Cameroon Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)) ... Read more

|

Major Players

|

Cameroon Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

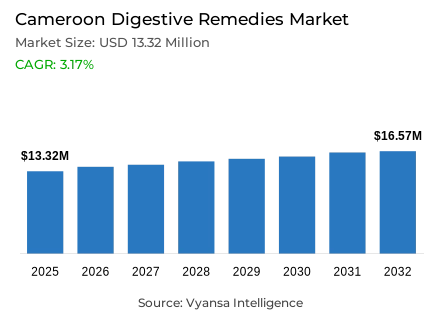

- Digestive remedies market size in Cameroon was valued at USD 13.32 million in 2025 and is estimated at USD 13.83 million in 2026.

- The market size is expected to grow to USD 16.57 million by 2032.

- Market to register a CAGR of around 3.17% during 2026-32.

- Product Type Shares

- Diarrhoeal remedies grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing digestive remedies in Cameroon.

- Top 5 companies acquired around 45% of the market share.

- Ajanta Pharma Ltd, GlaxoSmithKline Plc, UBITHERA PHARMA PVT LTD, EXPHAR SA, Laboratoire Bailly-Creat SAS etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

Cameroon Digestive Remedies Market Outlook

The Cameroon digestive remedies market size was valued at USD 13.32 million in 2025 and is projected to grow from USD 13.83 million in 2026 to USD 16.57 million by 2032, exhibiting a CAGR of around 3.17% during the forecast period. Growth is supported by the continued prevalence of gastrointestinal conditions linked to lifestyle habits, environmental factors, and healthcare infrastructure limitations. High gastritis incidence associated with widespread Helicobacter pylori infection, combined with alcohol consumption levels exceeding 10 litres per capita, contributes to frequent digestive discomfort. These conditions sustain the need for treatments such as antacids, proton pump inhibitors, and anti-diarrhoeal medicines that provide quick symptom relief.

Demand is also influenced by infrastructure constraints that continue to expose populations to water-borne diseases. Although many households report access to improved drinking water, only a few have piped water inside their homes, while around one-third rely on boreholes or tube wells. Such conditions contribute to recurring gastrointestinal infections, supporting the steady use of digestive remedies across the country. Within product categories, diarrhoeal remedies hold a strong position with a 35% share, reflecting the persistent need for treatments addressing acute digestive issues caused by infections and contaminated water sources.

However, the adoption of digestive remedies may face certain limitations due to cultural practices and shifting health behaviour. Traditional and homemade treatments remain widely used, as many consumers continue to rely on remedies passed down through generations. In addition, broader health and wellness changes, including healthier diets and reduced alcohol consumption, could gradually lower the occurrence of gastrointestinal issues. Consumers may also explore preventive options such as dietary supplements, probiotics, and lifestyle adjustments rather than relying only on symptom-based treatment.

At the same time, innovation in product formulations is shaping the competitive landscape for digestive remedies. Manufacturers are introducing improved delivery systems, combination therapies, and convenient dosage formats such as suspensions, chewable tablets, and paediatric liquids to enhance treatment adherence. The category remains highly commoditised, especially among proton pump inhibitors where numerous generic omeprazole and esomeprazole products compete. Distribution is largely dominated by pharmacies, as retail offline accounts for around 95% of sales, supported by regulations that grant pharmacies exclusive authority to sell medicines while restricting distribution through informal retail outlets.

Cameroon Digestive Remedies Market Growth DriverPersistent Health and Lifestyle Pressures Sustain Demand

The ongoing impact of gastrointestinal problems, often due to poor lifestyle choices, environmental problems and general health issues contributes greatly to the continued strength of the overall market for digestive supplements in Cameroon. The prolonged high level of gastritis often characterized by a high prevalence of H. pylori infections in combination with one of the highest levels of per capita alcohol consumption (over ten litres) globally play a significant role in the overall prevalence of digestive-related problems. Due to high levels of stress, primarily as a result of economic depression and political unrest, combined with the prevalence of foods high in fat and/or spicy food, continue to have a severe impact on the prevalence of gastrointestinal discomfort. All these factors combined ensure that consumers will seek fast acting solutions such as antacids and proton pump inhibitors as digestive remedies.

Infrastructure limitations also contribute heavily to high levels of continued gastrointestinal illnesses with many people potentially capable of accessing improved water supplies; however, very few people have access to piped water within their home. Approximately 40% of consumers in Cameroon rely on boreholes/tube wells for access directly to water. These limitations have resulted in extensive access to water borne diseases which, in turn, supports the continued need for the purchase of anti-diarrhoeal products such as loperamide and demonstrate to consumers that purchasing digestive remedies remains a viable method of managing healthcare issues in Cameroon.

Cameroon Digestive Remedies Market ChallengeTraditional Practices Continue to Compete with Modern Treatments

In Cameroon, there is still a heavy reliance by consumers for digestion aids on what they have traditionally used; this is attributed to the cultural norm and the practice of using home recipes. Many consumers continue to use remedies that date back to generations past and many consumers prefer to continue to do so. Even with the availability of scientific studies that show the safety and effectiveness of pharmaceuticals in treating digestion problems, people still prefer to use the old ways to treat these types of problems. Because of these cultural norms and practices, it will continue to limit the amount of demand for scientific pharmaceutical digestion products.

