Australia Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (Queensland, New South Wales, Victoria, South Australia, Others) ... Read more

|

Major Players

|

Australia Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

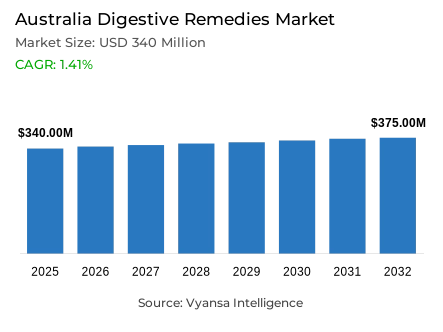

- Digestive remedies market size in Australia was valued at USD 340 million in 2025 and is estimated at USD 346 million in 2026.

- The market size is expected to grow to USD 375 million by 2032.

- Market to register a CAGR of around 1.41% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 40%.

- Competition

- More than 15 companies are actively engaged in producing digestive remedies in Australia.

- Top 5 companies acquired around 50% of the market share.

- Procter & Gamble Australia Pty Ltd, Aspen Pharmacare Australia Pty Ltd, Nestle Australia Ltd, Johnson & Johnson Pacific Pty Ltd, Care Pharmaceuticals Pty Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Australia Digestive Remedies Market Outlook

The Australia digestive remedies market size was valued at USD 340 million in 2025 and is projected to grow from USD 346 million in 2026 to USD 375 million by 2032, exhibiting a CAGR of around 1.41% during the forecast period. Growth remains steady as consumers continue to focus on maintaining digestive comfort as part of overall wellbeing. Increasing awareness of gut health, along with lifestyle patterns such as busy schedules, stress, and irregular eating habits, continues to sustain demand for solutions that help manage common digestive discomfort.

Growing attention to digestive wellness is expected to support the continued relevance of digestive remedies in everyday health routines. Consumers increasingly associate digestive comfort with broader health outcomes such as immune balance and overall physiological wellbeing. At the same time, dietary habits remain a contributing factor to digestive issues. The ABS National Nutrition and Physical Activity Survey shows that 31.3% of Australians’ daily energy intake comes from discretionary foods such as processed or high-fat products, which are often linked with digestive discomfort and lifestyle-related gastrointestinal concerns.

At the same time, digestive remedies operate in a broader wellness environment where preventive approaches are gaining importance. According to the ABS National Nutrition and Physical Activity Survey, around 24.9% of Australians follow a specific diet or eating pattern, including food avoidance or energy-restriction diets. Digital tools are also shaping consumer behaviour, with mobile applications such as the Monash University FODMAP Diet App helping individuals track dietary triggers and manage symptoms like bloating or abdominal discomfort more effectively.

Product demand remains concentrated in commonly used treatment categories, with indigestion & heartburn remedies accounting for around 40% of total sales. These products remain widely used due to the frequent occurrence of symptoms linked to lifestyle and diet patterns. Distribution continues to rely heavily on physical retail environments, as digestive remedies are often purchased during routine shopping trips. Retail offline channels hold about 80% of total sales, supported by the accessibility of supermarkets and the trusted healthcare guidance available in pharmacies.

Australia Digestive Remedies Market Growth DriverGut Health Awareness Keeps Everyday Demand Strong

One major driver for digestive remedies in the Australian market is the increase in consumer interest in the health benefits of the digestive system. This is mainly due to the fact that the digestive system is a critical component of overall wellbeing. In the recent past, consumers have started to view the overall benefits of a comfortable digestive system as a vital component for maintaining a balanced state of wellbeing. This fact alone has led to a situation where consumers are seeking to address the symptoms that come with heartburn, indigestion, and bowel irregularity. In the recent past, the Australian consumer landscape has witnessed a situation where the number of people with busy lifestyles is on the increase. This factor alone has led to a situation where a number of consumers are seeking to address the symptoms that come with a digestive system that is affected by factors such as stress, processed foods, and irregular eating habits.

Recent dietary research indicates that the Australian consumer is likely to experience a number of digestive problems due to the high number of discretionary foods that they consume. According to the Australian Bureau of Statistics National Nutrition and Physical Activity Survey, 31.3% of the daily energy that the Australian consumer requires comes from the consumption of discretionary foods such as processed foods and high-fat foods. This fact alone indicates that the Australian consumer is likely to experience a number of digestive problems due to the high number of discretionary foods that they consume.

Australia Digestive Remedies Market ChallengePreventive Nutrition Alternatives Intensify Market Competition

One major challenge that the digestive remedy sector faces in the Australian market is the increase in the number of preventive wellbeing options that the Australian consumer is embracing. In the recent past, the digestive remedy sector in the Australian market has witnessed a situation where the overall wellbeing benefits of the digestive system extend to foods such as yoghurt, cheese, and other foods that help to promote the benefits of a probiotic diet.

