Baltic States Ground-Based Surveillance Radars Market Report: Trends, Growth and Forecast (2026-2032)

By Radar Type (Air Surveillance Radars, Ground & Surface Surveillance Radars, Counter-Battery Radars, Coastal & Border Surveillance Radars), By Range Category (Short-Range Radars (Up to 50 km), Medium-Range Radars (50 km-200 km), Long-Range Radars (Above 200 km)), By Frequency Band (L-Band Radars, S-Band Radars, C-Band Radars, X-Band Radars, Ku/Ka-Band Radars), By Technology (Active Electronically Scanned Array (AESA), Passive Electronically Scanned Array (PESA), Mechanically Scanned Radars), By Mobility (Fixed/Static Radars, Transportable Radars, Mobile Radars (Vehicle-Mounted)), By Application (Air Defense & Early Warning, Battlefield Surveillance, Counter-UAS Operations, Critical Infrastructure Protection, Border & Coastal Security), By End User (Defense Forces, Homeland Security Agencies, Critical Infrastructure Operators), By Country (Estonia, Latvia, Lithuania) ... Read more

|

Major Players

|

Baltic States Ground-Based Surveillance Radars Market Statistics and Insights, 2026

- Market Size Statistics

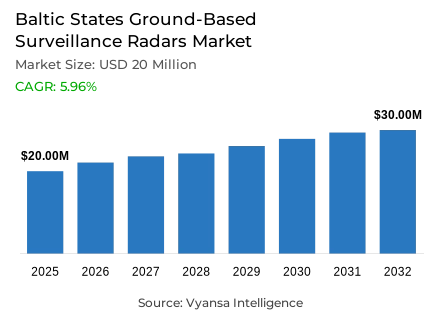

- Ground-based surveillance radars market size in Baltic States was estimated at USD 20 million in 2025.

- The market size is expected to grow to USD 30 million by 2032.

- Market to register a CAGR of around 5.96% during 2026-32.

- Radar Type Shares

- Air surveillance radars grabbed market share of 40%.

- Competition

- Ground-based surveillance radars in Baltic States is currently being catered to by more than 5 companies.

- Top 5 companies acquired around 70% of the market share.

- Kongsberg Defence & Aerospace, Raytheon, Thales (Thales Nederland), HENSOLDT etc., are few of the top companies.

- Range Category

- Medium-Range Radars (50 km-200 km) grabbed 45% of the market.

- Country

- Lithuania leads with a 40% share of the Baltic States market.

Baltic States Ground-Based Surveillance Radars Market Outlook

The Baltic States ground-based surveillance radars market was valued at USD 20 million in 2025 and is projected to grow from USD 25 million in 2026 to USD 30 million by 2032, exhibiting a CAGR of around 5.96% during the forecast period. This steady growth is underpinned by historically high defence budgets across the region - Lithuania allocating 5.38% of GDP, Latvia committing €2.16 billion (4.91% of GDP), and Estonia targeting at least 5% of GDP to national defence in 2026. These funding levels give procurement ministries room to buy new sensors, modernise legacy sites, and invest in secure integration work including tactical datalinks and command-and-control interfaces.

Air surveillance radars dominate demand, accounting for around 40% of the market by radar type. This reflects the Baltic priority of maintaining a continuous recognised air picture that feeds into shared allied frameworks like BALTNET, which is an integral part of NATO's integrated air and missile defence system. Medium-range radars (50–200 km) hold the largest share by range category at 45%, as they suit the regional model of fielding multiple networked sites that together form a unified air picture rather than depending on single large installations.

Lithuania leads the Baltic States with a 40% market share, driven by both its substantial defence allocation and rising operational demand. The country's border authorities intercepted 546 balloon-borne contraband shipments and 50 drones through October 2025, pushing users toward ground-based surveillance radars capable of detecting low radar-cross-section targets and enabling faster response cueing.

Estonia, with approximately 30% of the overall demand in the region, adds to the ecosystem with its developed digital infrastructure, which ranks 1st in the EU’s Digital Economy and Society Index for public digital services in 2025. At the same time, the EU’s €1 billion European Defence Fund 2026 program provides opportunities for Baltic companies to participate in R&D activities in the area of signal processing and cyber-secure integration.

Baltic States Ground-Based Surveillance Radars Market Growth Driver

Escalating Defence Expenditure Strengthens Radar Procurement

Baltic defence planning priorities now include airspace awareness and air defence at the top of the budget stack, which directly drives demand for ground-based surveillance radar. In 2026, Lithuania will spend national defence budgetary allocations of 5.38% GDP, Latvia will spend national defence budget of €2.16 billion (4.91% of GDP), and Estonia will increase defence spending to at least 5% of GDP in its 2026 state budget.

At this level of budgetary allocation, ministries have the flexibility to purchase new sensors, upgrade existing radars, and pay for integration activities (tactical datalinks, secure communications, and command and control interfaces). Budgetary allocations also support training, spares, and life cycle support, which is important since surveillance radars operate 24/7 and must remain interoperable with allied air picture systems.