Other changes in health and lifestyles will also impact this category as well. Consumers who improve their diet and reduce alcohol intake may have fewer gastrointestinal problems. As a result of this shift in consumer behaviour towards being healthier, digestion products will face additional competition from dietary supplements, probiotics, lifestyle changes and non-pharmaceutical traditional therapies as more consumers will want to take a preventative approach to treat these types of problems instead of a symptom-based approach.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Cameroon Digestive Remedies Market TrendFormulation Innovation Is Reshaping Competitive Dynamics

A key growing trend in Cameroon’s digestive remedies category is greater emphasis on innovation based on formulation. Competition among PPIs, antacids, and diarrhoeal products will often be driven by patient-orientated design rather than simply relying on availability as a generic. Manufacturers are using better delivery methods, better formulations, and combination therapies aimed at increasing effectiveness, convenience, and compliance with treatment.

The proton pump inhibitor segment continues to be heavily commoditised, with a large quantity of generic omeprazole and esomeprazole products, many of which have been approved, and most of which are manufactured by Indian companies. In contrast, European pharmaceutical manufacturers are implementing new delivery systems (e.g., MUPS-based formulations) and introducing advanced delivery technologies (e.g., sustained release technology) to compete based on those innovations. Innovations in formulas are becoming increasingly focused on convenience and patient adherence, including new formulas for suspensions, chewable tablets and liquid forms for children.

Cameroon Digestive Remedies Market OpportunityPatient-Centric Product Development Creates New Value Areas

An important opportunity within digestive remedies in Cameroon lies in patient-focused innovation and specialised formulations. The new product launches are increasingly centred on improved delivery formats, differentiated combinations, and targeted treatment approaches. These developments aim to enhance ease of use and broaden therapeutic applications, which can create opportunities for companies to move beyond basic commoditised products.

Paediatric formulations in particular represent a promising area of development. The new suspensions and child-friendly versions are expected to expand across the forecast period, largely introduced by Indian manufacturers. By focusing on specialised patient needs and improved administration methods, companies can differentiate their offerings and strengthen product relevance in a market where traditional generics dominate much of the digestive remedies category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Cameroon Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share around product type under the category, with diarrhoeal remedies grabbing market share of 35%. This strong position can be attributed to the continual incidence of gastrointestinal infections as well as diseases associated with water. These types of illnesses will cause consumers to continue to require effective treatment quickly until their diarrhoea subsides, which will lead to even more cases being treated swiftly.

Loperamide-based products are among the most commonly used diarrhoeal therapy products due to their ability to help with the treatment of acute gastrointestinal infections. The continued prevalence of gastrointestinal infections means that diarrhoeal medications will continue to have a major impact on digestive healthcare; therefore, they are the dominating category of product sold in digestive healthcare.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share around the sales channel, where retail offline grabbed 95% of the market. The pharmacies hold the exclusive legal authority to distribute medicines in Cameroon, including digestive remedies.

Under the law, selling or showing medicinal products to the public in informal sales locations such as markets and stores, is illegal. The law enforcement agencies are continually working to reduce illegal pharmaceutical sales in some locations; the Mayor of Yaoundé provided an 8-day warning to all vendors selling medicine in markets and along the roadside that they must stop selling within the 8-day period. Continued efforts by law enforcement agencies reinforce pharmacies are the only permitted retail distribution network to acquire medicine in Cameroon whereby retail pharmacy continues to be the primary access point for over-the-counter digestion medications in this country.

List of Companies Covered in Cameroon Digestive Remedies Market

The companies listed below are highly influential in the Cameroon digestive remedies market, with a significant market share and a strong impact on industry developments.

- Ajanta Pharma Ltd

- GlaxoSmithKline Plc

- UBITHERA PHARMA PVT LTD

- EXPHAR SA

- Laboratoire Bailly-Creat SAS

- OPELLA HEALTHCARE France SAS

- AstraZeneca UK Ltd

- Sanofi

- Bristol-Myers Squibb Co

- SSP Co Ltd

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in Cameroon was relatively fragmented, with EXPHAR SA leading the market with a 12.5% retail value share, followed closely by Laboratoire Bailly-Creat SAS with 11.9%. EXPHAR maintains its leadership primarily through its strong antacid portfolio, particularly the Gastracid brand, supported by product line extensions such as chewable tablet formats designed to improve convenience and treatment adherence. Laboratoire Bailly-Creat also holds a significant position through its established pharmaceutical presence and distribution within pharmacies, which remain the only legally authorised retail channel for medicines in Cameroon. Market demand is driven by high rates of gastrointestinal conditions linked to Helicobacter pylori infections, alcohol consumption, dietary habits and limited access to safe water, which sustain strong demand for antacids, proton pump inhibitors and anti-diarrhoeal treatments. Although pharmaceutical products dominate the formal market, companies continue to face competition from traditional remedies and growing interest in preventive health solutions such as probiotics and dietary supplements.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Cameroon Digestive Remedies Market Policies, Regulations, and Standards

- Cameroon Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Cameroon Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Cameroon Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cameroon Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cameroon IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cameroon Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cameroon Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cameroon Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- EXPHAR SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratoire Bailly-Creat SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OPELLA HEALTHCARE France SAS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AstraZeneca UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sanofi

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ajanta Pharma Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- UBITHERA PHARMA PVT LTD

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bristol-Myers Squibb Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSP Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EXPHAR SA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.