These dietary trends further reinforce the idea that the environment in which OTC digestive remedies compete is an environment of increasing competition. According to the ABS National Nutrition and Physical Activity Survey, approximately one in four people in Australia (24.9%) follow a specific diet or eating pattern, including food avoidance or energy restriction diets. This shows that people in Australia are becoming more inclined towards being proactive in their approach towards digestive health rather than being reactive. As people in Australia become more inclined towards being proactive in their approach towards digestive health, OTC digestive remedies face increasing competition from an overall health and wellness environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Digestive Remedies Market TrendDigital Symptom Tracking Is Shaping Digestive Care

The growing use of digital technologies in the general health and wellness sphere is one of the current trends that can impact the state of the Australian digestive system. Australians are also resorting to mobile applications that help them to monitor their digestive discomforts. This tendency is remarkable as it indicates the increasing tendency to proactive management of digestive health.

One of the brightest examples of such a change is the Monash University FODMAP Diet App that is aimed at helping people with irritable bowel syndrome (IBS) to understand how certain foods and digestive well-being are interconnected. With the Australian population growing increasingly active in their attitude to digestive health, over-the-counter digestive products are facing increased competition with the growing health and wellness industry.

Australia Digestive Remedies Market OpportunityGLP-1 Weight-Loss Therapies Open New Product Pathways

An emerging opportunity that is likely to affect the OTC digestive remedy environment is the increasing adoption of GLP-1 drugs by people suffering from diabetes. As people in Australia become more inclined towards being proactive in their approach towards digestive health, OTC digestive remedy manufacturers could benefit from an emerging opportunity that is likely to affect the OTC digestive remedy environment. As people in Australia become more inclined towards being proactive in their approach towards digestive health, OTC digestive remedy manufacturers could benefit from an emerging opportunity that is likely to affect the OTC digestive remedy environment. This is because people suffering from diabetes and using drugs like Ozempic and Wegovy require digestive health support.

Innovation is already adapting to this change. For example, the Australian company Nutrabalance has recently introduced a High Protein Prebiotic Drink in August 2024, which is designed for digestive health for individuals using GLP-1 weight loss programs. Such products contain protein, fibers, vitamins, and other essential minerals that help in maintaining digestive comfort and overall health. With the growing adoption of GLP-1 therapies in weight management routines, digestive remedy producers can develop new products in the health and wellness space.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share in the product type category, in which indigestion and heartburn remedies hold 40% of the market share. This segment comprises antacids, proton pump inhibitors, antiflatulents, and H2 blockers. These products have been in high demand for many years due to the prevalence of heartburn and indigestion in consumers.

Such digestive issues arise from hectic lifestyles, irregular meals, and the consumption of processed foods. Since such issues arise frequently, consumers look for quick and effective remedies. They prefer OTC products that have already proven themselves in providing the desired results. In this case, the familiarity of the product plays a major part in the purchase decision. Thus, indigestion and heartburn remedies continue to be the major segment of the digestive remedies market.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share in the sales channel category, in which retail offline has the highest share of 80%. This indicates the high influence of retail offline in the digestive remedies market. Retail offline comprises supermarkets and other retail outlets that provide digestive remedies. Such retail outlets benefit from the association of digestive health products and food products. Since consumers purchase food products frequently, they experience digestive discomfort and look for digestive remedies.

Additionally, the pharmacy channel will continue to be significant because of the trusted advice that pharmacists provide regarding healthcare and the wide range of OTC digestive remedies. Thus, the offline channel will continue to be the preferred channel for the purchase of digestive remedies. Even though the online channel will continue to emerge as the new normal in the healthcare industry, the case of digestive remedies will be different because of the in-store purchase of such products.

List of Companies Covered in Australia Digestive Remedies Market

The companies listed below are highly influential in the Australia digestive remedies market, with a significant market share and a strong impact on industry developments.

- Procter & Gamble Australia Pty Ltd

- Aspen Pharmacare Australia Pty Ltd

- Nestle Australia Ltd

- Johnson & Johnson Pacific Pty Ltd

- Care Pharmaceuticals Pty Ltd

- Norgine Pty Ltd

- Reckitt Benckiser (Australia) Pty Ltd

- Haleon Australia Pty Ltd

- Opella Consumer Healthcare ANZ

- Bayer Australia Pty Ltd

Competitive Landscape

The competitive landscape of digestive remedies in Australia is characterised by the presence of established multinational and local players competing through strong brand portfolios and consumer trust. Johnson & Johnson Pacific Pty Ltd leads the market with a value share of 13%, supported by a diverse portfolio that includes brands such as Mylanta in antacids and H2 blockers and Imodium in diarrhoeal remedies. Care Pharmaceuticals Pty Ltd follows with a value share of 11.1%, benefiting from the strong performance of its Hydralyte brand, which dominates diarrhoeal remedies and offers a wide range of SKUs across multiple retail channels. Competition in the category is shaped by high brand familiarity and consumer trust, which favour established international brands. Companies also compete through product format innovation, portfolio diversification and wide distribution across supermarkets and pharmacies, ensuring accessibility while addressing the rising consumer focus on digestive health and gut wellbeing.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Australia Digestive Remedies Market Policies, Regulations, and Standards

- Australia Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Australia Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Queensland

- New South Wales

- Victoria

- South Australia

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Australia Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Johnson & Johnson Pacific Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Care Pharmaceuticals Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Norgine Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser (Australia) Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haleon Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Procter & Gamble Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aspen Pharmacare Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestle Australia Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Opella Consumer Healthcare ANZ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer Australia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson Pacific Pty Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.