Baltic States Ground-Based Surveillance Radars Market Challenge

Cyber and GNSS Disruptions Complicate System Deployment

Ground-based surveillance radars increasingly operate as networked “nodes,” so the region’s cyber pressure becomes a real deployment barrier. In 2024, Estonia’s Information System Authority (RIA) registers 6,515 impactful cyber incidents, while Lithuania’s National Cyber Security Centre records 3,874 cyber incidents.

The electromagnetic environment also stays noisy: Riga ATC records 830 GNSS interference reports in 2024, pointing to persistent jamming/spoofing activity around critical airspace systems. Together, these conditions force extra secure-integration work (hardening, encryption, access control, and supply-chain assurance) before radars can be fielded, slowing acceptance testing and raising lifecycle complexity.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Baltic States Ground-Based Surveillance Radars Market Trend

Growing Focus on Low-Altitude and Small-Object Monitoring

Surveillance demand shifts from only “traditional” aircraft tracking toward spotting small, slow objects that still disrupt air traffic and border security. Lithuania’s State Border Guard Service reports 226 balloon-borne contraband shipment interceptions in 2024, and 546 such interceptions in 2025 (reported 30 Oct 2025), showing how frequently these objects appear in operational airspace.

This pattern pushes users to favour radars and processing upgrades that improve detection of low radar-cross-section targets and enable faster cueing to response teams. The same VSAT update notes 54 contraband drones intercepted in 2024 and 50 in 2025 (to 30 Oct 2025), reinforcing the move toward counter-UAS-ready surveillance architectures rather than stand-alone sensors.

Baltic States Ground-Based Surveillance Radars Market Opportunity

EU-Funded Collaborative Defence Innovation Expands Capability Scope

European funding channels now make it easier for Baltic stakeholders to co-develop advanced radar building blocks with larger EU primes, instead of only buying “black-box” systems. The European Commission adopts the European Defence Fund (EDF) 2026 Annual Work Programme and earmarks €1 billion for collaborative defence R&D, including areas that overlap with modern ground surveillance radars (electronic warfare, multi-domain cloud, and secure networks).

Because the programme is consortium-based, local firms and labs can participate via niche contributions such as signal processing, target classification, cyber-secure interfaces, and test tooling. The Commission also states the 2026 work programme includes around €60 million for disruptive technologies and €60 million for SME-focused non-thematic calls, supporting smaller teams that specialise in radar software and integration.

Baltic States Ground-Based Surveillance Radars Market Country Analysis

By Country

- Estonia

- Latvia

- Lithuania

Estonia represents approximately 30% of the Baltic States market, due to its robust digital infrastructure and defence technology sector. Estonia remains committed to its role as a leader in secure digital governance and cyber-resilient infrastructure, which has a direct impact on advanced sensor integration and data-centric defence systems.

Currently, as of 2025, Estonia is at the top of the EU Digital Economy and Society Index (DESI) for digital public services, due to its highly developed national digital infrastructure and secure data exchange infrastructure. Estonia’s highly developed digital infrastructure further improves command and control interoperability and radar data networking, making it a vital contributor to the modernization of ground-based surveillance in the region.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Baltic States Ground-Based Surveillance Radars Market Segmentation Analysis

By Radar Type

- Air Surveillance Radars

- Ground & Surface Surveillance Radars

- Counter-Battery Radars

- Coastal & Border Surveillance Radars

The segment with the highest share under the Radar Type category is Air Surveillance Radars, accounting for around 40% of demand. This dominance reflects the Baltic focus on maintaining a continuous recognised air picture, where ground sensors feed shared command-and-control arrangements and support rapid identification of air objects.

Air surveillance radars also align with the region’s established cooperative air-surveillance framework: BALTNET is described by the Estonian Defence Forces as an integral part of NATO’s integrated air and missile defence system (NATINAMDS), built around sharing surveillance data and tactical datalinks. In practice, this makes air-focused radars the most “network-relevant” asset class in procurement and upgrades, because they plug directly into allied air-picture workflows rather than serving a single site in isolation.

By Range Category

- Short-Range Radars (Up to 50 km)

- Medium-Range Radars (50 km-200 km)

- Long-Range Radars (Above 200 km)

The segment with the highest share under the Range Category is Medium-Range Radars (50 km-200 km), grabbing 45% of overall demand. These systems strike a practical balance: they cover most day-to-day airspace monitoring needs without the heavier footprint and cost typically associated with long-range installations.

Medium-range coverage also fits the Baltic operating model, where multiple sites contribute surveillance data into a shared network rather than relying on a single “strategic” radar. The Estonian Defence Forces describe BALTNET as a framework for sharing surveillance data and tactical datalinks across the three states, which naturally favours radars that can be fielded in several locations and fused into one air picture.

Various Market Players in Baltic States Ground-Based Surveillance Radars Market

The companies mentioned below are highly active in the Baltic States ground-based surveillance radars market, occupying a considerable portion of the market and shaping industry progress.

