in the construction sector, new project announcements from developers, EPC contractors, and government infrastructure agencies continue to demand the entire gamut of new elevator and escalator installations, including startup, inspection, and handing over to the authorities. These new installations are generally embedded in capital spending cycles, thereby providing a relatively clearer volume aggregation for the OEMs and installation partners.

Maintenance & repair and modernization are still very much part and parcel of the overall lifecycle management. However, these services are often highly dispersed among different asset owners and property managers. By contrast, new installations are generally tendered and phased in line with construction milestones, thereby providing relatively stronger short-term volume visibility. This has ensured that the suppliers focus on contractor engagement, speed of execution, and synchronized delivery planning to maximize their share of installation-related revenues.

List of Companies Covered in China Elevators & Escalators Market

The companies listed below are highly influential in the China elevators & escalators market, with a significant market share and a strong impact on industry developments.

- Mitsubishi Electric (Shanghai China) Co. Ltd.

- Canny Elevator Co. Ltd.

- Shanghai Johnson Elevator Co. Ltd. (SJEC Corporation)

- Shanghai Mitsubishi Elevator Co. Ltd.

- Otis Elevator Company

- KONE Elevator (China) Co. Ltd.

- Schindler (China) Elevator Co. Ltd.

- TK Elevator (China) Co. Ltd.

- Fuji Elevator Co. Ltd.

- IFE Elevators Co. Ltd.

Market News & Updates

- Otis Elevator Company, 2026:

In its annual regulatory filing covering FY2025, Otis reported that it purchased the remaining noncontrolling interest in Otis Electric in October 2025, making Otis Electric fully owned by Otis China—an operationally material move in China because it simplifies governance in a historically JV-led structure, increases Otis’ ability to standardize product/platform and procurement decisions, and can improve speed of execution on service digitalization and portfolio optimization at a time when China new-equipment dynamics are volatile and control over pricing/quality/service delivery is a competitive lever.

- KONE Elevator (China) Co. Ltd., 2026:

KONE’s 2025 Annual Review (published February 6, 2026) shows Greater China sales declined 14.3% to EUR 2,166.0 million in 2025 (−11.1% at comparable exchange rates), with New Building Solutions down significantly while Service was stable and Modernization grew significantly—an evidence-backed indicator that the China market mix is continuing to pivot away from new-build volume toward modernization and service value capture, which typically forces OEMs to re-allocate field capacity, prioritize installed-base monetization, and compete harder on digital maintenance and retrofit offerings rather than unit-volume share.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Elevator & Escalator Market Policies, Regulations, and Standards

- China Elevator & Escalator Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Elevator & Escalator Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Elevator- Market Insights and Forecast 2022-2032, USD Million

- By Type- Market Insights and Forecast 2022-2032, USD Million

- Traction- Market Insights and Forecast 2022-2032, USD Million

- Hydraulic- Market Insights and Forecast 2022-2032, USD Million

- Machine Room Less- Market Insights and Forecast 2022-2032, USD Million

- By Speed- Market Insights and Forecast 2022-2032, USD Million

- Upto 1 m/s- Market Insights and Forecast 2022-2032, USD Million

- 1.1 to 2 m/s- Market Insights and Forecast 2022-2032, USD Million

- 2.1 to 3 m/s- Market Insights and Forecast 2022-2032, USD Million

- 3.6 to 5 m/s- Market Insights and Forecast 2022-2032, USD Million

- Above 5 m/s- Market Insights and Forecast 2022-2032, USD Million

- By Type- Market Insights and Forecast 2022-2032, USD Million

- Escalator- Market Insights and Forecast 2022-2032, USD Million

- By Type- Market Insights and Forecast 2022-2032, USD Million

- Moving Walkway- Market Insights and Forecast 2022-2032, USD Million

- Moving Stairs- Market Insights and Forecast 2022-2032, USD Million

- By Type- Market Insights and Forecast 2022-2032, USD Million

- Elevator- Market Insights and Forecast 2022-2032, USD Million

- By Service

- New Installation- Market Insights and Forecast 2022-2032, USD Million

- After Sales Service- Market Insights and Forecast 2022-2032, USD Million

- Modernization- Market Insights and Forecast 2022-2032, USD Million

- Maintenance- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Commercial- Market Insights and Forecast 2022-2032, USD Million

- Industrial- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- Southwest

- Northwest

- North East

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- China Elevator Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Escalator Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Service- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Shanghai Mitsubishi Elevator Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Otis Elevator Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KONE Elevator (China) Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schindler (China) Elevator Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TK Elevator (China) Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric (Shanghai China) Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Canny Elevator Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shanghai Johnson Elevator Co. Ltd. (SJEC Corporation)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fuji Elevator Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IFE Elevators Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shanghai Mitsubishi Elevator Co. Ltd.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Type |

|

| By Speed |

|

| By Type |

|

| By Service |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.