- Kongsberg Defence & Aerospace

- Raytheon

- Thales (Thales Nederland)

- HENSOLDT

- Saab

- Altimus-Tech

- Pro Patria Electronics

Market News & Updates

- HENSOLDT, 2026:

On February 2, 2026, HENSOLDT reported ESSI orders from Diehl Defence worth over €100 million to supply additional TRML-4D high-performance radars (plus maintenance and training) to multiple European countries—an important Baltic-market signal because TRML-4D sits at the core of modern, mobile air-surveillance and target-acquisition architectures being fielded across Europe, and this scale order indicates accelerating fleet build-out and support-package standardization that can compress deployment timelines and de-risk follow-on radar modernization decisions for Baltic operators prioritizing integrated air picture, counter-UAS, and layered GBAD readiness.

- Pro Patria Electronics, 2025:

On April 3, 2025, Pro Patria Electronics stated it was selected as the winning bidder in an Estonian Centre for Defence Investments (ECDI) procurement for a passive radar system, positioning Estonia to add a low-emission detection layer optimized for tracking hard-to-detect aerial objects (including drones) and strengthening border-area situational awareness—an outcome that materially shifts Baltic ground-based surveillance radar demand toward multi-sensor architectures (passive + active fusion) and expands the addressable opportunity for integration, sustainment, and data-processing upgrades inside Estonia as passive surveillance becomes operationalized at scale.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Baltic States Ground-Based Surveillance Radars Market Policies, Regulations, and Standards

- Baltic States Ground-Based Surveillance Radars Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Baltic States Ground-Based Surveillance Radars Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Radar Type

- Air Surveillance Radars- Market Insights and Forecast 2022-2032, USD Million

- Ground & Surface Surveillance Radars- Market Insights and Forecast 2022-2032, USD Million

- Counter-Battery Radars- Market Insights and Forecast 2022-2032, USD Million

- Coastal & Border Surveillance Radars- Market Insights and Forecast 2022-2032, USD Million

- By Range Category

- Short-Range Radars (Up to 50 km)- Market Insights and Forecast 2022-2032, USD Million

- Medium-Range Radars (50 km-200 km)- Market Insights and Forecast 2022-2032, USD Million

- Long-Range Radars (Above 200 km)- Market Insights and Forecast 2022-2032, USD Million

- By Frequency Band

- L-Band Radars- Market Insights and Forecast 2022-2032, USD Million

- S-Band Radars- Market Insights and Forecast 2022-2032, USD Million

- C-Band Radars- Market Insights and Forecast 2022-2032, USD Million

- X-Band Radars- Market Insights and Forecast 2022-2032, USD Million

- Ku/Ka-Band Radars- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Active Electronically Scanned Array (AESA)- Market Insights and Forecast 2022-2032, USD Million

- Passive Electronically Scanned Array (PESA)- Market Insights and Forecast 2022-2032, USD Million

- Mechanically Scanned Radars- Market Insights and Forecast 2022-2032, USD Million

- By Mobility

- Fixed/Static Radars- Market Insights and Forecast 2022-2032, USD Million

- Transportable Radars- Market Insights and Forecast 2022-2032, USD Million

- Mobile Radars (Vehicle-Mounted)- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Air Defense & Early Warning- Market Insights and Forecast 2022-2032, USD Million

- Battlefield Surveillance- Market Insights and Forecast 2022-2032, USD Million

- Counter-UAS Operations- Market Insights and Forecast 2022-2032, USD Million

- Critical Infrastructure Protection- Market Insights and Forecast 2022-2032, USD Million

- Border & Coastal Security- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Defense Forces- Market Insights and Forecast 2022-2032, USD Million

- Homeland Security Agencies- Market Insights and Forecast 2022-2032, USD Million

- Critical Infrastructure Operators- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Estonia

- Latvia

- Lithuania

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Radar Type

- Market Size & Growth Outlook

- Estonia Ground-Based Surveillance Radars Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Radar Type- Market Insights and Forecast 2022-2032, USD Million

- By Range Category- Market Insights and Forecast 2022-2032, USD Million

- By Frequency Band- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Mobility- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Latvia Ground-Based Surveillance Radars Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Radar Type- Market Insights and Forecast 2022-2032, USD Million

- By Range Category- Market Insights and Forecast 2022-2032, USD Million

- By Frequency Band- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Mobility- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Lithuania Ground-Based Surveillance Radars Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Radar Type- Market Insights and Forecast 2022-2032, USD Million

- By Range Category- Market Insights and Forecast 2022-2032, USD Million

- By Frequency Band- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Mobility- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Thales (Thales Nederland)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HENSOLDT

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saab

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Altimus-Tech

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pro Patria Electronics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kongsberg Defence & Aerospace

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raytheon

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales (Thales Nederland)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Radar Type |

|

| By Range Category |

|

| By Frequency Band |

|

| By Technology |

|

| By Mobility |

|

| By Application |

|

| By End User |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.